Aflac Q2 Preview: Can the Earnings Streak Continue?

The Zacks Finance Sector has undergone turbulence year-to-date, declining approximately 13.5% in value vs. the S&P 500’s 15% decline.

One such company residing in the sector, Aflac AFL, is on deck to report quarterly results on Monday, August 1st, after market close. Aflac is an American insurance company and a massive supplier of supplemental insurance within the U.S.

In addition, the company currently carries a Zacks Rank #3 (Hold) with an overall VGM Score of a B.

How do things look for the insurance titan heading into its quarterly release? Let’s take a closer look.

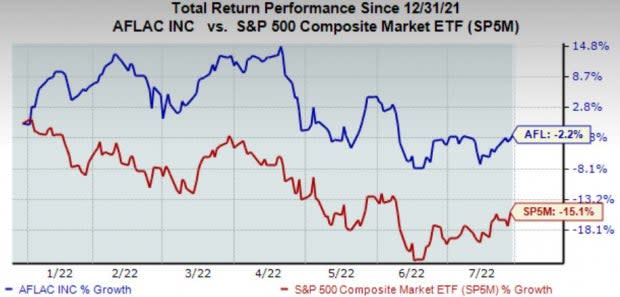

Share Performance & Valuation

Year-to-date, Aflac shares have been highly defensive in nature relative to the S&P 500, declining a modest 2%.

Image Source: Zacks Investment Research

Over the last three months, Aflac shares have primarily remained stagnant, declining a marginal 0.9% vs. the S&P 500’s decline of 2.3%.

Image Source: Zacks Investment Research

In addition, Aflac shares could be undervalued, as displayed by its Style Score of an A for Value.

The company’s forward earnings multiple resides at an enticing 10.7X, nicely below its five-year median of 11.3X and representing a substantial 27% discount relative to its Zacks Finance Sector.

Image Source: Zacks Investment Research

Quarterly Estimates

Analysts have been overwhelmingly bearish over the last 60 days, lowering their outlook for not just the quarter to be reported but across all timeframes.

Image Source: Zacks Investment Research

The Zacks Consensus EPS Estimate for the quarter sits at $1.29, penciling in a disheartening 18% decline in quarterly earnings year-over-year.

The top-line is also displaying weakness; Aflac is forecasted to generate $4.8 billion in revenue for the quarter, notching a 14% decline from year-ago quarterly sales of $5.6 billion.

Quarterly Performance & Market Reactions

Aflac has been on a blazing-hot earnings streak, exceeding bottom-line estimates in 21 consecutive quarters – undoubtedly impressive. Just in its latest quarter, the company recorded a 3% bottom-line beat.

Top-line results have also been solid – Aflac has posted better-than-expected sales results in seven of its previous ten quarters. The chart below illustrates the company’s revenue on a quarterly basis.

Image Source: Zacks Investment Research

In addition, the market has had mixed reactions following its last six quarterly reports, with shares moving upwards three times and downwards three times.

Bottom Line

Aflac shares have been highly defensive in 2022, a significant positive amidst the deep valuation slashes across many industries.

In addition, the insurance giant boasts rock-solid valuation levels and has repeatedly posted better-than-expected quarterly results, another plus.

However, both the top and bottom-lines are forecasted to decline by double-digit percentages, analysts have been bearish, and the market has had mixed reactions to the company’s quarterly reports as of late.

Heading into the quarterly report, Aflac AFL has an Earnings ESP Score of -1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Aflac Incorporated (AFL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research