3 Reasons to Retain OPKO Health (OPK) Stock in Your Portfolio

OPKO Health, Inc. OPK is well-poised for growth in the coming quarters, courtesy of its potential in RAYALDEE. The optimism led by solid third-quarter 2022 performance, along with a few regulatory approvals, is expected to contribute further. Forex woes and concerns regarding overdependence on RAYALDEE persist.

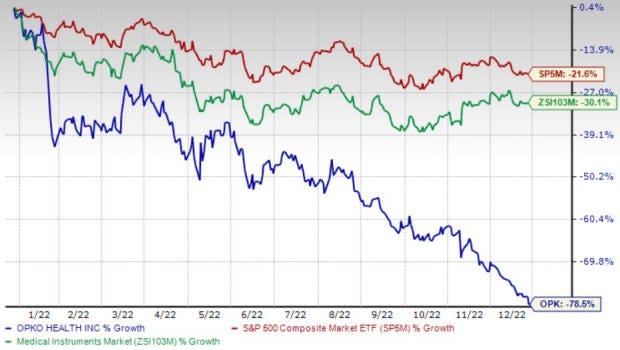

Over the past year, this Zacks Rank #3 (Hold) stock has lost 78.5% compared with 30.2% decline of the industry and 21.6% fall of the S&P 500.

This renowned multinational biopharmaceutical and diagnostics company has a market capitalization of $826.8 million. It projects 23.3% growth for 2023 and expects to maintain its strong performance. OPKO Health’s P/B ratio of 0.5 compares favorably with the industry’s 2.5.

Image Source: Zacks Investment Research

Let’s delve deeper.

Potential in RAYALDEE: We are upbeat about OPKO Health’s RAYALDEE business. During the third quarter of 2022, OPKO Health began to receive royalty payments from sales of RAYALDEE by CSL Vifor in Germany and Switzerland. The company expects these payments to increase as CSL Vifor launches RAYALDEE in additional territories throughout Europe.

In February, OPKO Health announced that Vifor Fresenius Medical Care Renal Pharma had initiated the commercial launch of RAYALDEE (extended-release calcifediol) in Germany.

Regulatory Approvals: We are optimistic about OPKO Health’s progress on the regulatory front for its products. In February, the company and Pfizer Inc. gained marketing authorization from the European Commission for the next-generation long-acting recombinant human growth hormone NGENLA (somatrogon).

At the time of third-quarter 2022 earnings release, OPKO Health confirmed that NGENLA is the first once-weekly product approved for the treatment of pediatric growth hormone deficiency in Japan, Canada, Australia, Taiwan, UAE and Brazil.

Strong Q3 Results: OPKO Health’s better-than-expected third-quarter 2022 revenues buoy our optimism. OPKO Health’s buyout of ModeX Therapeutics, Inc. continues to benefit it as the latter progresses its proprietary immunotherapy pipeline, raising our optimism. The company’s continued strength in its women's health and oncology businesses also augurs well.

Downsides

Forex Woes: OPKO Health derives a significant portion of its consolidated net revenues from international sales, which subject the company to risks relating to fluctuations in currency exchange rates. The company, through its subsidiaries, operates in a wide variety of jurisdictions. Certain countries in which it operates or may operate have experienced geopolitical instability, economic problems and other uncertainties from time to time.

Overdependence on RAYALDEE: OPKO Health’s RAYALDEE is the company’s only pharmaceutical product approved for marketing in the United States. The company’s ability to generate revenues from product sales and achieve profitability is substantially dependent on its ability to effectively commercialize RAYALDEE. The failure to successfully commercialize RAYALDEE would have a material adverse effect on the company’s business.

Estimate Trend

OPKO Health is witnessing a negative estimate revision trend for 2022. In the past 90 days, the Zacks Consensus Estimate for its earnings has widened from a loss of 38 cents per share to a loss of 43 cents.

The Zacks Consensus Estimate for the company’s fourth-quarter 2022 revenues is pegged at $168.1 million, suggesting a 58.1% fall from the year-ago quarter’s reported number.

This compares to our fourth-quarter 2022 revenue estimate of $166.5 million, suggesting a 58.5% decline from the year-ago quarter’s reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Exact Sciences Corporation EXAS, ShockWave Medical, Inc. SWAV and Merit Medical Systems, Inc. MMSI.

Exact Sciences, carrying a Zacks Rank #2 (Buy) at present, has an estimated long-term growth rate of 27.5%. EXAS’ earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missed the same in one, the average beat being 0.6%.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Exact Sciences has lost 32.2% compared with the industry’s 24.2% decline in the past year.

ShockWave Medical, carrying a Zacks Rank #2 at present, has an estimated growth rate of 22.2% for 2023. SWAV’s earnings surpassed estimates in all the trailing four quarters, the average beat being 146.1%.

ShockWave Medical has gained 17.9% against the industry’s 30.2% decline over the past year.

Merit Medical, carrying a Zacks Rank #2 at present, has an estimated long-term growth rate of 11%. MMSI’s earnings surpassed estimates in all the trailing four quarters, the average beat being 25.4%.

Merit Medical has gained 9.5% against the industry’s 12.5% decline over the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Merit Medical Systems, Inc. (MMSI) : Free Stock Analysis Report

OPKO Health, Inc. (OPK) : Free Stock Analysis Report

Exact Sciences Corporation (EXAS) : Free Stock Analysis Report

ShockWave Medical, Inc. (SWAV) : Free Stock Analysis Report