Is Carbine Tungsten Limited (ASX:CNQ) Cheap And High Growth?

Carbine Tungsten Limited (ASX:CNQ), a AUDA$6.76M small-cap, is a metals and mining operating in an industry which supplies materials for construction. This means it is highly sensitive to changes in the economic cycle, a key driver of building activities. Basic material analysts are forecasting for the entire industry, a strong double-digit growth of 26.78% in the upcoming year , and a whopping growth of 36.14% over the next couple of years. This rate is larger than the growth rate of the Australian stock market as a whole. Below, I will examine the sector growth prospects, and also determine whether CNQ is a laggard or leader relative to its basic materials sector peers. Check out our latest analysis for Carbine Tungsten

What’s the catalyst for CNQ’s sector growth?

Altogether the basic materials sector seems like it has reached maturity in its life cycle. Companies appear to be vastly competitive and consolidation seems to be a inevitable. There are plenty of emerging trends to deal with across the board including the reduction of waste, raw material inflation, and innovation in global supply chain management. In the past year, the industry delivered growth of 6.76%, though still underperforming the wider Australian stock market. CNQ lags the pack with its sustained negative earnings over the past couple of years. The company’s outlook seems uncertain, with a lack of analyst coverage, which doesn’t boost our confidence in the stock. This lack of growth and transparency means CNQ may be trading cheaper than its peers.

Is CNQ and the sector relatively cheap?

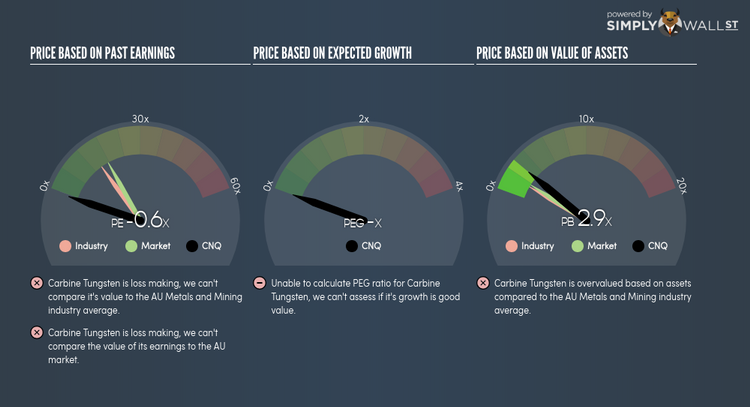

The metals and mining sector’s PE is currently hovering around 15x, relatively similar to the rest of the Australian stock market PE of 18x. This means the industry, on average, is fairly valued compared to the wider market – minimal expected gains and losses from mispricing here. Furthermore, the industry returned a similar 10.53% on equities compared to the market’s 11.91%. Since CNQ’s earnings doesn’t seem to reflect its true value, its PE ratio isn’t very useful. A loose alternative to gauge CNQ’s value is to assume the stock should be relatively in-line with its industry.

What this means for you:

Are you a shareholder? CNQ has been a metals and mining industry laggard in the past year. If your initial investment thesis is around the growth prospects of CNQ, there are other metals and mining companies that have delivered higher growth, and perhaps trading at a discount to the industry average. Consider how CNQ fits into your wider portfolio and the opportunity cost of holding onto the stock.

Are you a potential investor? If CNQ has been on your watchlist for a while, now may be a good time to dig deeper into the stock. Although its growth has delivered lower growth relative to its metals and mining peers in the near term, the market may be pessimistic on the stock, leading to a potential undervaluation. Before you make a decision on the stock, I suggest you look at CNQ’s future cash flows in order to assess whether the stock is trading at a reasonable price.

For a deeper dive into Carbine Tungsten’s stock, take a look at the company’s latest free analysis report to find out more on its financial health and other fundamentals. Interested in other basic materials stocks instead? Use our free playform to see my list of over 2000 other basic materials companies trading on the market.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.