Casey's General Stores (NASDAQ:CASY) Takes On Some Risk With Its Use Of Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Casey's General Stores, Inc. (NASDAQ:CASY) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Casey's General Stores

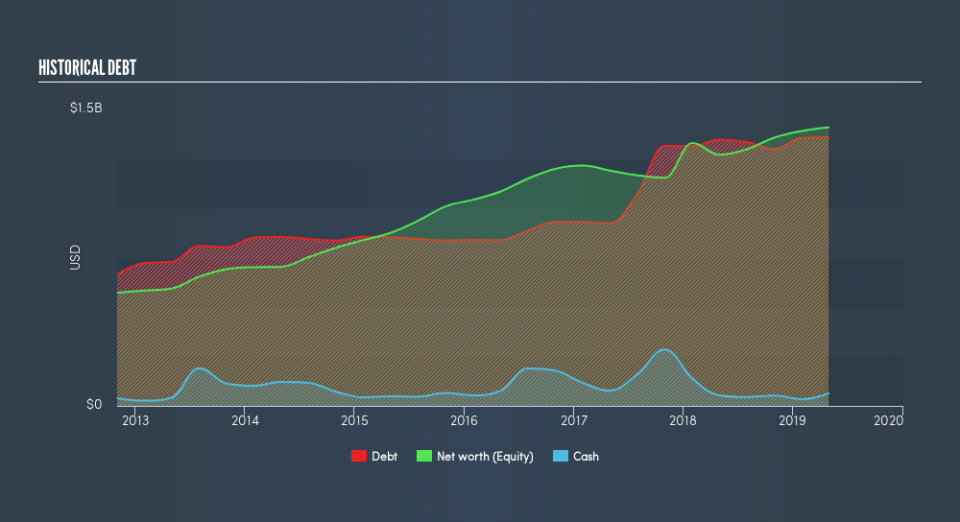

How Much Debt Does Casey's General Stores Carry?

As you can see below, Casey's General Stores had US$1.36b of debt, at April 2019, which is about the same the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$63.3m, its net debt is less, at about US$1.30b.

A Look At Casey's General Stores's Liabilities

The latest balance sheet data shows that Casey's General Stores had liabilities of US$590.9m due within a year, and liabilities of US$1.73b falling due after that. Offsetting these obligations, it had cash of US$63.3m as well as receivables valued at US$66.8m due within 12 months. So its liabilities total US$2.19b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Casey's General Stores has a market capitalization of US$6.13b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Casey's General Stores's net debt is sitting at a very reasonable 2.3 times its EBITDA, while its EBIT covered its interest expense just 5.8 times last year. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. Also relevant is that Casey's General Stores has grown its EBIT by a very respectable 20% in the last year, thus enhancing its ability to pay down debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Casey's General Stores's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Casey's General Stores barely recorded positive free cash flow, in total. While many companies do operate at break-even, we prefer see substantial free cash flow, especially if a it already has dead.

Our View

Casey's General Stores's conversion of EBIT to free cash flow was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. For example its EBIT growth rate was refreshing. Looking at all the angles mentioned above, it does seem to us that Casey's General Stores is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. In light of our reservations about the company's balance sheet, it seems sensible to check if insiders have been selling shares recently.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.