Australian Dollar Hoping for a Correction After Dramatic Selloff

Fundamental Forecast for Australian Dollar: Neutral

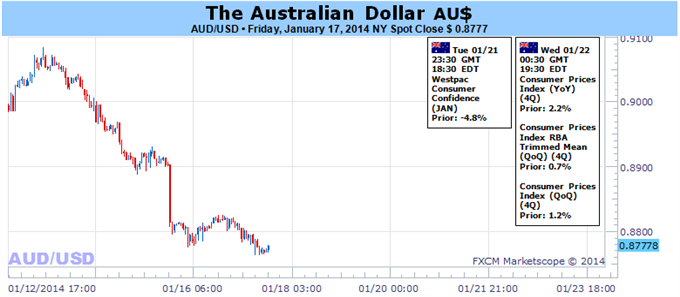

4Q Chinese GDP, Australian CPI Data Set to Guide RBA Policy Outlook

Aussie May Find a Lifeline Amid a Lull in Taper-Related US News-Flow

Help Time Key Turning Points for the Australian Dollar with DailyFX SSI

The Australian Dollar floundered last week, producing its worst five-day performance in since mid-June of last year. Home-grown and external factors aligned to undermine the currency. On the domestic front, December’s abysmal jobs report weighed heavily on RBA policy expectations, pushing a Credit Suisse index tracking investors priced-in 12-month rates outlook to the weakest since early October. Meanwhile, upbeat comments from Federal Reserve officials and a rosy Beige Book survey scattered doubts about continued “tapering” of QE asset purchases that emerged following December’s soft nonfarm payrolls print. This pushed US yields higher, punishing the yield-sensitive Australian unit.

Next week, fourth-quarter Chinese GDP and Australian CPI figures will continue to inform speculation about the RBA’s next move. The former is due to show output growth in the world’s second-largest economy and Australia’s top export market is expected to slow to year-on-year rate of 7.6 percent, down from 7.8 percent recorded in the prior quarter. That would put the average 2013 growth rate slightly higher than economists’ median forecasts (as tracked by a survey conducted by Bloomberg), so absent a significant downside surprise the result may prove to have a lasting negative impact on the Aussie.

The latter is expected to put the headline year-on-year inflation rate at 2.4 percent, reversing a drop to 2.2 percent in the third quarter to match the result recorded in the three months to June 2013. Leading indicators from the Australian Industry Group (AiG) suggest that while pricing trends in the manufacturing and services sectors remained sluggish (but broadly in line with 12-month trends), the construction industry saw a dramatic increase. Indeed, output prices expanded for the first time since 2010 in December. That seems to reinforce the likelihood of a pickup in overall inflation, which may work against RBA rate cut bets and offer support to the beleaguered Australian currency.

Turning to the US, a shortened holiday week offers little in terms of high-profile economic data. That leaves relatively little fuel to feed last week’s strongly pro-taper cues. That may open the door for a bit of a correction across the spectrum of assets sensitive to the FOMC policy outlook. Such a scenario in the context of last week’s brutal Aussie selloff may leave the door open for a correction, particularly considering the steady rebuilding of speculative net-short positioning toward record levels over recent weeks. - IS

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.

Learn forex trading with a free practice account and trading charts from FXCM.