Will Brady Corporation (NYSE:BRC) Continue To Underperform Its Industry?

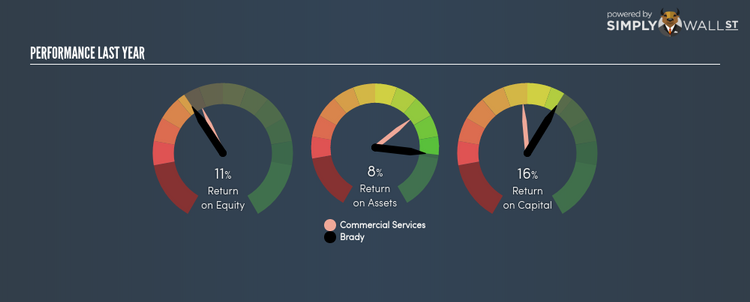

Brady Corporation (NYSE:BRC) delivered a less impressive 10.64% ROE over the past year, compared to the 12.04% return generated by its industry. BRC’s results could indicate a relatively inefficient operation to its peers, and while this may be the case, it is important to understand what ROE is made up of and how it should be interpreted. Knowing these components could change your view on BRC’s performance. I will take you through how metrics such as financial leverage impact ROE which may affect the overall sustainability of BRC’s returns. See our latest analysis for Brady

What you must know about ROE

Return on Equity (ROE) is a measure of Brady’s profit relative to its shareholders’ equity. An ROE of 10.64% implies $0.11 returned on every $1 invested. While a higher ROE is preferred in most cases, there are several other factors we should consider before drawing any conclusions.

Return on Equity = Net Profit ÷ Shareholders Equity

ROE is assessed against cost of equity, which is measured using the Capital Asset Pricing Model (CAPM) – but let’s not dive into the details of that today. For now, let’s just look at the cost of equity number for Brady, which is 4.65%. While Brady’s peers may have higher ROE, it may also incur higher cost of equity. An undesirable and unsustainable practice would be if returns exceeded cost. However, this is not the case for Brady which is encouraging. ROE can be broken down into three different ratios: net profit margin, asset turnover, and financial leverage. This is called the Dupont Formula:

Dupont Formula

ROE = profit margin × asset turnover × financial leverage

ROE = (annual net profit ÷ sales) × (sales ÷ assets) × (assets ÷ shareholders’ equity)

ROE = annual net profit ÷ shareholders’ equity

Basically, profit margin measures how much of revenue trickles down into earnings which illustrates how efficient the business is with its cost management. Asset turnover reveals how much revenue can be generated from Brady’s asset base. The most interesting ratio, and reflective of sustainability of its ROE, is financial leverage. Since ROE can be artificially increased through excessive borrowing, we should check Brady’s historic debt-to-equity ratio. The debt-to-equity ratio currently stands at a low 9.73%, meaning Brady still has headroom to borrow debt to increase profits.

Next Steps:

ROE is one of many ratios which meaningfully dissects financial statements, which illustrates the quality of a company. Even though Brady returned below the industry average, its ROE comes in excess of its cost of equity. Also, ROE is not likely to be inflated by excessive debt funding, giving shareholders more conviction in the sustainability of returns, which has headroom to increase further. Although ROE can be a useful metric, it is only a small part of diligent research.

For Brady, there are three fundamental factors you should further research:

Financial Health: Does it have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

Valuation: What is Brady worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether Brady is currently mispriced by the market.

Other High-Growth Alternatives : Are there other high-growth stocks you could be holding instead of Brady? Explore our interactive list of stocks with large growth potential to get an idea of what else is out there you may be missing!

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.