3 Overlooked Growth Stocks to Buy for 2019

If you are willing to avoid the glamor stocks and market bellwethers, then there are plenty of investment options open for enterprising investors. In this line of thought, sustainable water technology company Xylem, heating ventilation and air conditioning (HVAC) specialist Ingersoll-Rand, and security products manufacturer Allegion all look like attractive stocks. Let's take a look at why.

Good earnings growth prospects

In a nutshell, all three operate in industries with good long-term prospects, have double-digit earnings growth prospects in 2019, and trade on relatively attractive valuations.

As you can see in the table below, the analyst consensus is for all three to follow up with strong earnings growth in 2018, with another year of double-digit growth in 2018. Moreover, all three are set to significantly increase their free-cash-flow (FCF) generation.

Company | 2017 EPS | 2018 Estimated EPS | 2019 Estimated EPS |

|---|---|---|---|

Xylem (NYSE: XYL) | $2.40 | $2.89 | $3.38 |

Ingersoll-Rand (NYSE: IR) | $4.50 | $5.60 | $6.32 |

Allegion (NYSE: ALLE) | $3.78 | $4.48 | $4.96 |

Data source: FactSet Research. EPS = earnings per share.

It's one thing to generate good growth in the upcycle of a strong economy, but can these companies be trusted to continue growing over the long term? I think the answer is a qualified yes.

A sustainable water stock

The investment case for Xylem centers on the idea that emerging markets have a need to build out water infrastructure and improve water quality. Meanwhile, there's also a need in developed markets to replace aging infrastructure, particularly as more rigorous environmental standards take effect.

Moreover, Xylem is expanding into smart meters and infrastructure analytics solutions, and this should help spur spending from utilities keen to reduce leakage and theft from their water networks. Management's medium-term forecast calls for 4% to 6% organic revenue growth, with margin expansion leading to earnings growth in the mid-teens.

Image source: Getty Images.

It isn't just about end markets, though, because thanks to internal productivity improvements and the better cash-generating profile of smart technology, Xylem expects to start generating more FCF in the future. Expectations are for 115% conversion of net income into FCF for 2018, and based on my calculations, this puts Xylem at a price-to-FCF multiple of 20 times. That's a good value for a company with mid-teens earnings growth prospects.

Ingersoll-Rand continues its strong run

The case for buying HVAC specialist Ingersoll-Rand relates to its ongoing margin expansion, strong order book, and improved cash-generation profile. It's all backed by solid growth prospects coming from the emergence of an HVAC-hungry middle class in emerging markets. In addition, the focus of global growth is shifting toward countries with hotter climates. Meanwhile, by being a more energy-efficient solution provider, Ingersoll-Rand can help localities relieve the stress on electricity grids caused by power-hungry HVAC equipment.

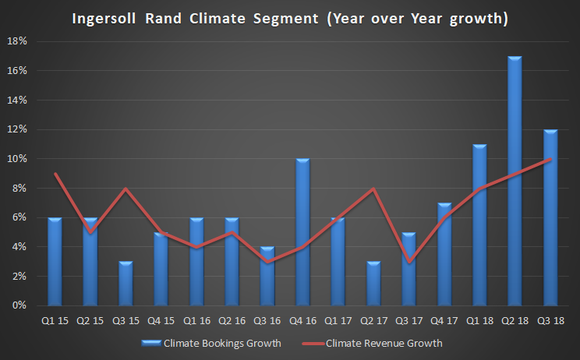

As you can see in the chart below, outstanding bookings growth in 2018 sets the company up for another year of good growth in 2019.

Data source: Ingersoll-Rand presentations. Chart by author.

Meanwhile, internal improvements in FCF generation and ongoing margin expansion underpin the company's valuation.

IR Free Cash Flow (TTM) data by YCharts

Management expects 100% FCF conversion from adjusted net income in 2018, and based on my calculations, the stock trades at around 16 times its 2018 FCF, which is too cheap for a company with double-digit earnings growth prospects.

Allegion is finally a good value

The lock security company -- which, incidentally, was spun out of Ingersoll-Rand in 2013 -- undoubtedly is attractive to investors looking for a good long-term theme to invest in, but it's one of those stocks that investors often take a look at only to slouch away moaning about valuation.

However, after a year of flat stock performance, but good earnings and FCF growth, the stock has finally moved into a good value range.

ALLE Price to Free Cash Flow (TTM) data by YCharts.

Allegion is attractive because it's the leading player in the convergence of electronic and mechanical locks. Adoption of electronic locks and security with connected technology is a key feature of the movement toward smart homes. Meanwhile, in the commercial market, using web-enabled technologies, companies can now remotely configure and monitor locks, while adding and deleting who has access to specific areas -- a key benefit in improving productivity and security.

Management sees revenue growth in the mid single-digits accompanied by margin expansion and double-digit earnings growth. Meanwhile, Allegion is on track for available FCF of $380 million to $400 million in 2018, putting it on a price-to-FCF multiple of slightly less than 20 times. Again, that's a good value for a company with such good secular growth prospects.

Stocks to buy?

All three companies trade on good valuations and have strong long-term growth prospects. They may not be the best-known companies out there, but sometimes buying under-the-radar and overlooked stocks is the best way to generate good returns.

More From The Motley Fool

Lee Samaha owns shares of Ingersoll-Rand. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.