Has Check Point Software Technologies Ltd’s (NASDAQ:CHKP) Earnings Momentum Changed Recently?

When Check Point Software Technologies Ltd’s (NASDAQ:CHKP) announced its latest earnings (30 June 2018), I wanted to understand how these figures stacked up against its past performance. The two benchmarks I used were Check Point Software Technologies’s average earnings over the past couple of years, and its industry performance. These are useful yardsticks to help me gauge whether or not CHKP actually performed well. Below is a quick commentary on how I see CHKP has performed.

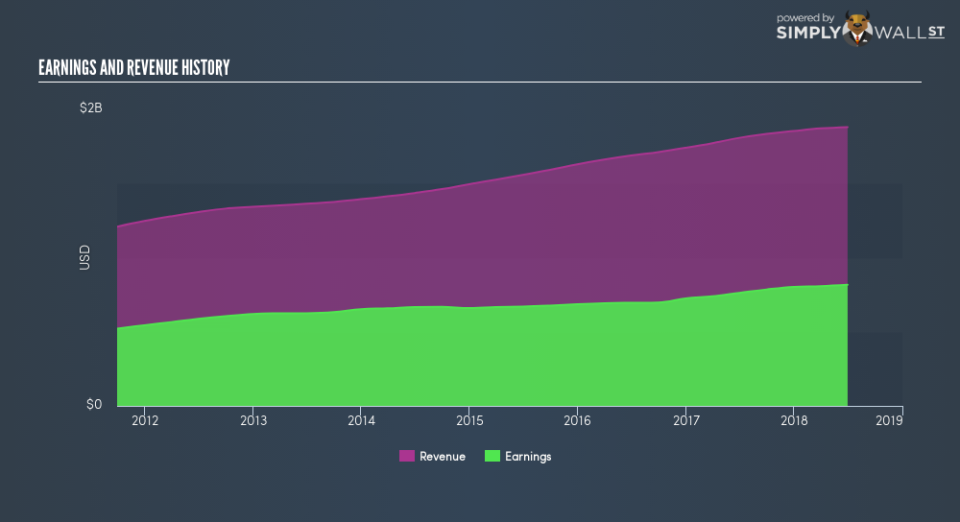

Check out our latest analysis for Check Point Software Technologies

How CHKP fared against its long-term earnings performance and its industry

CHKP’s trailing twelve-month earnings (from 30 June 2018) of US$816.8m has increased by 7.1% compared to the previous year. Furthermore, this one-year growth rate has exceeded its 5-year annual growth average of 5.4%, indicating the rate at which CHKP is growing has accelerated. How has it been able to do this? Let’s take a look at if it is merely due to industry tailwinds, or if Check Point Software Technologies has experienced some company-specific growth.

The climb in earnings seems to be driven by a solid top-line increase outstripping its growth rate of expenses. Though this resulted in a margin contraction, it has made Check Point Software Technologies more profitable. Looking at growth from a sector-level, the US software industry has been growing its average earnings by double-digit 11.2% in the prior year, and 12.1% over the past half a decade. This growth is a median of profitable companies of 25 Software companies in US including NetSol Technologies, LINE and LINE. This shows that any tailwind the industry is benefiting from, Check Point Software Technologies has not been able to leverage it as much as its average peer.

In terms of returns from investment, Check Point Software Technologies has invested its equity funds well leading to a 22.5% return on equity (ROE), above the sensible minimum of 20%. Furthermore, its return on assets (ROA) of 13.4% exceeds the US Software industry of 7.5%, indicating Check Point Software Technologies has used its assets more efficiently. And finally, its return on capital (ROC), which also accounts for Check Point Software Technologies’s debt level, has increased over the past 3 years from 22.3% to 23.4%.

What does this mean?

Check Point Software Technologies’s track record can be a valuable insight into its earnings performance, but it certainly doesn’t tell the whole story. While Check Point Software Technologies has a good historical track record with positive growth and profitability, there’s no certainty that this will extrapolate into the future. I suggest you continue to research Check Point Software Technologies to get a better picture of the stock by looking at:

Future Outlook: What are well-informed industry analysts predicting for CHKP’s future growth? Take a look at our free research report of analyst consensus for CHKP’s outlook.

Financial Health: Are CHKP’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 30 June 2018. This may not be consistent with full year annual report figures.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.