Alliance Data Systems (NYSE:ADS) Has A Somewhat Strained Balance Sheet

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Alliance Data Systems Corporation (NYSE:ADS) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Alliance Data Systems

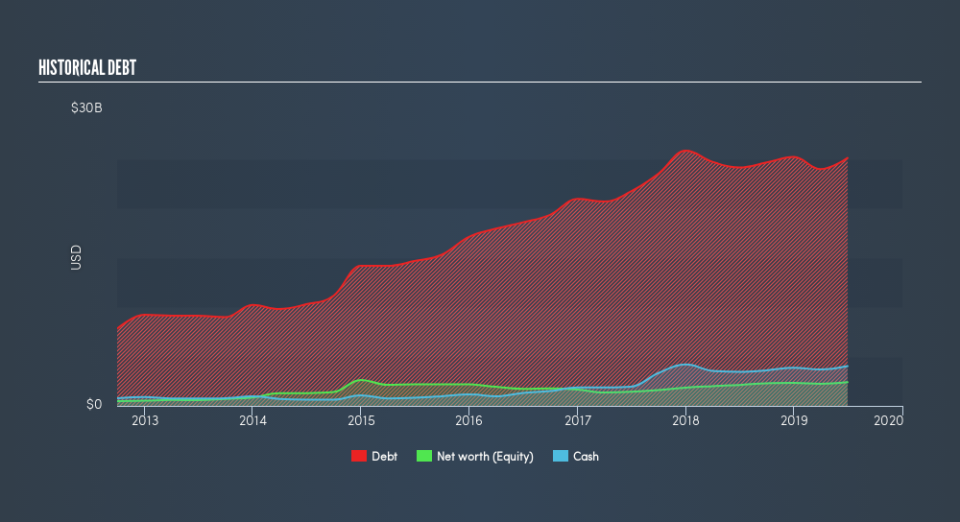

How Much Debt Does Alliance Data Systems Carry?

As you can see below, Alliance Data Systems had US$25.1b of debt, at June 2019, which is about the same the year before. You can click the chart for greater detail. However, it does have US$4.03b in cash offsetting this, leading to net debt of about US$21.0b.

A Look At Alliance Data Systems's Liabilities

We can see from the most recent balance sheet that Alliance Data Systems had liabilities of US$351.4m falling due within a year, and liabilities of US$28.0b due beyond that. Offsetting these obligations, it had cash of US$4.03b as well as receivables valued at US$354.2m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$24.0b.

This deficit casts a shadow over the US$8.12b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Alliance Data Systems would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Alliance Data Systems has a rather high debt to EBITDA ratio of 12.6 which suggests a meaningful debt load. However, its interest coverage of 5.0 is reasonably strong, which is a good sign. Importantly Alliance Data Systems's EBIT was essentially flat over the last twelve months. We would prefer to see some earnings growth, because that always helps diminish debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Alliance Data Systems can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, Alliance Data Systems actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

To be frank both Alliance Data Systems's net debt to EBITDA and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Once we consider all the factors above, together, it seems to us that Alliance Data Systems's debt is making it a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. Over time, share prices tend to follow earnings per share, so if you're interested in Alliance Data Systems, you may well want to click here to check an interactive graph of its earnings per share history.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.