Americans have more debt than ever — and it's creating an economic trap

REUTERS/Andrew Winning

An International Monetary Fund report finds that high levels of household debt deepen and prolong recessions.

US household debt is at pre-Great Recession levels.

Household debt jumped by over $500 billion in the second quarter to $12.84 trillion.

A scary little statistic is buried beneath the US economy's apparent stability: Consumer-debt levels are now well above those seen before the Great Recession.

As of June, US households were more than half a trillion dollars deeper in debt than they were a year earlier, according to the latest figures from the Federal Reserve. Total household debt now totals $12.84 trillion — also, incidentally, about two-thirds of gross domestic product.

The proportion of overall debt that was delinquent in the second quarter was steady at 4.8%, but the New York Fed warned over transitions of credit-card balances into delinquency, which "ticked up notably."

Here's the thing: Unlike government debt, which can be rolled over continuously, consumer loans actually need to be paid back. And despite low official interest rates from the Federal Reserve, those often do not trickle down to financial products like credit cards and small-business loans.

Michael Lebowitz, the cofounder of the market-analysis firm 720 Global, says the US economy is already dangerously close to the edge.

"Most consumers, especially those in the bottom 80%, are tapped out," he told Business Insider. "They have borrowed about as much as they can. Servicing this debt will act like a wet towel on economic growth for years to come. Until wages can grow faster than our true costs of inflation, this problem will only worsen."

The International Monetary Fund devotes two chapters of its latest Global Financial Stability Report to the issue of household debt. It finds that, rather intuitively, high debt levels tend to make economic downturns deeper and more prolonged.

"Increases in household debt consistently [signal] higher risks when initial debt levels are already high," the IMF says.

Nonetheless, the results indicate that the threshold levels for household-debt increases being associated with negative macro outcomes start relatively low, at about 30% of GDP.

Clearly, America is already well past that point. As households become more indebted, the IMF says, future GDP growth and consumption decline and unemployment rises relative to their average values.

"Changes in household debt have a positive contemporaneous relationship to real GDP growth and a negative association with future real GDP growth," the report says.

Specifically, the IMF says a 5% increase in household debt to GDP over a three-year period leads to a 1.25% fall in real GDP growth three years into the future.

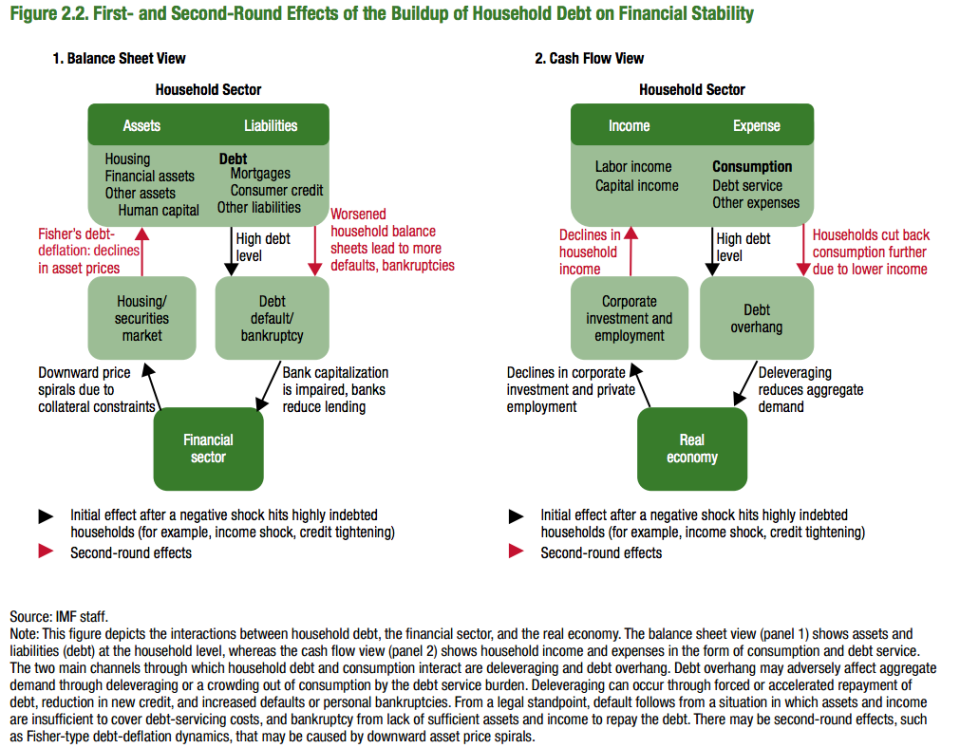

The following chart helps visualize the process by which this takes place:

International Monetary Fund"Housing busts and recessions preceded by larger run-ups in household debt tend to be more severe and protracted," the IMF said.

Is there a solution? If things reach a tipping point, yes, says the IMF — there's always debt forgiveness. Even creditors stand to benefit.

"We find that government policies can help prevent prolonged contractions in economic activity by addressing the problem of excessive household debt," the report said.

The IMF cites "bold household debt restructuring programs such as those implemented in the United States in the 1930s and in Iceland today" as historical precedents.

"Such policies can, therefore, help avert self-reinforcing cycles of household defaults, further house price declines, and additional contractions in output."

It's no coincidence that household debt soared across many countries right before the most recent global slump. The figures are rather startling: In the five years to 2007, the ratio of household debt to income rose by an average of 39 percentage points, to 138%, in advanced economies. In Denmark, Iceland, Ireland, the Netherlands, and Norway, debt peaked at more than 200% of household income, the IMF said.

In other words: We’ve seen this movie before.

NOW WATCH: RAY DALIO: You have to bet against the consensus and be right to be successful in the markets

See Also: