Is Carrizo Oil & Gas, Inc. (NASDAQ:CRZO) A Financially Sound Company?

Carrizo Oil & Gas, Inc. (NASDAQ:CRZO) is a small-cap stock with a market capitalization of US$1.1b. While investors primarily focus on the growth potential and competitive landscape of the small-cap companies, they end up ignoring a key aspect, which could be the biggest threat to its existence: its financial health. Why is it important? Companies operating in the Oil and Gas industry, even ones that are profitable, are inclined towards being higher risk. Evaluating financial health as part of your investment thesis is vital. I believe these basic checks tell most of the story you need to know. Though, since I only look at basic financial figures, I’d encourage you to dig deeper yourself into CRZO here.

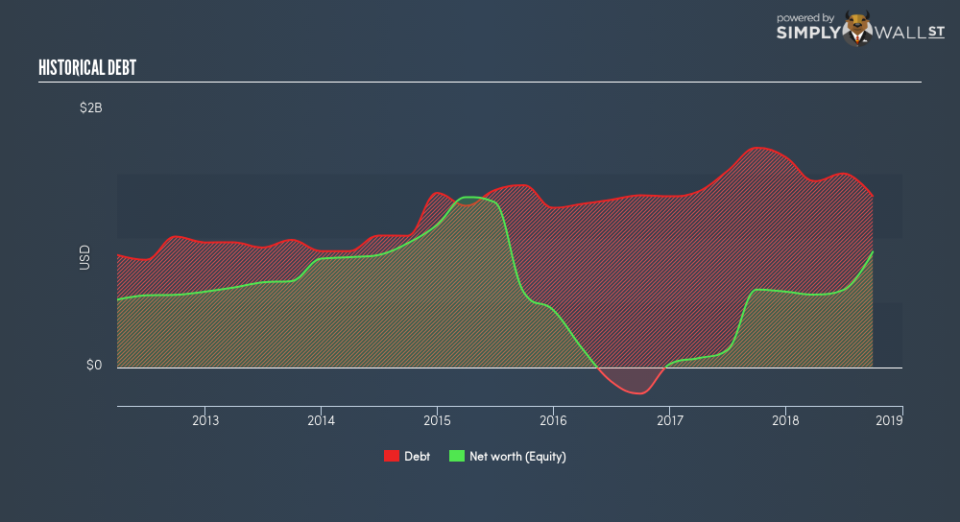

How does CRZO’s operating cash flow stack up against its debt?

CRZO has shrunken its total debt levels in the last twelve months, from US$1.7b to US$1.3b – this includes long-term debt. With this debt payback, CRZO currently has US$2.4m remaining in cash and short-term investments for investing into the business. On top of this, CRZO has generated US$608m in operating cash flow over the same time period, leading to an operating cash to total debt ratio of 46%, meaning that CRZO’s current level of operating cash is high enough to cover debt. This ratio can also be a sign of operational efficiency as an alternative to return on assets. In CRZO’s case, it is able to generate 0.46x cash from its debt capital.

Can CRZO pay its short-term liabilities?

With current liabilities at US$556m, the company may not be able to easily meet these obligations given the level of current assets of US$151m, with a current ratio of 0.27x.

Does CRZO face the risk of succumbing to its debt-load?

CRZO is a highly-leveraged company with debt exceeding equity by over 100%. This is not uncommon for a small-cap company given that debt tends to be lower-cost and at times, more accessible. We can check to see whether CRZO is able to meet its debt obligations by looking at the net interest coverage ratio. A company generating earnings before interest and tax (EBIT) at least three times its net interest payments is considered financially sound. In CRZO’s, case, the ratio of 3.28x suggests that interest is appropriately covered, which means that lenders may be inclined to lend more money to the company, as it is seen as safe in terms of payback.

Next Steps:

Although CRZO’s debt level is towards the higher end of the spectrum, its cash flow coverage seems adequate to meet debt obligations which means its debt is being efficiently utilised. However, its lack of liquidity raises questions over current asset management practices for the small-cap. Keep in mind I haven’t considered other factors such as how CRZO has been performing in the past. I recommend you continue to research Carrizo Oil & Gas to get a better picture of the stock by looking at:

Future Outlook: What are well-informed industry analysts predicting for CRZO’s future growth? Take a look at our free research report of analyst consensus for CRZO’s outlook.

Valuation: What is CRZO worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether CRZO is currently mispriced by the market.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.