Canopy Growth or Curaleaf: How To Choose The Better Cannabis Stock?

The pandemic has negatively impacted several industries but the cannabis or marijuana industry is certainly not one of them. In fact, cannabis sales increased since the pandemic in several markets in North America. In Illinois alone, cannabis sales touched a record $47.6 million in June, up from $44.3 million in May. As per Statistics Canada, cannabis retail sales in the country rose 7.9% month-over-month in June to C$201 million.

Anxiety due to the COVID-19 outbreak, stay-at-home orders, and greater availability of products are being cited as some of the reasons for the increased sales.

Cannabis is legal in Canada both for recreational and medical purposes. In the US, more states are expected to legalize cannabis soon. And, there are hopes of cannabis being legalized at the federal level too.

Against this backdrop, we will use TipRanks’ Stock Comparison tool, to see whether Canopy Growth or Curaleaf is a better cannabis bet.

Canopy Growth (CGC)

Canada-based Canopy Growth is one of the largest cannabis producers. Mounting losses caused the ouster of the company’s co-founder Bruce Linton as the co-CEO in June 2019. Mark Zekulin served as CEO of the company till he was replaced by alcoholic beverage giant Constellation Brands’ finance head David Klein.

Canopy Growth continued to post losses in the first quarter of fiscal 2021, which ended on June 30. However, investors were pleased to see a lower-than-anticipated loss. The fiscal first-quarter net loss reduced 34% Y/Y to C$128.3 million. The company's adjusted EBITDA loss came in at C$92 million.

Higher revenue, more than 18% reduction in headcount and lower expenses helped in trimming the losses. Canopy Growth has also scaled back or shut down facilities in many countries as part of its restructuring efforts.

Canopy Growth’s first-quarter revenue grew 22% Y/Y to C$110.4 million. However, the sequential growth was only 2%. The Y/Y growth in the company’s revenue was due to higher medical cannabis sales in Canada and Germany, increased sales of Storz & Bickel vaporizer, and the contribution from C3 and This Works, which were acquired last year.

However, the company’s Canadian recreational revenue declined 11% Y/Y due to the impact of intense competition for dried flower-based products and retail store closures due to the pandemic.

Following the results, Canaccord Genuity analyst Matt Bottomley raised his price target to C$22 from C$21 and reaffirmed his Hold rating.

Explaining the reason for a higher price target, the analyst said, “On the back of better than anticipated quarter on the top line as the company reduced its free-cash burn by >40% from only a quarter ago, we have updated our model to account for a slightly faster path to break-even (profitability).”

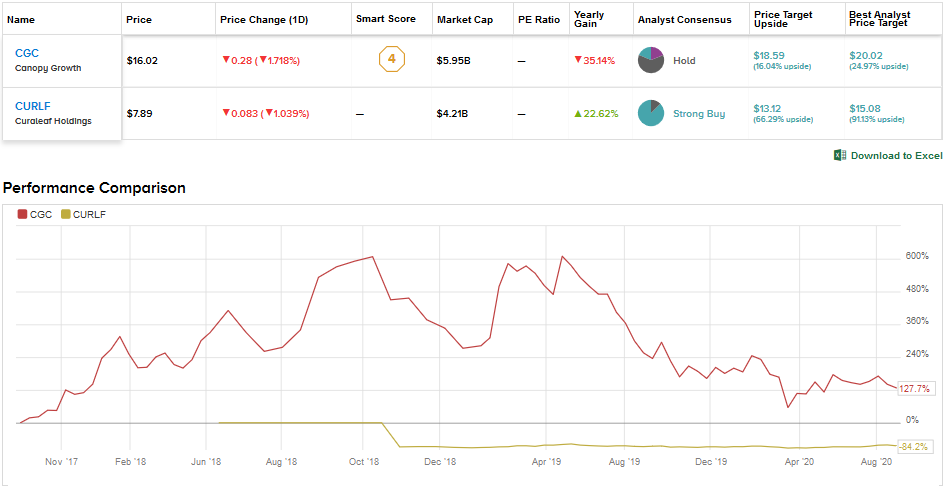

Canopy Growth has a Hold consensus rating based on 3 Buys, 10 Holds and 3 Sells. CGC stock (on NYSE) has declined 24% year-to-date. But there could be a possible upside of 16% based on an average price target of $18.69.

One of Canopy Growth’s strength is that it is backed by Constellation Brands (STZ). In May, Constellation Brands increased its stake in Canopy Growth to 38.6% by exercising its warrants. The move reinforced the company’s belief in Canopy Growth’s ability to capture growth in the emerging cannabis space.

Meanwhile, Canopy aims to boost its US sales through the launch of shopcanopy.com for CBD (cannabidiol) products, expanded distribution of Storz & Bickel vaporizer and BioSteel Sports Nutrition’s products, and a key partnership with Martha Stewart for health and wellness CBD products.

The company also aims to capture further market share in Canada for derivatives products like vapes, edibles, concentrates, and beverages. Canada legalized derivative products in October 2019 as part of the next wave of legalization, often called "Cannabis 2.0". (See CGC stock analysis on TipRanks)

Curaleaf Holdings (CURLF)

Vertically integrated multi-state operator Curaleaf is considered as one of the leading companies in the US cannabis space. The company’s second-quarter revenue surged 142% Y/Y and 22% sequentially to $117.5 million due to an array of favorable factors, including the impact of the Select acquisition, organic growth, and new stores in Florida, Massachusetts and New York.

Curaleaf’s gross margin on cannabis sales expanded by an impressive 300 basis point Y/Y to 43%. The company delivered adjusted EBITDA of $28 million, up from $4.4 million in the second quarter of 2019. However, second-quarter net loss came in at $2.0 million.

Curaleaf is expanding its business through strategic acquisitions including three Arrow Alternative Care dispensaries in Connecticut and Colorado-based premium cannabis edibles producer BlueKudu. The BlueKudu acquisition helped the company launch its Select product line in Colorado. With 4 roll-outs in new states, Select brand is now available in 12 states.

Moreover, Curaleaf’s recent acquisition of Grassroots made it the world’s largest cannabis company based on revenue and expanded its footprint from 18 to 23 states, including key growth markets like Illinois and Pennsylvania. (See CURLF stock analysis on TipRanks)

Needham analyst Matt McGinley reaffirmed his Buy rating for Curaleaf after its results. He stated, “While the pro forma 3Q revenue guide of $205-215mn is a substantial step up from comparable $165.4mn in 2Q, this could be seen as light, in our view, and margins don’t seem poised for breakout.”

However, he raised his price target to $13.50 from $11 and added, “That said, everything is very much coming together operationally for Curaleaf, and we see the prospects for growth in 2H and ’21 as exceptionally strong.”

The Street has a Strong Buy consensus for Curaleaf stock based on 7 Buys and 1 Hold. The stock had already surged 25% year-to-date as of August 23 and an average price target of $13.12 indicates a further upside potential of 66.3%.

Conclusion

Canopy Growth is struggling to be profitable and is in the midst of restructuring efforts. Meanwhile, Curaleaf delivered impressive growth in its recently reported quarterly metrics. Based on the Street’s bullish stance, strong upside potential and a vertically-integrated business model, Curaleaf definitely looks to be a better cannabis choice.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment