American Lorain Corporation (ALN): Time For A Financial Health Check

Investors are always looking for growth in small-cap stocks like American Lorain Corporation (AMEX:ALN), with a market cap of USD $10.33M. However, an important fact which most ignore is: how financially healthy is the company? There are always disruptions which destabilize an existing industry, in which most small-cap companies are the first casualties. Thus, it becomes utmost important for an investor to test a company’s resilience for such contingencies. In simple terms, I believe these three small calculations tell most of the story you need to know. See our latest analysis for ALN

Does ALN generate an acceptable amount of cash through operations?

While failure to manage cash has been one of the major reasons behind the demise of a lot of small businesses, mismanagement comes into the light during tough situations such as an economic recession. Furthermore, failure to service debt can hurt its reputation, making funding expensive in the future. Can ALN pay off what it owes to its debtholder by using only cash from its operational activities? ALN’s recent operating cash flow was -0.57 times its debt within the past year. This means what ALN can generate on an annual basis, which is currently a negative value, does not cover what it actually owes its debtors in the near term. This raises a red flag, looking at ALN’s operations at this point in time.

Can ALN pay its short-term liabilities?

What about its commitments to other stakeholders such as payments to suppliers and employees? During times of unfavourable events, ALN could be required to liquidate some of its assets to meet these upcoming payments, as cash flow from operations is hindered. We should examine if the company’s cash and short-term investment levels match its current liabilities. Our analysis shows that ALN is unable to meet all of its upcoming commitments with its cash and other short-term assets. While this is not abnormal for companies, as their cash is better invested in the business or returned to investors than lying around, it does bring about some concerns should any unfavourable circumstances arise.

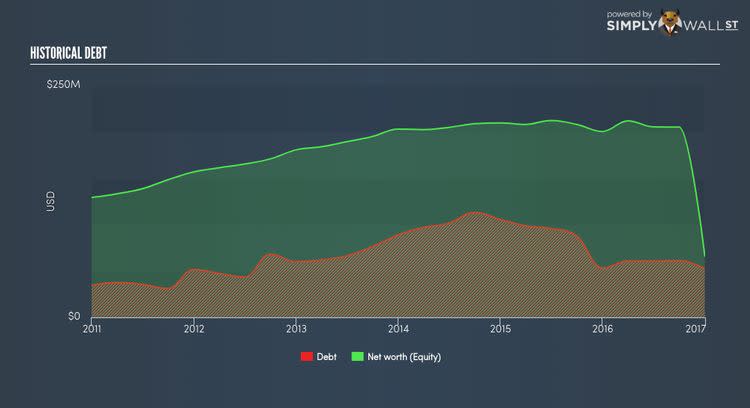

Does ALN face the risk of succumbing to its debt-load?

A substantially higher debt poses a significant threat to a company’s profitability during a downturn. In the case of ALN, the debt-to-equity ratio is 79.62%, which indicates that its debt can cause trouble for the company in a downturn but it is still at a manageable level.

Next Steps:

Are you a shareholder? ALN’s debt and cash flow levels indicate room for improvement. Its cash flow coverage of less than a quarter of debt means that operating efficiency could be an issue. Furthermore, the company may struggle to meet its near term liabilities should an adverse event occur. Given that its financial position may change. You should always be keeping on top of market expectations for ALN’s future growth on our free analysis platform.

Are you a potential investor? ALN’s large debt ratio on top of low cash coverage of debt in addition to low liquidity coverage of near-term expenses may not build the strongest investment case. Though, keep in mind that this is a point-in-time analysis, and today’s performance may not be representative of ALN’s track record. As a following step, you should take a look at ALN’s past performance analysis on our free platform to figure out ALN’s financial health position.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.