3 Great Stocks You Can Buy and Hold Forever

If you want to improve your odds of success in the stock market, all you need to do is buy proven stocks with a solid forward-looking thesis and hold them forever -- also Warren Buffett's "favorite holding period." Just check occasionally to ensure the thesis is intact and you're good to go. While no company is risk-free, owning stocks with sustainable competitive advantages and a visionary management for decades can multiply returns manifold as blips smooth out and compounding works its magic over the years.

If you're wondering where to find such "forever" stocks, start with Brookfield Renewable Partners (NYSE: BEP), Mastercard (NYSE: MA), and 3M (NYSE: MMM).

Clean energy is where the action is

The world is transitioning to clean energy, be it solar, wind, or hydroelectric power. The trend, however, is only picking up, which means owning shares of companies that are investing in renewable assets sounds like a really smart long-term idea. How about investing in one of the world's largest renewable-power generating companies with rock-solid financials and strong dividends to boot? That's Brookfield Renewable Partners, yielding a solid 6.4% at the moment.

Brookfield acquires assets at discounted prices and turns them around to sell power to utilities under regulated, long-term contracts. The company currently owns more than 800 power-generation facilities across North America, South America, Europe, and Asia with nearly 16,300 megawatts of capacity. What intrigues me most is that 82% of its portfolio is composed of hydroelectric power, making Brookfield a dominant play in a niche space.

Buying and holding fundamentally strong stocks forever can make you rich. Image source: Getty Images.

Brookfield's cash flows have grown steadily over the years, largely because 90% of them are contracted. That's been a boon for shareholders, who've seen the company's dividends grow at a compound annual rate of 6% since 2012.

Management has even bigger plans and aims to grow annual dividend by 5%-9% backed by 6%-11% growth in per share funds from operation in the long run -- goals Brookfield believes it can comfortably achieve, thanks to its ongoing efforts to boost margins, targeted annual investment of $600 million-$700 million, and in-built inflation escalators in contracts. Going by the management's track record, I wouldn't hesitate placing my trust on it and the stock for the long haul.

Go cashless to earn more cash

By December 2008, 981 million Mastercard-branded cards had been issued worldwide. The company generated $5 billion in revenue that year from the fees that it earned every time someone swiped its card, and earned an adjusted net income of $1.2 billion (the company took a huge litigation charge that year, hence adjusted earnings).

The number of Mastercard and Maestro-branded cards in circulation had shot up to 2.4 billion by the end of 2017. Mastercard generated $12.5 billion in revenue and earned $3.9 billion net profit last year. Over the period, Mastercard's operating margins crossed 50% and haven't looked back since in at least the last five years.

Image source: Getty Images.

These numbers should give you an idea about the kind of hold Mastercard enjoys in the payments processing industry, as well as its growth potential. In fact, industry experts believe that the global transition from cash to a cashless society is at an inflection point, more so in the Asia-Pacific region where the bulk of transactions are still cash-denominated.

Mastercard, with its expansive network and solid global footprint, is perfectly poised to exploit the opportunities. As a matter of fact, the company's accelerated growth efforts in emerging markets is a step in that direction. It's not an overnight trend -- digital money is a paradigm global shift, one that could make patient investors in stocks like Mastercard really rich.

A multibillion-dollar powerhouse brand

You probably know that Mastercard is a big brand, but what if I tell you 3M is even bigger? Global brand consultancy firm Interbrand valued 3M's brand to be worth nearly $8.9 billion last year versus Mastercard's brand valuation of $6.4 billion.

So what does 3M do to command such brand power? The easiest way to relate to the company is to think of Post-it Notes and Scotch tape, two of 3M's most powerful brands. The company's much bigger, though, selling more than 60,000 products today across the globe, each patented under one of its 100,000-plus patents.

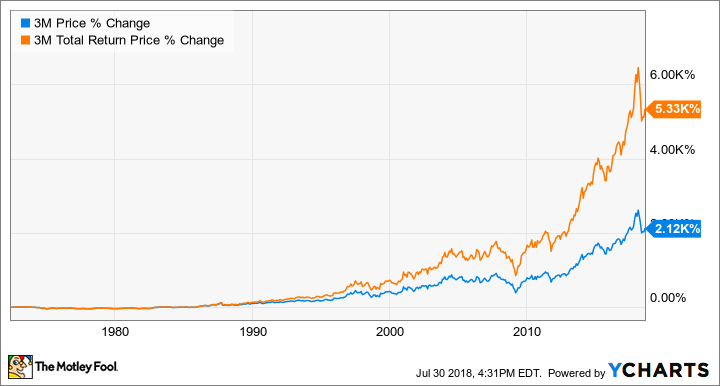

3M's powerful product portfolio generated $31.7 billion in revenue and $4.9 billion in net profit last year, 100% of which was converted into free cash flows. 3M is also a Dividend King, having increased its dividends every year for more than 50 consecutive years. Investors wouldn't have turned millionaires if not for the dividends.

Now, 3M may not have a growth catalyst as easily identifiable as Mastercard's, but 3M's size and reach that goes beyond industrials is unparalleled. To give you an idea about where growth could from, 3M pegs its addressable opportunity in just the new-age markets like electric vehicles, data centers, and advanced healthcare to be worth a whopping $30 billion.

There's a lot to like in 3M's story, one that should continue to play out for decades to come.

More From The Motley Fool

Neha Chamaria has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Mastercard. The Motley Fool recommends 3M. The Motley Fool has a disclosure policy.