Campbell (CPB) Surpasses Earnings & Sales Estimates in Q4

Campbell Soup Company CPB has reported solid results for fourth-quarter fiscal 2021, wherein the top and bottom lines beat the Zacks Consensus Estimate. However, both metrics declined year over year. Results gained from strength across the majority of its core categories. The company noted that fiscal 2021 ended on a strong note. It expects fiscal 2022 to gain from positive momentum in its brands and efforts to mitigate inflation.

Quarterly Highlights

Adjusted earnings from continuing operations tumbled 13% year over year to 55 cents per share but surpassed the Zacks Consensus Estimate of 47 cents. The downside was a result of reduced adjusted EBIT. However, the metric advanced 31% from 42 cents reported in fourth-quarter fiscal 2019.

Net sales of $1,873 million decreased 11% year over year but surpassed the Zacks Consensus Estimate of $1,821 million. However, sales rose 5% from fourth-quarter fiscal 2019. Organic sales declined 4% year over year due to lower volumes and mix stemming from sturdy demand in food and continued at-home consumption. The metric grew 9% from fourth-quarter fiscal 2019.

The company’s adjusted gross margin contracted 420 basis points to 31.4%. The downside was caused by cost inflation and other supply-chain expenses, which somewhat offset supply-chain productivity improvements and cost-saving initiatives.

Adjusted EBIT plunged 13% to reach $267 million mainly on account of lower sales volumes and reduced adjusted gross margin, somewhat made up by a decline in marketing and selling costs as well as lower adjusted administrative expenses. Nonetheless, the metric rose 6% from $252 million reported in fourth-quarter fiscal 2019.

Campbell Soup Company Price, Consensus and EPS Surpris

Campbell Soup Company price-consensus-eps-surprise-chart | Campbell Soup Company Quote

Segment Analysis

Meals & Beverages: Net sales declined 16% year over year to $851 million, with organic sales declining 9%. The downside mainly resulted from declines in all U.S. retail products (including U.S. soup, Prego pasta sauces and Pace Mexican sauces). However, organic net sales increased 10% on a two-year basis.

Volumes in U.S. retail were hurt due to partial retailer inventory recovery and positive demand in food from continued at-home consumption. U.S. soup sales fell 21% due to weakness in condensed soups, broth and ready-to-serve soups. Operating earnings in the unit tanked 30%.

Snacks: Net sales in the division were down 6% to $1,022 million. The segment was hurt by weakness in salty snacks like Pop Secret popcorn, Cape Cod potato chips and Snyder's of Hanover pretzels along with softness in Lance sandwich crackers, partner brands and fresh bakery.

Organic sales in the segment rose 1%, driven by higher volumes in Goldfish crackers and the salty snacks portfolio, including Snack Factory Pretzel Crisps, Snyder's of Hanover pretzels and Cape Cod potato chips, which partly offset the sluggishness in partner brands and fresh bakery. The metric also grew 7% on a two-year basis. Segmental operating earnings rose 7%.

Other Financial Details

As of Aug 1, 2021, Campbell’s total cash and cash equivalents stood at $69 million, long-term debt was $5,010 million, and total equity amounted to $3,154 million. The company generated $1.04 billion as cash flow from operations in fiscal 2021. Capital investments amounted to $275 million in the same period.

In the fiscal fourth quarter, management paid out dividends worth $439 million and approved a $500-million share repurchase program. This is in addition to the $250-million anti-dilutive share repurchase program announced in the fiscal third quarter.

In the fiscal fourth quarter, Campbell generated savings worth $25 million as part of its multi-year, cost-saving program, which included synergies associated with the Snyder’s-Lance buyout. With this, the company generated total program-to-date savings of nearly $805 million. Management continues to anticipate annualized savings of $850 million by fiscal 2022-end.

Fiscal 2022 Guidance

Based on its fourth-quarter results and impacts of the divestiture of the Plum baby food and snacks business (on May 3), management issued the guidance for fiscal 2022. The view also considers solid demand, rising inflation and tightening of the labor market, which were somewhat offset by continued in-market momentum as well as pricing and productivity efforts.

For fiscal 2021, the company expects net sales of flat to down 2%, with organic sales likely to be between down 1% and up 1%. The sale of Plum baby food and snacks business is expected to affect fiscal 2022 sales by 1 percentage point. Adjusted EBIT is forecast to be down 8-5% but EBIT margin is predicted to improve in the second half of fiscal 2022. Adjusted EPS is envisioned to be $2.75-$2.85 for fiscal 2022.

However, management envisions first-quarter fiscal 2022 to remain drab. Margins in the first half of fiscal 2022 are estimated to be affected by transitional headwinds but the metric is likely to witness a sequential improvement in the second half of fiscal 2022. Cost inflation is anticipated to be more pronounced in the second half of fiscal 2022. Having said that, positive net price realization, supply-chain productivity improvements, and cost-saving initiatives are likely to aid the fiscal 2022 performance.

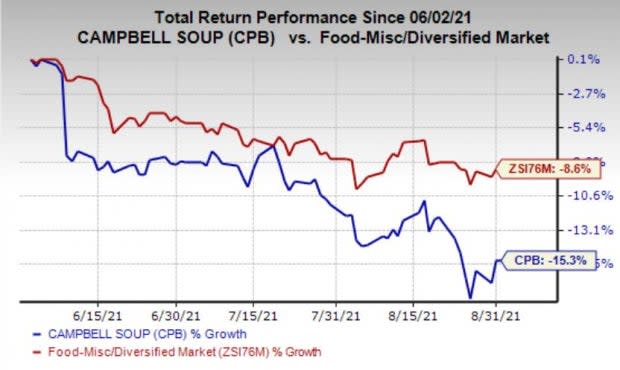

Shares of this Zacks Rank #3 (Hold) company have lost 15.3% in the past three months compared with the industry’s decline of 8.6%.

Image Source: Zacks Investment Research

Better-Ranked Stocks to Consider

Pilgrims Pride Corporation PPC currently has an expected long-term earnings growth rate of 31% and a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Chewy CHWY currently has a long-term earnings growth rate of 20% and a Zacks Rank #2 (Buy).

Hormel Foods Corporation HRL, also a Zacks Rank #2 stock, has an expected long-term earnings growth rate of 7.4%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Campbell Soup Company (CPB) : Free Stock Analysis Report

Hormel Foods Corporation (HRL) : Free Stock Analysis Report

Pilgrims Pride Corporation (PPC) : Free Stock Analysis Report

Chewy Inc. (CHWY) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research