Is Alliant Energy (NASDAQ:LNT) A Risky Investment?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Alliant Energy Corporation (NASDAQ:LNT) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Alliant Energy

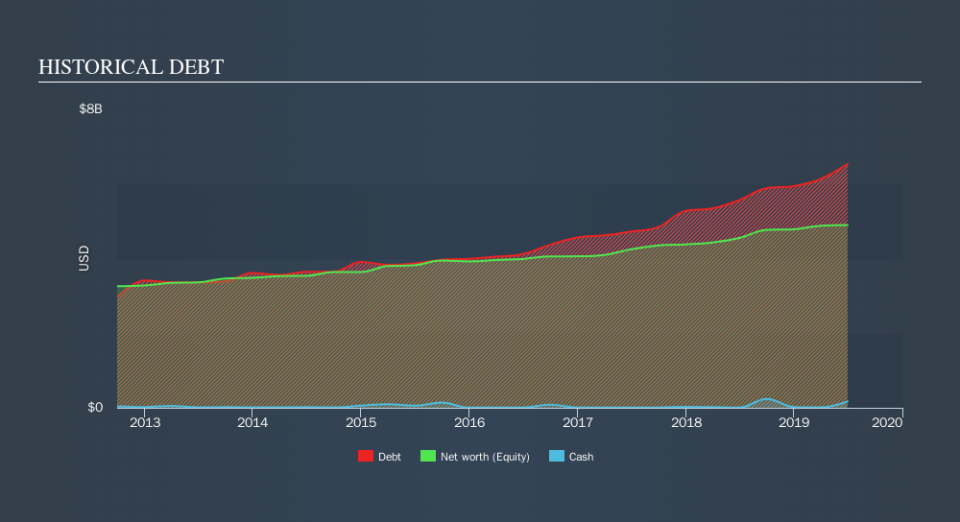

What Is Alliant Energy's Net Debt?

The image below, which you can click on for greater detail, shows that at June 2019 Alliant Energy had debt of US$6.54b, up from US$5.57b in one year. On the flip side, it has US$170.2m in cash leading to net debt of about US$6.37b.

How Healthy Is Alliant Energy's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Alliant Energy had liabilities of US$1.95b due within 12 months and liabilities of US$9.27b due beyond that. On the other hand, it had cash of US$170.2m and US$421.5m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$10.6b.

This deficit is considerable relative to its very significant market capitalization of US$12.7b, so it does suggest shareholders should keep an eye on Alliant Energy's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Alliant Energy has a rather high debt to EBITDA ratio of 5.1 which suggests a meaningful debt load. However, its interest coverage of 2.5 is reasonably strong, which is a good sign. Fortunately, Alliant Energy grew its EBIT by 2.3% in the last year, slowly shrinking its debt relative to earnings. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Alliant Energy can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Alliant Energy saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both Alliant Energy's net debt to EBITDA and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. Having said that, its ability to grow its EBIT isn't such a worry. We should also note that Electric Utilities industry companies like Alliant Energy commonly do use debt without problems. Overall, it seems to us that Alliant Energy's balance sheet is really quite a risk to the business. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Alliant Energy's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.