Is Brambles Limited’s (ASX:BXB) 15.34% ROE Good Enough Compared To Its Industry?

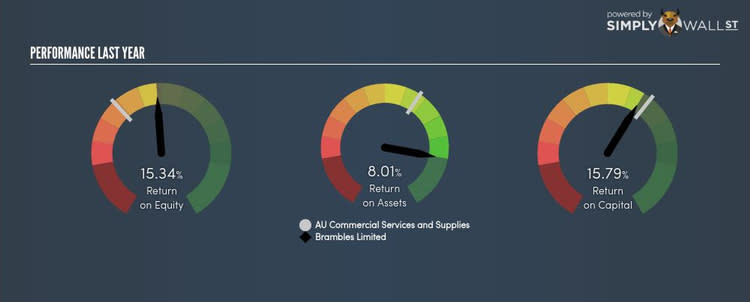

Brambles Limited (ASX:BXB) delivered an ROE of 15.34% over the past 12 months, which is an impressive feat relative to its industry average of 9.12% during the same period. On the surface, this looks fantastic since we know that BXB has made large profits from little equity capital; however, ROE doesn’t tell us if management have borrowed heavily to make this happen. We’ll take a closer look today at factors like financial leverage to determine whether BXB’s ROE is actually sustainable. See our latest analysis for BXB

Breaking down ROE — the mother of all ratios

Return on Equity (ROE) weighs BXB’s profit against the level of its shareholders’ equity. For example, if BXB invests $1 in the form of equity, it will generate $0.15 in earnings from this. Generally speaking, a higher ROE is preferred; however, there are other factors we must also consider before making any conclusions.

Return on Equity = Net Profit ÷ Shareholders Equity

ROE is measured against cost of equity in order to determine the efficiency of BXB’s equity capital deployed. Its cost of equity is 8.55%. Since BXB’s return covers its cost in excess of 6.78%, its use of equity capital is efficient and likely to be sustainable. Simply put, BXB pays less for its capital than what it generates in return. ROE can be dissected into three distinct ratios: net profit margin, asset turnover, and financial leverage. This is called the Dupont Formula:

Dupont Formula

ROE = profit margin × asset turnover × financial leverage

ROE = (annual net profit ÷ sales) × (sales ÷ assets) × (assets ÷ shareholders’ equity)

ROE = annual net profit ÷ shareholders’ equity

Basically, profit margin measures how much of revenue trickles down into earnings which illustrates how efficient BXB is with its cost management. Asset turnover shows how much revenue BXB can generate with its current asset base. And finally, financial leverage is simply how much of assets are funded by equity, which exhibits how sustainable BXB’s capital structure is. Since financial leverage can artificially inflate ROE, we need to look at how much debt BXB currently has. At 95.98%, BXB’s debt-to-equity ratio appears balanced and indicates the above-average ROE is generated from its capacity to increase profit without a large debt burden.

What this means for you:

Are you a shareholder? BXB’s above-industry ROE is encouraging, and is also in excess of its cost of equity. Since its high ROE is not likely driven by high debt, it might be a good time to top up on your current holdings if your fundamental research reaffirms this analysis.

Are you a potential investor? If BXB has been on your watch list for a while, making an investment decision based on ROE alone is unwise. I recommend you do additional fundamental analysis by looking through our most recent infographic report on Brambles to help you make a more informed investment decision. If you are not interested in BXB anymore, you can use our free platform to see our list of stocks with Return on Equity over 20%.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.