Avoid Buyer’s Remorse by Avoiding Shopify Stocks for the Near Term

Without a doubt, e-commerce marketplace Shopify (NYSE:SHOP) has been a revelation. After a brilliant performance in 2017 and a respectable one in 2018, Shopify stock is simply on fire this year. Despite a general slowdown in momentum in the second half, shares are still up nearly 169% year-to-date. Still, with so much positivity, it’s fair to wonder if this rally is sustainable.

Source: Paul McKinnon / Shutterstock.com

Based on Shopify’s disclosure about its holiday sales, the answer is a resounding “yes.” From Black Friday to Cyber Monday, SHOP subscribers generated $2.9 billion in revenue. This represents a massive 61% jump from the year-ago results of $1.8 billion. Not surprisingly, SHOP stock jumped over 6% in the markets on the emphatically bullish disclosure.

Aside from the growth implications, Shopify stock now has more credibility. Management has set ambitious goals, planning to spend $1 billion over the next five years to bolster its businesses. Primarily, the company sets up e-commerce platforms for small businesses. It also has partnerships with larger enterprises to handle their online payments and shipping services.

InvestorPlace - Stock Market News, Stock Advice & Trading Tips

Nevertheless, it’s a tough feat to consecutively generate double- or triple-digit returns. Although SHOP stock is levered to one of the most-powerful revolutions in business (e-commerce), competition is fierce. Furthermore, a challenge for Shopify is that it’s an entrepreneurial platform.

This contrasts with an organization like Square (NYSE:SQ). Featuring applications that are relevant for both small businesses and non-entrepreneurs (e.g., its Cash App), Square’s services have broader appeal. But with Shopify, you must have the entrepreneurial bug to make use of the platform.

Moving forward, I believe this limited scope makes buying Shopify stock now a risky proposition.

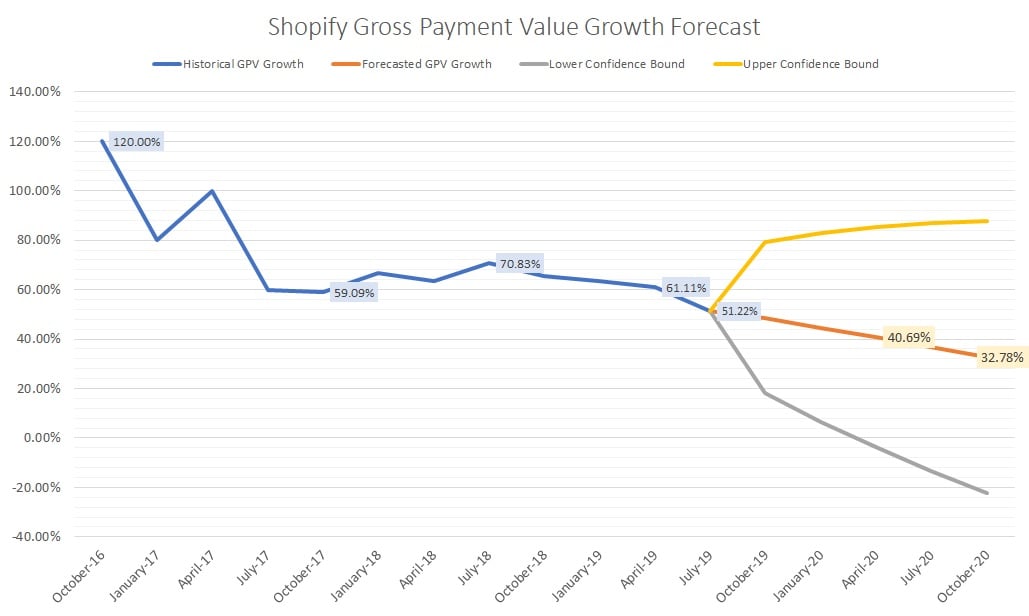

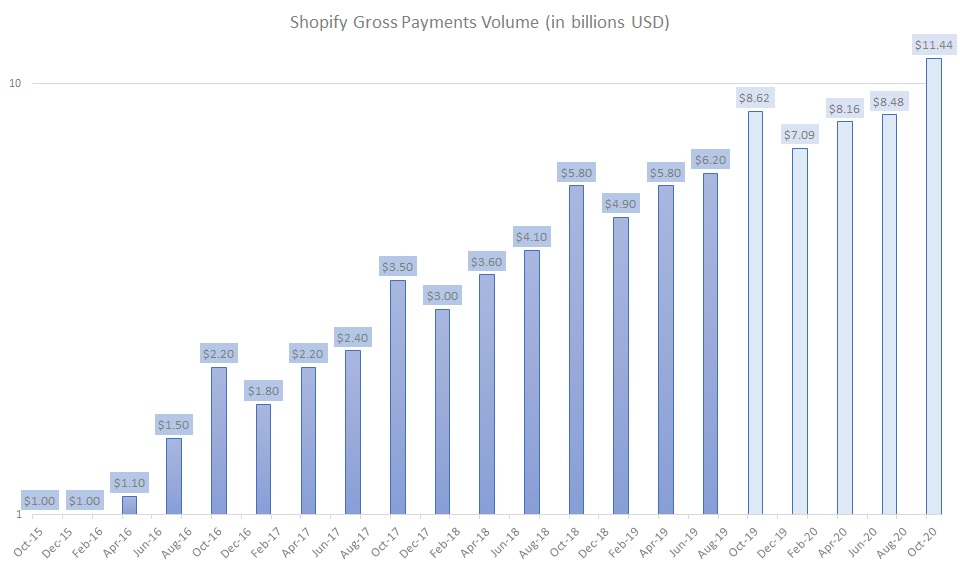

Declining Growth in Gross Payment Volume

One helpful metric to determine the popularity of an e-commerce platform is gross payment volume (GPV). This is the total spend that merchants process minus refunds. Ideally, you’d like to see strong growth in this metric as it lends credibility toward expansionary strategies.

For Shopify stock, the interval from the fourth quarter of 2016 through third quarter 2017 witnessed the most-robust year-over-year growth in GPV over a one-year period, averaging 90%. However, the rate has declined noticeably since then. For example, in the last four reported quarters, GPV growth averaged 60.3%.

Source: Chart by Josh Enomoto

Is this slowdown by itself enough to warrant panic on SHOP stock? Probably not. However, if I extrapolate the growth rate out to Q4 2020, using growth rate data from Q4 2016 onward, I calculate an average of 40.7% GPV growth over the next five quarters.

Implementing some simple math, I come out with a Q4 2020 GPV haul of $11.4 billion. While that sounds like a lot from where we stand, it’s not that impressive contextually.

Source: Chart by Josh Enomoto

For instance, Square’s GPV in Q3 2019 was $28.2 billion. And it also made money in the quarter, whereas Shopify’s net income losses are expanding. Square’s forward price-earnings ratio is 70 times, whereas SHOP stock is at a blistering 417 times.

In other words, you’re paying an extremely high premium for a platform that appears to be peaking.

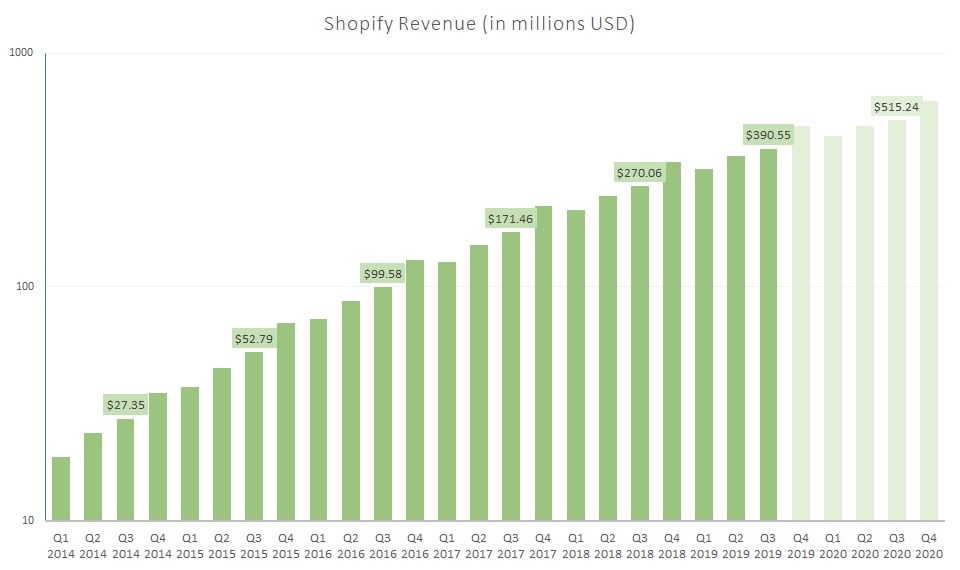

Slowing Revenue Growth a Concern for Shopify Stock

Another factor that gives me pause is top-line sales. Looking at Shopify’s numbers quarter to quarter is somewhat misleading. For example, in Q3 2019, the company rang up $390.5 million, which is nearly 45% YOY growth.

By itself, this figure is very impressive. However, since Q1 2016, the growth rate has declined for 15 straight quarters. I find this odd because, with quarterly sales of $390 million, you should still have the law of small numbers working in your favor. This is especially the case if your ultimate ambition is to challenge Amazon (NASDAQ:AMZN), which Shopify intends to do.

Source: Chart by Josh Enomoto

Using the above extrapolation method, I forecast average YoY revenue growth over the next five quarters at 35%. That ultimately translates to 2020 revenue of $2.07 billion.

If we assume that 2019 revenue hits around $1.6 billion (it’s currently tracking for $1.42 billion), this would represent around 29% annual sales growth. It’s a respectable number, but it’s a far cry from challenging Amazon.

From 2017 to 2018, Shopify revenue jumped 59%. And in the prior-year comparison, sales increased 73%. Thus, the growth rate isn’t moving in the right direction.

Takeaway on SHOP Stock

Of course, the immediate counterargument to these forecasts is that they could be well off the mark. And that’s a very fair point. However, I’m coming up with my numbers based on available data. What they show consistently is that fundamental momentum is declining. Not good news for SHOP stock investors.

Ultimately, though, I’m not here to bash Shopify stock. Rather, I’m cautioning against buying shares at their current market premium. I get the idea that the company provides a fun, intuitive platform for entrepreneurs. However, small businesses fail more often than they succeed.

From that perspective, the declining rates in GPV and revenue become even more of a cautionary tale. I like the concept of Shopify stock. I’m just not ready to pay that steep a price.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.

More From InvestorPlace

The post Avoid Buyer’s Remorse by Avoiding Shopify Stocks for the Near Term appeared first on InvestorPlace.