Better Buy: Enbridge vs. Enterprise Products Partners

Enbridge (NYSE: ENB) and Enterprise Products Partners (NYSE: EPD) are among the largest midstream players in North America. Although they hail from different countries, if you've looked at the high-yield midstream energy space, these two and their roughly 6% yields have probably popped onto your radar screen. Despite their numerous similarities, there are a few key differences that will help you decide which one is a better buy for you. Here's what you need to know.

The similarities

With a roughly $75 billion market cap, Enbridge is a bit larger than $60 billion market cap Enterprise, which is structured as a master limited partnership. However, both rank among the largest energy companies in North America, in addition to being two of the biggest in the midstream sector. They each have assets spanning across Canada and the United States. And their businesses are largely backed by regulated assets and long-term contracts.

Image source: Getty Images.

There are some differences in the assets themselves, however. For example, Enterprise's portfolio includes pipelines, storage, export facilities, processing plants, and a fleet of boats. It's more focused on oil, natural gas, and the products into which they are turned. Enbridge's portfolio includes similar energy infrastructure, but also contains a utility business. That adds a level of diversification, though it pulls the company a little outside of the midstream space. That's not necessarily good or bad in itself, but it does mean that Enbridge isn't as pure a play on midstream as Enterprise, if that's important to you.

Each company has also done an excellent job of rewarding investors over time. Enbridge has the longer streak of annual dividend hikes, with 22 years of consecutive increases under its belt, and Enterprise is close behind with 21 years of distribution hikes. However, this is where some key differences start to show up.

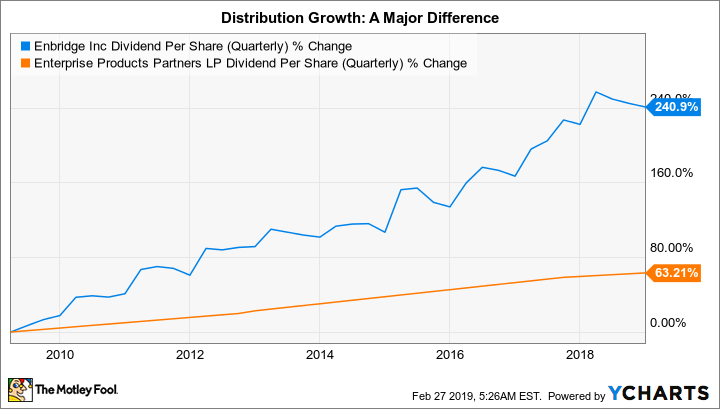

The important disparities

Over the past decade, Enbridge's dividend has grown at a compound annual rate of roughly 12%. The fact that that's around four times the historical rate of inflation growth ensures that the buying power of investor dividends grows robustly over time. Enterprise's distribution increased by a little less than 6% over the past decade, a notably slower pace. Although both midstream giants kept investors ahead of inflation, Enbridge's numbers here are clearly better.

ENB Dividend Per Share (Quarterly) data by YCharts.

That said, the future is likely to be a little different. For example, Enterprise is currently working to shift its business model so that it will self-fund more of its growth spending (which will minimize the number of dilutive units it has to sell to raise capital). That's pushing its distribution growth rate down to roughly the inflation rate for a couple of years (and also has the effect of lowering its historical averages). After this transition is done, which should happen by 2020, distribution growth is likely to tick back up to the mid single digits. Enbridge, which recently completed buying a number of controlled businesses, is looking for distribution growth of roughly 10% a year through 2020, after which it believes dividend will grow around 5% to 7% a year. It expects to self-fund much of that growth.

Neither of these projections includes major acquisitions, which could result in a large one-time distribution boost. But the basic idea is that Enbridge will be a far more rewarding dividend-growth investment for a couple of years and then be roughly on par with Enterprise. That would give it the edge if all other things were equal -- but they aren't.

ENB Financial Debt to EBITDA (TTM) data by YCharts.

Enbridge's debt-to-EBITDA ratio is roughly 6.7, more than twice Enterprise's ratio of 3. Enbridge has historically made greater use of leverage than Enterprise, which increases financial risk. The higher distribution growth rate has, basically, come with a cost. So far Enbridge has managed that risk well, but for conservative investors, Enterprise and its lower leverage might start looking a little more enticing at this point.

What to do?

In the end, both Enterprise and Enbridge are large and well-run midstream players. They each have robust yields that are supported by long histories of distribution growth. Enbridge will likely provide more dividend growth for a couple of years before settling down into the mid single digits, but it has more leverage. Enterprise's distribution will be a little less rewarding for a couple of years as it makes a conservative change to its business model. And then distribution growth should get back to its historical mid-single-digit range. That said, the company has a history of being very conservative with its finances, which some will see as a big plus.

If you prefer a more conservative approach to investing, you should probably err on the side of caution and go with Enterprise. However, if you don't mind paying a little more attention to your investments, and can get comfortable with the company's more aggressive use of leverage, then Enbridge is likely to be the better option. Neither, however, is likely to be a bad choice.

More From The Motley Fool

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool recommends Enbridge and Enterprise Products Partners. The Motley Fool has a disclosure policy.