Advanced Micro Devices (AMD) Q1 Preview: Can Shares Return to Former Glory?

Stocks tumbled again last Friday to close out a tough week in the market. To put it simply, it was a pretty brutal April month all around. Perhaps, the old saying “April showers bring May flowers” can be valid for the investing world and bring us a prosperous month.

It’s a fresh week. Investors will be pivoting their focus to the Federal Open Market Committee’s (FOMC) announcement on Wednesday; the consensus is that the Fed will be raising rates by 50 basis points. While this rate hike is critical, the real focus will be on what the Fed plans moving forward in the summer meetings.

In the meantime, earnings season rolls on. We’ve witnessed adverse market reactions to quarterly releases, which is usually not the case. Economic concerns and geopolitical issues have undoubtedly weighed heavily on investor sentiment.

On deck to report quarterly results tomorrow after the market closes is the big semiconductor player Advanced Micro Devices AMD. The chart below illustrates the year-to-date performance of AMD and two other chip names – Nvidia Corporation NVDA and ON Semiconductor Group ON – while comparing the S&P 500 as well.

Image Source: Zacks Investment Research

As we can see, it’s been a tough stretch in the semiconductor space. AMD has had the worst 2022 performance, followed closely by NVDA. In fact, none of the companies have managed to even come close to the S&P 500's performance. The semiconductor shortage has added fuel to this fire sale.

Stretching out the time frame over the past year, we can see that nearly all three companies’ shares took a downwards trajectory around December 2021. Though 2022 hasn’t been kind, all three companies have managed to outpace the S&P 500 thanks to their nearly year-long run in 2022.

Image Source: Zacks Investment Research

Previous Share Reactions

AMD has exceeded EPS estimates over its last six quarterly reports. However, the share price has only moved upwards twice over this timeframe; shares rose 7.5% following its latest earnings release and 6.6% in its July 2021 earnings release. The company’s four-quarter trailing average EPS surprise sits at a respectable 17%.

When share price rallied following the quarterly reports, AMD exceeded EPS expectations by at least 20% in both instances. To me, it seems an extensive EPS beat may be needed to fuel another rally for shares. Additionally, with the weakness in the semiconductor space throughout 2022, investors will most likely react adversely to any EPS or revenue miss.

Q4 2021 Earnings

AMD reported quarterly record revenue of $4.8 billion in its latest earnings report, up 49% year-over-year and 12% quarter-over-quarter. It also had robust quarterly profitability; gross margin was 50%, and operating income tallied $1.2 billion.

In its computing and graphics segment, revenue was up 32% year-over-year, driven by its RyzenTM and RadeonTM processor sales. Within the company’s enterprise, embedded, and semi-custom segment, revenue tallied $2.2 billion, boosted by higher EPYCTM and semi-custom processor sales.

AMD witnessed strong demand for premium desktop and notebook PCs built with their impressive Ryzen 5000 processors and announced new Ryzen processors with AMD 3D V-Cache technology to power an unparalleled gaming experience. Additionally, AMD had a higher average selling price for its products throughout the quarter, driven by a richer mix of Ryzen processor and Radeon product sales.

Moving forward, AMD expects robust demand across both segments due to its cutting-edge technology and its established stance in the booming gaming industry. Furthermore, the company is benefitting majorly from the digital shift we’ve undergone since COVID-19 took the world by storm.

EPS & Revenue Estimates

The Zacks Consensus Estimate for Q1 earnings sits at $0.91 per share, reflecting stellar earnings growth in the double-digits at 75% from the year-ago quarter. Additionally, the Consensus Estimate trend has remained unchanged over the last 60 days, though one analyst recently upgraded their quarterly estimate. Notably, zero analysts have downgraded their estimates in this timeframe.

Q1 sales estimates are looking strong as well; the $5 billion consensus revenue estimate represents a sizable top-line expansion of 45% from the year-ago quarter. Additionally, AMD provided uplifting revenue guidance for 2022, held down by robust growth across all businesses.

ON Semiconductor & Nvidia Comparison

ON Semiconductor ON is a leading supplier of power and analog semiconductors and sensors. Before the market opened today, ON reported its quarterly results; the company reported EPS of $1.22 and quarterly revenue of $1.9 billion, fueling shares to gain nearly 4% in the pre-market session.

ON Semiconductor Corporation Price, Consensus and EPS Surprise

ON Semiconductor Corporation price-consensus-eps-surprise-chart | ON Semiconductor Corporation Quote

Nvidia Corporation NVDA is the worldwide leader in visual computing technologies and the inventor of the graphic processing unit (GPU). The Zacks Consensus Estimate Trend for NVDA’s upcoming quarter has retraced marginally over the last 60 days, now displaying quarterly earnings of $1.29 per share.

Nvidia’s quarterly EPS estimate displays a notable 43% year-over-year growth in earnings, and the $8.1 billion consensus revenue estimate easily beats out NVDA’s year-ago quarterly sales of $5.6 billion by close to 45%.

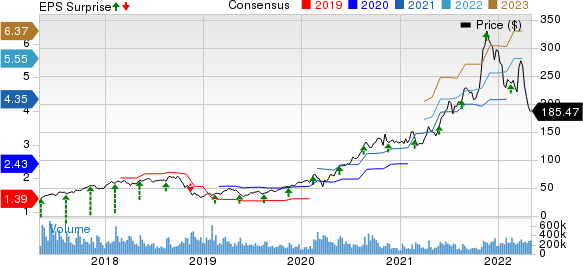

NVIDIA Corporation Price, Consensus and EPS Surprise

NVIDIA Corporation price-consensus-eps-surprise-chart | NVIDIA Corporation Quote

These semiconductor companies are still posting and forecasting strong year-over-year growth rates, which bodes well for AMD heading into tomorrow.

Bottom Line

A highly unanticipated level of demand for microchips during the pandemic caused the supply chain to fall completely out of equilibrium. Blending the chip shortage into a volatile market environment with rising borrowing rates and surging energy costs has undoubtedly fueled the poor 2022 share performance.

However, microchips are a staple in our everyday lives, whether we realize it or not. Nearly every piece of technology requires a microchip to function correctly, and this trend isn’t going anywhere anytime soon as we continuously become more dependent on them.

Quarterly estimates and year-over-year growth rates are looking solid. This, paired with AMD’s strong demand across nearly all products, gives me an optimistic view of the company heading into its quarterly release. It is important that investors are aware of current market sentiment, as a robust earnings does not guarantee anything as we've seen so far in 2022. Still, semiconductor companies will benefit massively in the long-term.

AMD is currently a Zacks Rank #3 (Hold) with an overall VGM Score of an A.

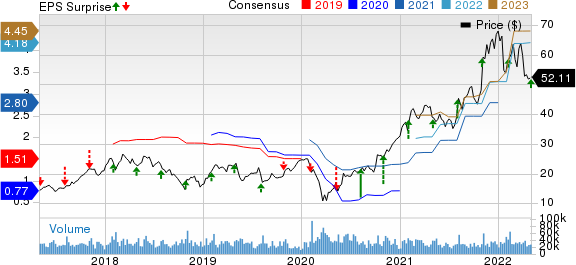

Advanced Micro Devices, Inc. Price, Consensus and EPS Surprise

Advanced Micro Devices, Inc. price-consensus-eps-surprise-chart | Advanced Micro Devices, Inc. Quote

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

ON Semiconductor Corporation (ON) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research