Ashland (ASH) Benefits From Strong End-Market Demand & Pricing

Ashland Global Holdings Inc. ASH is benefiting from strong demand across its end markets and disciplined pricing actions amid supply-chain and logistics headwinds.

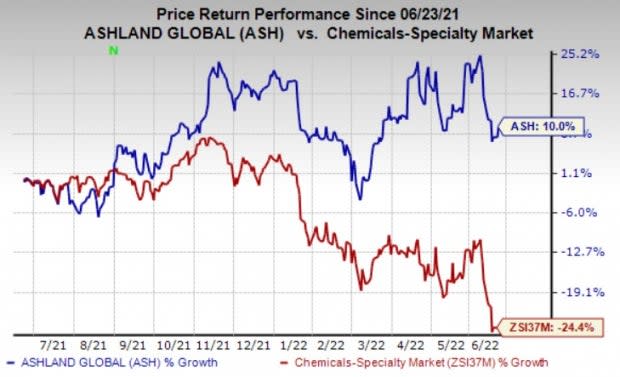

Shares of Ashland, a Zacks Rank #3 (Hold) stock, have gained 10% over the past year against the 24.4% decline of its industry.

Image Source: Zacks Investment Research

Ashland’s restructuring actions have provided it with a profitable, high-margin portfolio focused on high-quality markets and better positioned it for future growth. It is benefiting from solid demand in most consumer end markets. Its industrial businesses are witnessing strong demand recovery. Ashland is seeing higher demand across core personal-care end markets. The company, in its fiscal second quarter call, noted that it expects underlying demand to remain strong for its focused ingredients and additives product portfolio. The company is also gaining from the contributions from the Schulke & Mayr acquisition.

The company is also taking a number of actions including reduction of operating costs to boost profitability. Cost-reduction measures are expected to support its margins in fiscal 2022. The company’s pricing measures are also contributing to its top line growth. It expects its pricing and mix improvement actions to cover the current inflation.

Ashland also remains committed to boosting its cash flows and returning value to shareholders. The company remains focused on expanding margins and improving free cash flow conversion. It recently raised its quarterly cash dividend by 12% to 33.5 cents per share. The company’s board also authorized a new, evergreen $500-million common stock repurchase program. The new authorization discontinues and replaces Ashland’s 2018 $1-billion share buyback program.

However, tight raw material supply conditions are a concern. The company faces challenges from availability of raw materials. It is seeing a significant inflation in raw material and energy costs. Raw material and supply chain tightness are expected to continue in the short haul.

The company also faces headwinds from global logistics and shipping constraints. Ashland continued to witness higher freight and logistics costs in the second quarter of fiscal 2022. The supply chain and logistics challenges are expected to persist over the near term. This might result in higher costs and weigh on the company’s margins. Pandemic-related lockdowns in China and the impact of the Russia-Ukraine conflict are other concerns.

Ashland Global Holdings Inc. Price and Consensus

Ashland Global Holdings Inc. price-consensus-chart | Ashland Global Holdings Inc. Quote

Stocks to Consider

Better-ranked stocks worth considering in the basic materials space include Nutrien Ltd. NTR, Albemarle Corporation ALB and Cabot Corporation CBT.

Nutrien, sporting a Zacks Rank #1 (Strong Buy), has an expected earnings growth rate of 174.6% for the current year. The Zacks Consensus Estimate for NTR's current-year earnings has been revised 22.9% upward over the last 60 days. You can see the complete list of today’s Zacks #1 Rank stocks here.

Nutrien beat the Zacks Consensus Estimate for earnings in three of the last four quarters while missed once. It has a trailing four-quarter earnings surprise of roughly 5.8%, on average. NTR has rallied roughly 41% in a year.

Albemarle has a projected earnings growth rate of 231.7% for the current year. The Zacks Consensus Estimate for ALB’s current-year earnings has been revised 116.1% upward in the past 60 days.

Albemarle’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average being 22.5%. ALB has rallied roughly 32% in a year. The company flaunts a Zacks Rank #1.

Cabot, currently carrying a Zacks Rank #1, has an expected earnings growth rate of 22.5% for the current fiscal year. The Zacks Consensus Estimate for CBT's earnings for the current fiscal has been revised 6% upward in the past 60 days.

Cabot’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average being 16.2%. CBT has gained around 10% over a year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

To read this article on Zacks.com click here.