The 15 Most Important ETFs

[Editor's Note: In celebration of ETF Report’s 15th anniversary, we have created what we feel are the 15 most important U.S.-listed ETFs, one for each year of ETF Report’s existence. These featured funds are the ETF industry’s biggest game changers, and at least some of them are likely among the core holdings in your portfolio.]

SPY: SPDR S&P 500

And then there was "SPY"…

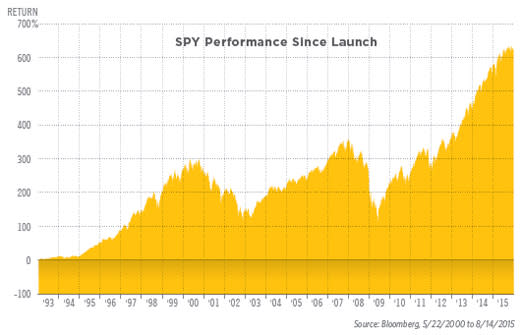

The brainchild of the late Nate Most, the SPDR S&P 500 (SPY | A-99) was the first U.S-listed ETF launched in January 1993.

SPY is no small achievement. It gave rise to what is today a $2.1 trillion U.S. ETF industry, comprising more than 1,700 funds. Globally speaking, it helped pave the way for thousands of ETFs, with nearly $3 trillion in global assets today.

SPY is also the largest ETF in the market, boasting roughly $170 billion in assets under management. And it's the most liquid security in the world, trading some $27.4 billion on average every day.

"SPY sparked a revolution in the asset management industry that significantly improved access to the markets and lowered costs for all investors," said Jim Ross, global head of ETFs at State Street Global Advisors, who was part of the original team that brought SPY to market.

While there were other strategies before SPY that sought to offer investors the ability to trade an index—such as the Toronto 35 Index Participation Units (TIPS), which tracked the Toronto 35 Index—SPY was the first bona fide ETF. TIPS lacked the creation/redemption structure ETFs are known for, and it had no mechanism to ensure it tracked its underlying index closely throughout the day, Ross says. SPY also was the first ETF product registered under the Investment Company Act of 1940.

But SPY has its quirks, too.

The fund is actually a unit investment trust that has an expiration date: Jan. 22, 2118, or 20 years after the death of the last survivor of 11 people named in the Trust Agreement, the oldest of whom was born in 1990 and the youngest of whom was born in 1993, according to Kathleen Moriarty, the attorney who helped bring SPY to market—and countless other ETFs since.

That date can be extended. In fact, it already was once. When the fund first came to market, it was set to expire 25 years later, or January 2018—less than three years from now.

The history of its name is also amusing. SPY was originally named "SPIRS," which was the acronym for Standard & Poor's Index Receipts.

"Eventually, it was decided that 'SPIRS' sounded like 'SPEARS' and no one wanted the product to be dubbed with the name of a weapon," said Moriarty, who's a partner at Kaye Scholer's Investment Management Group, said. SPY has also gotten cheaper over the years. It launched with an annual expense ratio of 0.20%. Today the fund costs 0.09%.

EWJ: iShares MSCI Japan

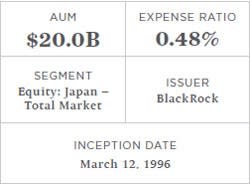

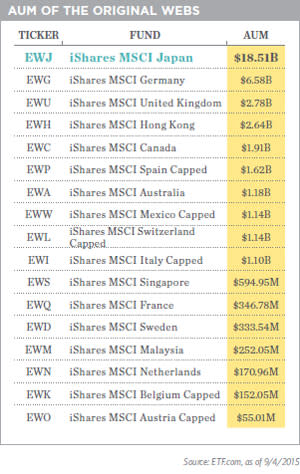

The iShares MSCI Japan (EWJ | B-99) was launched in 1996 as part of Morgan Stanley's World Equity Benchmark Series, which were a group of country-specific funds that tracked Morgan Stanley Capital International (MSCI) country indexes. The funds were developed with Barclays Global Investors, and in 2000, were renamed the iShares MSCI Series.

These were the first ETFs to provide exposure to foreign markets, which was revolutionary at the time. And it allowed for price discovery when those markets were closed during U.S. trading hours. Before this, outside of the options market, there wasn't a live price for a market like Japan.

"In 1996, I would say nobody I knew was talking 'price discovery,'" said Dave Garff, managing director of Walnut Creek, California-based Accuvest Global, who was a broker then. "And you wanted to own tech. You weren't really thinking internationally."

Global investment options, though, would soon be very much on radar screens everywhere.

"In 2004, dollar volumes of non-U.S. ETFs exploded," said Garff. "Part of that has to do with the fact that during that time, you have non-U.S. assets that are making money and U.S. markets underperforming. I personally believe it was the performance that drove the interest."

And in 2015, country-specific ETFs have become sliced and diced much like the rest of the investment universe.

"EWJ is a great segue in to the things you can do now with Japan ETFs," Garff added. "There are all kinds of Japan ETFs now: large-cap, small-cap currency-hedged, noncap-weighted. The only way any of those were going to happen for investors was if EWJ was successful."

We chose EWJ as opposed to the other WEBS products because of Japan's markets being closed during U.S. trading and the price discovery it created. Most of the other country-specific products were in European or South American markets, which also have some overlap with the U.S. We could just as easily have chosen any of the other original WEBS funds.

EWJ tracks a market-cap-weighted index of Japanese stocks, providing broad exposure to the Japanese equity market with a large-cap tilt, and excludes most small-caps. Industry tilts are present, but very minor.

When it comes to liquidity, EWJ is a titan today. The fund trades hundreds of millions of dollars on most days, at pennywide spreads. Its massive assets under management—nearly $20 billion—and strong liquidity set EWJ apart from its Japan ETF competitors.

XLK: Technology Select Sector SPDR

The idea of sector investing is so entrenched in the market today that it's hard to imagine that, as recently as the late 1990s, it was virtually impossible to do.

But Dan Dolan, one of the creators of the $95 billion Select Sector SPDRs family, remembers.

"[In the late 1990s] Chuck Clough was our well-respected chief investment strategist at Merrill Lynch," Dan recalled. "He was there more than 10 years and had a huge following. He had a sector-based model where he would over- and underweight sectors and talk about what he liked and didn't. The advisors loved him, but he had a hard time implementing his strategy."

Enter the Select Sector SPDRs. The ETFs, which launched in 1998, divided the S&P 500 into nine distinct sectors, allowing Merrill Lynch advisors (and everyone else in the market) the opportunity to slice, dice, over- and underweight sectors however they wanted.

Beyond model usage, Dolan says, they expected advisors to use the funds to customize the S&P 500 and institutions to trade sectors long and short. And use them they did.

"At the time of the launch, having a $1 billion ETF trust was huge," noted Dolan. "We were able to raise $500 million even before our nine ETFs started trading. We thought Sector SPDRs could one day be a $10 billion family."

Today they stand a little north of $95 billion in assets, and have sparked a wave of more than 400 competing sector, subsector, industry and niche ETFs.

From the beginning, however, technology was hot.

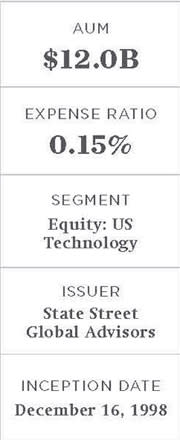

"In the late 1990s when we launched, technology was the star, and we knew the Technology Select Sector SPDR (XLK | A-89) would generate huge demand; it was half the trust assets for the first few years," Dolan added.

Today XLK is the third-largest Select Sector SPDR, trailing the $17.8 billion Financial Select SPDR (XLF | A-89) and the $14 billion Health Care Select SPDR (XLV | A-94).

For investors of all stripes, sector investing has become another tool that ETFs have provided in an easy, inexpensive manner. XLK, to us, is the epitome of how the market can be sliced in a passive vehicle.

QQQ: PowerShares QQQ

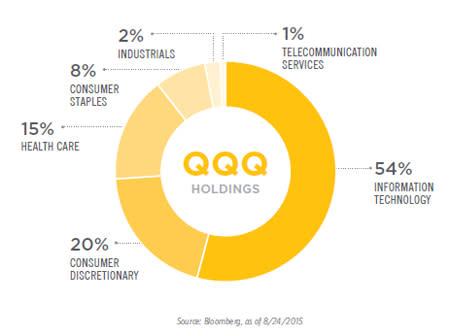

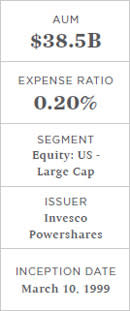

The PowerShares QQQ (QQQ | A-67) is one of the more interesting ETFs in the market. Also known as the "cubes" or the "Q's," the fund tracks an index that seemingly makes no sense. That hasn't dampened popularity for the fund one iota, and it's currently the second-most-actively traded ETF in the United States.

Launched in March 1999, QQQ was initially called the Nasdaq-100 Trust, Series 1 and it traded on the American Stock Exchange. Though now owned by Invesco PowerShares, the ETF was initially introduced by Nasdaq itself, with the aim of increasing trading volume in Nasdaq-listed securities.

To that end, the ETF tracked the Nasdaq-100, an index designed by the stock exchange that comprised the 100 largest nonfinancial securities that traded exclusively on the Nasdaq. The financial companies were relegated to their own index, giving the Nasdaq-100 a heavy bias toward health care, consumer discretionary and in particular, technology.

For the Q's, the timing of the launch couldn't have been better. The late '90s were the heyday of the dot-com bubble, and investors were gaga for all things tech. The fund gained immediate traction, and the ETF quickly became the most-traded security on the stock market.

Nearly a year after the QQQs launched, the tech bubble reached its peak, and the fund hit its highest point ever, at $120.50, 135% above where it was only 12 months earlier. Unfortunately for tech enthusiasts, the mania didn't last, and the subsequent bursting of the Internet bubble sent the ETF plunging to an all-time low of $19.76 in October 2002, a loss of 84% from its peak.

Recently, the Q's have made a comeback alongside the broader stock market, with the fund trading as high as $114 this year. Throughout its wild swings, the ETF has remained popular, and the No. 1 choice for many tech traders, even though the fund only has about a 54% weighting in the technology sector.

"The Nasdaq-100 doesn't have any financials, but it doesn't mean it's all tech," said John Jacobs, senior advisor of Nasdaq, Inc.

"If you look at the breakdown, it includes all sorts of industries. It's [really] a nonfinancial growth index," he added.

Perhaps a big reason for QQQ's consistent popularity is its relatively large marketing budget. According to the fund's prospectus, 0.05% of the fund's assets are used annually for marketing purposes.

Using the current asset base of nearly $40 billion, that's a $20 million budget for advertising, which translates into exposure not just for the Q's, but ETFs as a trading and investment vehicle more generally.

IVV: iShares Core S&P 500

The SPDR S&P 500 (SPY | A-99) was the original U.S.-listed ETF, but several years later, with the launch of what is now known as the iShares Core S&P 500 ETF (IVV | A-99), it was confronted with its own doppelganger as a direct competitor.

IVV was one fund in a wave of roughly 40 launches from iShares, then a part of Barclays Global Investors, in 2000 that really established the ETF family as a major player in the space. While SPY was designed as a trading tool, BGI's lineup was more advisor-friendly, offering all the core index funds that would be on the average advisor's wish list.

IVV was offered as part of a plan to provide a complete and broad product family, according to former iShares head Lee Kranefuss, but BGI's internal models also suggested that the fund would not only drain assets away from SPY, but would come to represent 60 to 70% of the total iShares assets under management.

Objectively speaking, IVV has a better construction than SPY, which is a grantor trust and cannot reinvest dividends. IVV has no such handicap. But most importantly, it was—and still is—cheaper than SPY.

"We thought that price was all important. We thought there would be a big deflation of [SPY]," Kranefuss said.

But while IVV has never lacked for assets, it was only last year that the fund pushed its way past the iShares MSCI EAFE ETF (EFA|A-93) and finally became the second-largest ETF in the world, behind SPY.

IVV is far from a failed experiment. Kranefuss notes that IVV helped to drive down the price of the S&P 500 for investors, as well as to lower spreads. Prior to IVV's launch, SPY was trading a quarter wide.

What was really important about IVV though, Kranefuss says, was that it showed that price is not the only criteria that investors use in selecting an ETF. If it were the only criteria, SPY would have ended up with no assets.

SPY had the advantage of being the first to market and established liquidity. IVV gathered assets in part because of its lower price but also because iShares made an effort to compete on customer service, Kranefuss adds.

IVV currently has roughly $67 billion in assets under management compared with SPY's $163 billion. Given that more advisors are moving toward ETFs, however, that gap might not be as insurmountable as some may think.

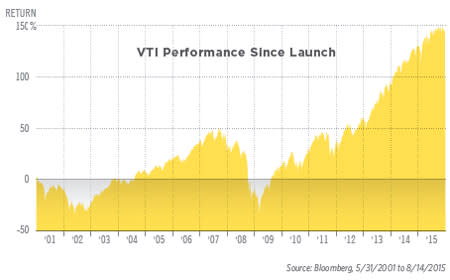

VTI: Vanguard Total Stock Market

Vanguard was always a pioneer, and its Vanguard Total Stock Market ETF (VTI | A-100) was nothing short of a major breakthrough for the industry.

Launching in 2001—some eight years after the very first U.S.-listed ETF debuted—VTI helped set the stage for what became an industry acutely focused on costs. It also helped bring ETFs into the mainstream retail market and popularize the structure among financial advisors. Today VTI boasts roughly $55 billion in assets.

It's no surprise Vanguard would rise to become the second-largest ETF issuer, with $456 billion in ETF assets as of August 2015. The company was ahead of the game in the equity index mutual fund space back in the 1970s. When Vanguard launched VTI as a share class of its Total Stock Market Index Fund, the mutual fund was the firm's best-selling equity fund, and one of the industry's most popular.

Known for its "characteristic candor and disclosure regarding costs," as Gus Sauter, managing director of Vanguard's Quantitative Equity Group, said at the time VTI came to market, Vanguard proved with VTI and its other ETFs that keeping costs low works.

"VTI marked the entrance of Vanguard into the ETF market, opening up a new distribution channel for our indexing experience and expertise," said Martha King, managing director at Vanguard. "VTI and the low-cost Vanguard ETFs to follow in subsequent years brought additional choice to investors and much-needed cost competition to the industry."

But VTI's success—and the success of Vanguard ETFs in general—hasn't come without its challenges. Right out of the gate, there was the issue of a name. Vanguard originally named its ETFs VIPERs, for Vanguard Index Participation Equity Receipts. The not-so-cuddly image wasn't a huge success, and Vanguard rebranded in 2006.

Another obstacle Vanguard ETFs had to face was the disbelief in the ETF structure the company's founder John Bogle never hesitated to share. Bogle, an avid fan of index investing, questioned the use of trading an index fund throughout the day. To him, ETFs were for day traders and not for the long-term investor Vanguard best served. He's still vocal about that all these years later.

Of note, unlike other ETF providers, Vanguard built its ETFs as share classes of existing mutual funds instead of stand-alone investment vehicles. Mutual fund shareholders were allowed to convert to ETF shares if they wanted to—a feature that appealed to Vanguard clients who already believed in index investing, but liked the feature of intraday pricing.

LQD: iShares iBoxx $ Investment Grade Corporate Bond

In 2002, the first fixed-income ETFs began trading, and perhaps no other fund represented such an important turning point for investors as the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD | A-77).

It launched alongside three Treasury ETFs, but Treasurys had always been a liquid market with few concerns about pricing or defaults. Investment-grade corporate bonds, though, were a different story.

Bonds don't trade on an exchange and investors can't get real-time pricing on individual issues. But ETF pricing is available in real time. While its underlying index tells one story, the price of LQD tells another story. It reflects the markets' real-time opinion of the value of its portfolio, and that offers all investors—even those who aren't investing in bonds—valuable information.

"When LQD launched, it really created the first way that investors could see what was happening in the bond market in real time. I think one of the biggest benefits it's provided since it launched is being a barometer for the corporate bond market," said Matt Tucker, head of the iShares Fixed Income Strategy team.

"It's a pioneer fund that created this concept of a visible fixed-income market and delivered it out to all investors," he added. For investors in the fund, it makes establishing a corporate bond position much easier and convenient due to the intraday trading, the ability to execute different types of orders and the ability to see a two-sided market, complete with bids, asks and spreads, Tucker says.

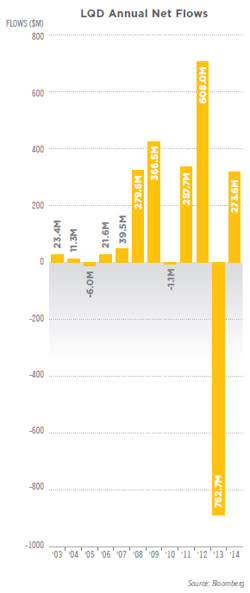

But the story of LQD is also one of liquidity, as its ticker implies. Tucker notes that from its 2002 launch through much of 2008, the fund traded an average of $20 million a day and was primarily used as a buy-and-hold vehicle by the retail and wealth markets. And then the financial crisis happened, and bond liquidity dried up.

It was during the crisis that institutions discovered LQD, Tucker says. By the fourth quarter of 2008, its average daily volume stood at $160 million, and currently stands at $320 million. Bond liquidity has continued to be an issue for investors, and that has had an impact on LQD's popularity.

"LQD is actually helping to solve the problem by delivering liquidity to the corporate bond market," Tucker said. "LQD is not the entire solution, but it's helping to address some of the market structure concerns people have today."

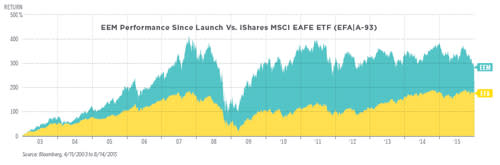

EEM: iShares MSCI Emerging Markets

The iShares MSCI Emerging Markets ETF (EEM | B-100) was the first emerging market ETF—and that's saying a lot.

Prior to EEM's launch in 2003, there had been a long, simmering debate in the emerging market space suggesting you simply couldn't provide low-cost exposure to developing markets to U.S. investors.

EEM proved that wasn't true, and that was momentous, which put this cap-weighted index of emerging market firms on this list.

Similarly, there was an argument that active managers would always outperform in the emerging market space, which has always struck us as a sort of colonialist view of investing. But passive-vehicle EEM disproved that argument as well, and became an enormously successful product, helping establish iShares as the dominant ETF issuer.

"Before EEM, you had to set up local brokerage accounts, establish local relationships, and sometimes there were tax implications and other mechanisms that made [investing in emerging markets] very cumbersome. Brazil was always a nightmare," said Mark Dow, founder of Dow Global Advisors, who has more than 20 years of experience as a policymaker, investor and trader focused on global macro and emerging markets.

Certainly, one side caveat was tracking issues with EEM early on, which really helped launch Vanguard into the space two years after EEM with it FTSE Emerging Markets ETF (VWO | B-88), which is now the bigger of the two in terms of assets. iShares, obviously, eventually corrected that tracking problem, and EEM continues to be a major provider of assets.

"EEM allowed one simple way to get in and out," Dow added. "It's a trading vehicle, so that will make things get whipped around a little bit more. But it's also a vehicle that will allow the long-term investor a very easy and low-cost way to get exposure to a major asset class."

Since EEM doesn't significantly optimize its portfolio, its sector and country bets are fairly muted. (EEM includes South Korea as emerging; rival VWO doesn't.) The fund's index also doesn't go down the market-cap spectrum very far, which helps tilt the portfolio's average market cap slightly higher than the market's.

But credit EEM with being the first ETF to open "impossible" markets to indexing.

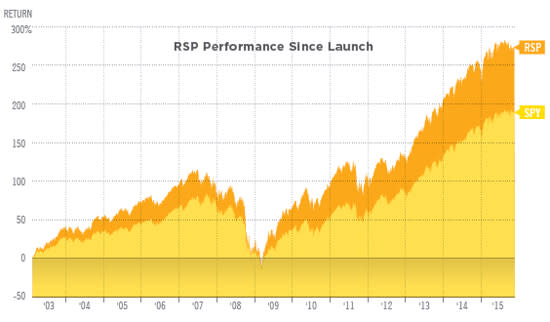

RSP: Guggenheim S&P 500 Equal Weight ETF

Smart-beta ETFs are currently all the rage, but they're not exactly a new concept. The Guggenheim S&P 500 Equal Weight ETF (RSP | A-83), which launched in 2003, was actually the first fund to entirely eschew weighting by market capitalization. And RSP's fairly consistent outperformance compared with its cap-weighted brethren (SPY and IVV) is likely part of the impetus behind the widespread popularity of alternatively weighted ETFs that we see today.

According to Bill Belden, managing director of Guggenheim Investments, the origins for RSP actually date back to the early 1970s, when an equal-weighted S&P 500 portfolio was first managed for an institutional investor as a separately managed account. But along with a general lowering of commission fees, it really was the ETF wrapper that made an equal-weighted portfolio practical for many.

The strategy came with significant transactional costs and tax consequences when packaged as a separately managed account or a mutual fund that diluted its outperformance relative to a cap-weighted S&P 500 strategy. Belden says that the ETF wrapper, with its in-kind transaction mechanism, offered both transactional and tax advantages.

"It's an efficient delivery of an impressive performance story," he explained, noting that a common criticism of smart-beta approaches is that their execution requires a higher number of transactions. The implication seems to be that the current smart-beta phenomenon wouldn't be possible without ETFs.

But it's that performance that's arguably the most interesting part of RSP's rise. A look at a graph comparing its history to that of SPY shows an ever-widening performance gap.

While Belden attributes some of RSP's outperformance to severing the link between a stock's price and its index weight, he believes the regular rebalancing has been a bigger factor, because it means the portfolio is regularly buying stocks after they've fallen in price, and selling them after they've risen in price.

"The rebalancing schedule—which happens on a quarterly basis—has really helped drive what value has been delivered through RSP over its 12-plus years of history," Belden noted.

To Guggenheim, RSP is a core large-cap holding for client portfolios, even if it's riskier than market-weighted vehicles. The added risk of higher volatility associated with an equal-weight strategy has been rewarded by the outperformance, which tends to be greater in rising markets, Belden says.

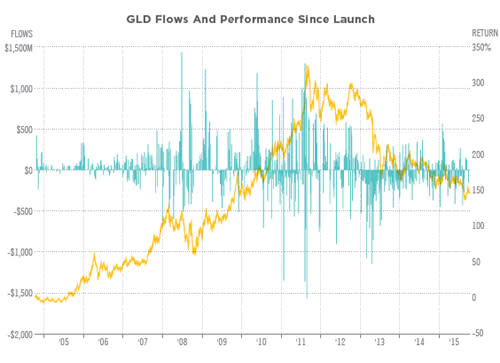

GLD: SPDR Gold

[Editor's Note: This version has been corrected to state that GLD was the first ETF launched in the U.S. to hold physical gold; it was not the first-ever launched of such.]

People have been using gold for millennia. The yellow metal's roots as jewelry and money can be traced all the way back to ancient Egypt, some 5,000 years ago. Gold's reign as the top currency lasted all the way until the last century, when it was finally jettisoned in favor of fiat money.

But gold is still valuable. People remain instinctively drawn to the metal, and its luster is unlikely to wear off any time soon. In fact, millions of ounces of gold continue to be bought every year, and not just for decorative purposes.

Indeed, much of the demand for gold now comes from investors who see the metal as a stable store of value. But rather than buying physical gold bars or coins, these investors are buying up SPDR Gold Shares (GLD | A-100), the revolutionary exchange-traded fund that has brought the ancient metal into the 21st century.

Launched in 2004 by State Street Global Advisors, GLD was the first ETF in the U.S. to hold physical gold. It was an instant hit, gaining more than $1 billion in assets in less than a week, a record that still stands today.

"It's transformed the way people think about gold and investing in gold," said World Gold Trust's CEO Will Rhind. "It also opened the door for investing in commodities more broadly as an asset class, which has become a key portfolio component over the last 10 years."

In fact, since GLD's launch a decade ago, more than 100 commodity ETFs have followed, and today the category boasts more than $50 billion in total assets.

That said, it certainly hasn't been a smooth ride for GLD. The fund's fortunes have waxed and waned based on the demand and price outlook for gold. At one point in 2011, as gold prices were peaking at a record high of $1,921, GLD briefly became the world's largest ETF, with $77.5 billion in assets.

Since then, assets have been slashed to $25 billion amid a combination of outflows and plunging gold prices. Nevertheless, the fund remains the largest and most liquid gold ETF by far.

Gold may be down, but it's not out. If history is any guide, peoples' fascination with the yellow metal isn't going away any time soon, and that means GLD is here to stay.

USO: United States Oil

What's the first company you think of when it comes to commodity ETFs? It's probably not any of the big ones like Deutsche Bank or Citigroup. Rather, you might think of United States Commodity Funds (UCSF), the issuer of highly popular ETFs such as the United States Oil Fund (USO | B-100) and the United States Natural Gas Fund (UNG | C-100).

Founded in 2006, USCF is a 10-person company based in Oakland, California. No one would have guessed this little upstart would be able to compete with the big ETF providers, but that's exactly what it's done.

USCF's flagship product, the United States Oil Fund, was one of the most daring launches in exchange-traded fund history, and catapulted the firm into the dominant position when it came to commodity ETFs.

USO was the first crude oil-linked ETF in history, as well as the first single-commodity futures ETF. The fund gave individual investors and advisors easy access to one of the most esoteric corners of the market for the first time, effectively bringing commodities to the mainstream investor.

"Prior to USO, if you wanted access to the global crude oil market, you would have to have a futures account or you would have to use an imperfect proxy like oil stocks," said John Love, president and CEO of United States Commodity Funds.

"We thought it'd be a great product. It's constructed very simply, so you always know what's in there. That's one of the things that has helped popularize the ETF," he added.

Now there are more than 100 commodity ETFs on the market, most of them futures-based funds. But with new access comes new risks, something that USO has exposed to the world. The fund has performed abysmally since its inception in 2006, losing 81% of its value.

Part of that is due to the poor performance in crude oil futures, which have dropped 43%. The other part is due to contango and the associated "roll costs" from that. Thanks to USO, commodity ETF investors are now well aware of terms like "contango" and "backwardation" and the impact they have on returns. Or at least they should be.

Despite the ugly returns, the $2.8 billion USO has done what it was designed to do: provide exposure to front-month crude oil futures contracts. It's probably not an ETF that investors should hold long term, but it's a great tool for traders and those with shorter-term horizons.

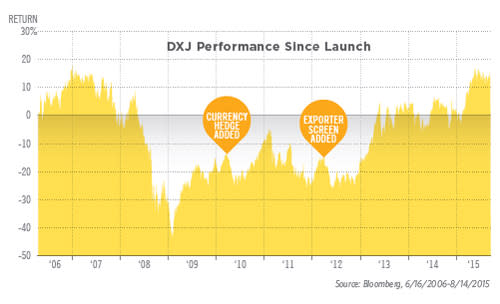

DXJ: WisdomTree Japan Hedged Equity

We chose the WisdomTree Japan Hedged Equity ETF (DXJ | B-64) and not one of WisdomTree's dividend-weighted products because, in many ways, DXJ opened up a whole new idea of currency hedging, which we believe is transformational for how advisors interact with the market.

Despite investors having been able to buy international stocks for 100 years, understanding that currency is a significant driver of those returns has never been so obvious until now. DXJ had a large role in changing that mindset.

Today investors realize they're making two bets when they invest overseas: one on the stocks, and one on the currency. That's transformational.

DXJ started out as a Japan equity ETF in 2006, some 10 years after the first Japan equity ETF—the iShares MSCI Japan ETF (EWJ | B-99)—launched. In 2010, Wisdom Tree added the currency hedge after the yen strength kept surging shortly after the financial crisis.

"Seeing headlines every morning that read, 'Yen Is Up, Japanese Exporters Hit,' and having thought this could potentially reverse one day was one simple inspiration for the addition of a currency hedge to DXJ in April 2010," said Jeremy Schwartz, director of research for WisdomTree.

"A further enhancement was decided in the middle of 2012—ahead of Shinzo Abe's election as prime minister," he added. "The fund would target exporters [under the premise that] an eventual weak yen would make Japan's multinationals more competitive globally, and that change went into effect in the fund on Nov. 30, 2012."

Currently, DXJ's narrow thesis selects export-oriented, dividend-paying Japanese firms, dividend-weights them and hedges its yen exposure. The fund positions itself to gain from increased trade and a devalued currency to the extent that dividend-paying firms benefit.

The fund's $18 billion in assets under management confirms investor understanding of currency hedging, with more than $14 billion of that having come in after Abe's election.

That gives the fund very good liquidity and makes it easy to trade. The fund's 0.48% expense ratio also makes it relatively cheap to hold.

"Abe's election in December 2012 was a critical catalyst for raising awareness of the currency risk inherent to traditional, nonhedged international equity funds," Schwartz said.

WisdomTree now offers a total of 17 currency-hedged equity ETFs, and most major ETF issuers have also initiated currency-hedged products on the heels of DXJ's success.

SSO: ProShares Ultra S&P 500

Leveraged and inverse ETFs have been among the most controversial ETF products on the market since before they even launched.

ProShares first filed for the right to launch leveraged/inverse ETFs in 2000, and the filing sat at the Securities and Exchange Commission for more than six years before the funds finally got the green light in 2006.

"When we began the process, the [ETF] industry was still very young," said Morgan Gold, managing director at ProShares. "As the industry grew, investors began to look for a wider choice of strategies in ETFs—including ones designed to help manage risk and enhance returns. By 2006, when we introduced the first geared ETFs, the industry and investor needs had evolved. The time was right for geared ETFs."

Asset flows and trading volumes certainly support that statement.

Leveraged and inverse funds rocketed out of the gate, attracting billions in assets in their first few years as investors embraced the easy leverage or downside exposure they offered.

But use of the funds was not without its issues. Not all investors understood that the funds were (and are) designed primarily for short-term use, and that delivering two times the daily return of the S&P 500, for instance, does not mean delivering two times the long-term return of that index.

ETF Report was actually the first to report on this disconnect, in a memorable June 2007 cover article, "1+1≠2."

Following the market volatility in 2008, which exacerbated the impact of the daily rebalancing, the products were banned by UBS and a number of other advisory firms on the grounds that advisors did not understand them.

Still, following a significant educational effort, things settled down and the products remain popular among hedge funds, institutional investors and certain advisors. There are currently 270 funds on the market and billions of dollars in assets.

One of the first leveraged ETFs on the market, the ProShares Ultra S&P 500 ETF (SSO), remains one of the largest.

"Our geared funds remain an important part of our overall product offering," said Gold. "They are used extensively by a diverse shareholder base. We recently added a number of geared ETFs to our lineup, and we expect to continue to respond to market demand for new products in the future."

SCHB: Schwab U.S. Broad Market ETF

Charles Schwab's entry into the exchange-traded fund market in 2009 changed the game for ETF investors in multiple ways.

First, there was the pricing. Schwab's message to the market was simple: We will not be undersold.

The firm launched a suite of four simple, broad-based ETFs, and priced them lower than anything else on the market.

The Schwab U.S. Broad Market ETF (SCHB | A-100), which quickly became Schwab's most popular fund, launched with an all-in fee of just 0.08%, making it the cheapest ETF on the market and undercutting competitors like the SPDR S&P 500 (SPY | A-99) by 1 basis point. It has been the low-cost leader in the ETF market ever since, currently charging just 0.04% a year.

Even more importantly, at its ETF launch, Schwab said it would allow all 8 million Charles Schwab customers to trade its ETFs commission-free.

That was revolutionary. Without commissions, ETFs suddenly made sense for retail investors, and strategies like tax-loss harvesting and frequent rebalancing suddenly made sense for advisors.

The impact was immediate and has only increased over time: According to Schwab, ETF assets custodied at the firm have grown from $83 billion in December 2009 to $231 billion at the end of 2014.

Meanwhile, brokerages like Fidelity and TD Ameritrade have been forced to respond with their own commission-free programs, letting millions of individual investors participate in the ETF market for the first time.

The biggest effect of Schwab's entry into the ETF market may be still to come.

"What I find very exciting is the role that Schwab ETFs are playing in two of the most ambitious and potentially landscape-changing initiatives in all of financial services today," said John Sturiale, senior vice president, product management, Charles Schwab Investment Management. "[That includes the] Schwab Intelligent Portfolios, our automated investment advisory service that's offered for only the cost of [underlying funds] to investors; and, the ETF version of the Schwab Index Advantage, which uses ETFs to build portfolios, dramatically lowering the costs to employees in retirement plans."

Schwab is also looking at ways to increase the use of ETFs in 401(k)s. If it can truly open up the retirement market, that could be its biggest impact yet.

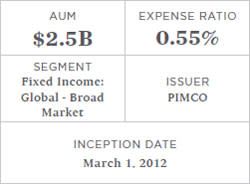

BOND: PIMCO Total Return Active

The launch of the Pimco Total Return ETF (BOND | B) was a turning point for the ETF industry, and not because BOND was the first actively managed ETF to come to market.

BOND was not even PIMCO's first foray into the ETF market—the PIMCO Enhanced Short Maturity Strategy (MINT | B) takes that credit, and it remains the asset manager's largest ETF, with some $4.2 billion in assets as of August 2015.

The turning point was that BOND brought Bill Gross into the ETF space. The world of predominantly passive strategies was now home to a celebrity active manager for the first time.

Gross, widely known as the "bond guru" who founded PIMCO and managed the world's largest bond portfolio—PIMCO's flagship fund—was now also an ETF portfolio manager.

Gross' entry into the fold helped pave the way for other active managers to follow. It also offered a significant endorsement to the ETF wrapper among the alpha-seeking crowd.

The fund, built around the Barclays U.S. Aggregate Index, showed that transparency in active fixed-income portfolios was nothing to be afraid of.

"The Total Return ETF harnesses PIMCO's time-tested investment process and our skills as an active manager, and we believe it signals an important new phase in the development of the ETF marketplace," Bill Gross said at BOND's launch in 2012.

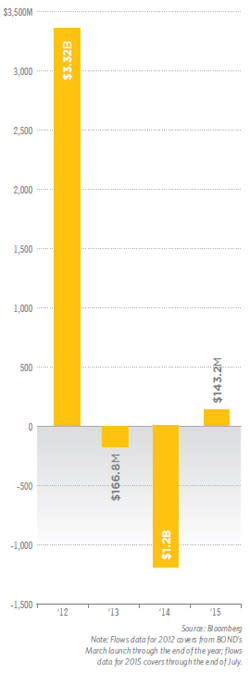

Indeed, BOND was transformative in the active ETF space. In roughly three months, the fund gathered its first $1 billion in assets, making it the most successful active ETF launch ever. Of the 1,700-plus ETFs in the market today, BOND's speed at asset-gathering remains second only to that of the SPDR Gold Trust (GLD|A-100), which reached $1 billion in assets just three days after its launch in 2004.

Perhaps something that helped propel BOND into the investor mainstream—beyond its star-name manager—was the resonance of its ticker.

What's interesting is that when the ETF came to market in March 2012, it was originally listed under the ticker "TRXT." But roughly a month later, Pimco went looking for a more visible name, just to discover that "BOND" hadn't yet been claimed by any issuer. The surprising discovery led to a rebranding that April of what became an icon in the active ETF segment.

Today Scott Mather, Mark Kiesel and Mihir Worah manage the portfolio following Gross' departure to Janus Capital in 2014.