At £16.665, Is easyJet plc (LON:EZJ) A Buy?

easyJet plc (LSE:EZJ), a airlines company based in United Kingdom, saw a significant share price rise of over 20% in the past couple of months on the LSE. With many analysts covering the mid-cap stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. However, could the stock still be trading at a relatively cheap price? Let’s examine easyJet’s valuation and outlook in more detail to determine if there’s still a bargain opportunity. See our latest analysis for easyJet

Is easyJet still cheap?

easyJet is currently overpriced based on my relative valuation model. I’ve used the price-to-equity ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 21.53x is currently well-above the industry average of 8.59x, meaning that it is trading at a more expensive price relative to its peers. In addition to this, it seems like easyJet’s share price is quite stable, which could mean two things: firstly, it may take the share price a while to fall back down to an attractive buying range, and secondly, there may be less chances to buy low in the future once it reaches that value. This is because the stock is less volatile than the wider market given its low beta.

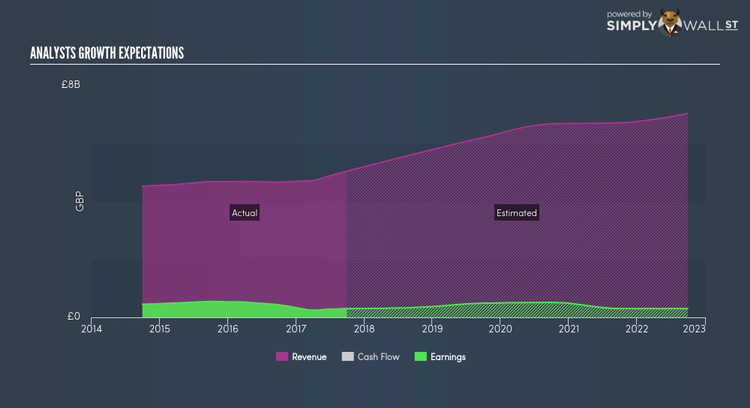

What kind of growth will easyJet generate?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. easyJet’s earnings over the next few years are expected to increase by 70.77%, indicating a highly optimistic future ahead. This should lead to more robust cash flows, feeding into a higher share value.

What this means for you:

Are you a shareholder? It seems like the market has well and truly priced in EZJ’s positive outlook, with shares trading above its fair value. At this current price, shareholders may be asking a different question – should I sell? If you believe EZJ should trade below its current price, selling high and buying it back up again when its price falls towards its real value can be profitable. But before you make this decision, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping tabs on EZJ for some time, now may not be the best time to enter into the stock. The price has surpassed its industry peers, which means it is likely that there is no more upside from mispricing. However, the optimistic prospect is encouraging for EZJ, which means it’s worth diving deeper into other factors in order to take advantage of the next price drop.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on easyJet. You can find everything you need to know about easyJet in the latest infographic research report. If you are no longer interested in easyJet, you can use our free platform to see my list of over 50 other stocks with a high growth potential.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.