3 Top Stocks in Energy

For a lot of investors, energy stocks can be a tough nut to crack. So many people -- those on Wall Street included -- build an incredible amount of their investment theses on the direction of oil prices in a year or so. For anyone with a long-term investment horizon, rethinking their oil strategy every few months is too much work and hardly worth the effort.

Fortunately, that isn't the only investment strategy for the energy industry. There's a collection of companies in this space that fit the mold of a long-term buy and hold stock. If this is the kind of investment you want to make in energy, then here's why you should check out Magellan Midstream Partners (NYSE: MMP), Total (NYSE: TOT), and First Solar (NASDAQ: FSLR).

Image source: Getty Images.

Stability and growth in one tidy package

There's a widely held belief that investing in oil and gas is a business akin to the wild west, where only those with iron stomachs can handle the volatility. Sure, there are parts of the industry like this where a few-dollar change in the price for a barrel of oil can mean the difference between riches and ruin. That doesn't mean that every investment in this business has to be this way.

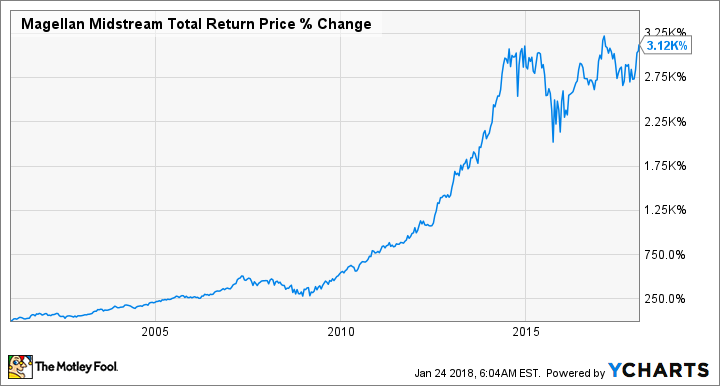

For those who want a stable, reliable investment in the oil and gas industry, take a look at Magellan Midstream Partners. As a pipeline, processing, and logistics company, Magellan's business is largely insulated from commodity prices. According to management, around 85% of its revenue comes from fixed fees it gets for leasing space in its pipelines or storage facilities. With so much of its revenue more or less locked in, management gets a steady cash flow with which it can pay a hefty distribution to its shareholders, as well as fund future growth.

The company's recipe of high revenue visibility through fixed-fee contracts, steady growth by bringing new assets into operation, and not relying too much on outside capital to meet its funding -- a rarity among pipeline companies -- has translated into incredible returns for its shareholders since its IPO back in 2001.

MMP Total Return Price data by YCharts.

Wall Street hasn't been too fond of the company's stock ever since oil prices started to crash back in 2014, but the company's financial performance has barely skipped a beat as both earnings before interest, taxes, depreciation, and amortization (EBITDA) and distributable cash flow have steadily grown since the downturn started. With a distribution yield of 4.8% and management's intention to grow that payout by 8% annually for the next couple of years, Magellan is a great slow-and-steady investment in a seemingly volatile industry.

A plan for today and tomorrow

We're in an incredibly interesting time for energy companies. While fossil fuels remain the dominant energy source globally, alternative sources, such as wind and solar, have become less expensive and will likely start clawing away at market share for the foreseeable future. For large energy companies that make investments based on decade-long time horizons, it's at the point where it's impossible to ignore the threat -- or opportunity -- that alternative energy poses to the global energy landscape.

For investors who want a slice of both pies, integrated oil and gas company Total is an intriguing pick. The company generates some of the best returns on equity among its Big Oil peers, so investors are getting an investment that can generate solid profits to support its enticing dividend yield of 4.8%. Over the past couple of years, the company has been building an oil strategy that should ensure profitability at oil prices as low as $50 a barrel, which should set it up nicely over the next decade.

What sets Total apart from its peers is its commitment to building a business ready for a life after oil. While just about every big oil company has some form of alternative-energy investment or strategy, Total is one of the few that has rigorous expectations for rates of return and free cash flow from those investments. By 2020, it intends to generate $500 million in free cash flow from its power generation and alternative-energy assets. That offering -- returns now from oil and gas with a plan for profitability from alternative energy -- is a rare thing in the energy world today, and something worth considering for your portfolio.

MMP Total Return Price data by YCharts.

The future is bright

As I mentioned, the economics for solar energy are getting better and better by the day, and it's not hard to envision a world where solar, wind, and some form of energy storage become the dominant power source. For investors who have a vision for the future, solar-panel manufacturer First Solar is one to watch.

One could get caught up putting a lot of emphasis on the Trump administration's decision to put import tariffs on solar panels, but the current tariff structure is a short-term thing that will expire in four years. For anyone looking to make an investment in a long-term trend, like completely changing our energy production, four years in only one market is small marbles. Instead, let's focus on First Solar as a business, and how it can capture these long-term tailwinds.

One thing that First Solar has going for it over so many other solar companies is a management team with a track record of generating returns and maintaining capital discipline. While most of its peers rely heavily on debt to juice returns, First Solar is almost completely debt free and has a war chest of $2 billion to deploy toward investments in new technology or expanding production. That kind of flexibility is a huge competitive advantage in an industry that consistently needs to reinvest in new technology and a product that rapidly commoditizes.

If there's one threat to First Solar, it's that the company's solar panel technology -- thin film versus more conventional crystalline silicon -- has lower efficiency ratings. First Solar has held an advantage over other technologies because its thin-film tech has been less expensive, and the difference in field efficiency isn't as pronounced as efficiency tests in the lab.

Still, if the company wants to remain competitive, it will need to invest in boosting panel efficiency. That isn't anything new, though, as the company has boosted its lab-tested cells from 17% in 2010 to 22%. As long as First Solar can keep making small efficiency gains, remain a low-cost supplier, and maintain capital discipline, it should remain a great investment in the solar business.

More From The Motley Fool

Tyler Crowe owns shares of First Solar, Magellan Midstream Partners, and Total. The Motley Fool recommends First Solar and Magellan Midstream Partners. The Motley Fool has a disclosure policy.