3 Reasons to Hold Inspire Medical (INSP) Stock in Your Portfolio

Inspire Medical Systems, Inc. INSP is well-poised for growth in the coming quarters, courtesy of its product innovations. The optimism led by a solid first-quarter 2023 performance and a few regulatory approvals are expected to contribute further. However, concerns regarding overdependence on the Inspire system and stiff competition persist.

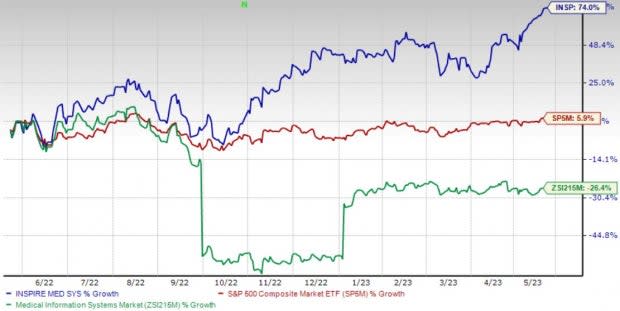

Over the past year, this Zacks Rank #3 (Hold) stock has gained 74.1% against the industry’s 26.4% decline and the S&P 500's 5.9% growth.

The renowned medical technology company focused on obstructive sleep apnea (OSA) has a market capitalization of $8.99 billion. The company projects 26.3% growth for 2023 and expects to maintain its strong performance. Inspire Medical delivered an earnings surprise of 43.3% for the past four quarters, on average.

Image Source: Zacks Investment Research

Let’s delve deeper.

Product Innovation: We are optimistic about Inspire Medical’s commitment to driving innovation, which has allowed it to achieve continuous, significant improvements in its Inspire therapy. On the first-quarter earnings call, management confirmed that the company had been continuing operational and production qualification as well as integration with the Inspire digital tools, specifically sleep sync.

On the same call, management also stated that Inspire Medical’s SleepSync system continues to progress well since the launch of the Bluetooth-enabled patient remote.

Regulatory Approvals: We are upbeat about Inspire Medical’s receipt of a slew of FDA approvals over the past few months. In March, the company received the FDA’s approval to offer Inspire therapy to pediatric patients with Down syndrome. The same month, Inspire Medical announced that it had received countrywide reimbursement approval in Belgium, effective immediately, at rates consistent with other countries around the world for the Inspire therapy.

Strong Q1 Results: Inspire Medical’s solid first-quarter 2023 results buoy our optimism. The company recorded a robust improvement in the top line and strength in year-over-year geographic results. Activation of new U.S. centers and the creation of new U.S. sales territories were also recorded during the reported quarter.

Downsides

Overdependence on the Inspire System: Sales of Inspire Medical’s Inspire system accounted for primarily all its revenues in the past few years. The company’s ability to execute its growth strategy and become profitable will, therefore, depend upon the adoption of the Inspire therapy to treat moderate-to-severe OSA in patients who are unable to use or get consistent benefits from continuous positive airway pressure. Management cannot ensure that the company’s Inspire therapy will achieve or maintain broad market acceptance among physicians and patients.

Stiff Competition: The medical technology industry is highly competitive, subject to change and significantly affected by new product introductions and other activities of industry participants. Inspire Medical’s competitors have historically dedicated and will continue to dedicate significant resources to promote their products or develop new products or methods to treat moderate-to-severe OSA.

Estimate Trend

Inspire Medical has been witnessing a positive estimate revision trend for 2023. In the past 90 days, the Zacks Consensus Estimate for loss per share has narrowed from $1.32 to $1.18.

The Zacks Consensus Estimate for the company’s second-quarter 2023 revenues is pegged at $137.5 million, suggesting a 50.5% improvement from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Hologic, Inc. HOLX, Merit Medical Systems, Inc. MMSI and Boston Scientific Corporation BSX.

Hologic, carrying a Zacks Rank #2 (Buy) at present, has an estimated growth rate of 5.1% for fiscal 2024. HOLX’s earnings surpassed estimates in all the trailing four quarters, the average being 27.3%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Hologic has gained 3.3% compared with the industry’s 2.3% rise in the past year.

Merit Medical, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 11%. MMSI’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 20.2%.

Merit Medical has gained 39.7% compared with the industry’s 7.5% rise over the past year.

Boston Scientific, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 11.5%. BSX’s earnings surpassed estimates in two of the trailing four quarters and missed in the other two, the average surprise being 1.9%.

Boston Scientific has gained 34.5% against the industry’s 29.6% decline over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boston Scientific Corporation (BSX) : Free Stock Analysis Report

Hologic, Inc. (HOLX) : Free Stock Analysis Report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report

Inspire Medical Systems, Inc. (INSP) : Free Stock Analysis Report