Is China Resources Beer (Holdings) Company Limited (SEHK:291) A Financially Sound Company?

Mid-caps stocks, like China Resources Beer (Holdings) Company Limited (SEHK:291) with a market capitalization of HK$73.96B, aren’t the focus of most investors who prefer to direct their investments towards either large-cap or small-cap stocks. Surprisingly though, when accounted for risk, mid-caps have delivered better returns compared to the two other categories of stocks. Mid-caps are found to be more volatile than the large-caps but safer than small-caps, largely due to their weaker balance sheet. I will take you through a few basic checks to assess the financial health of companies with no debt. See our latest analysis for 291

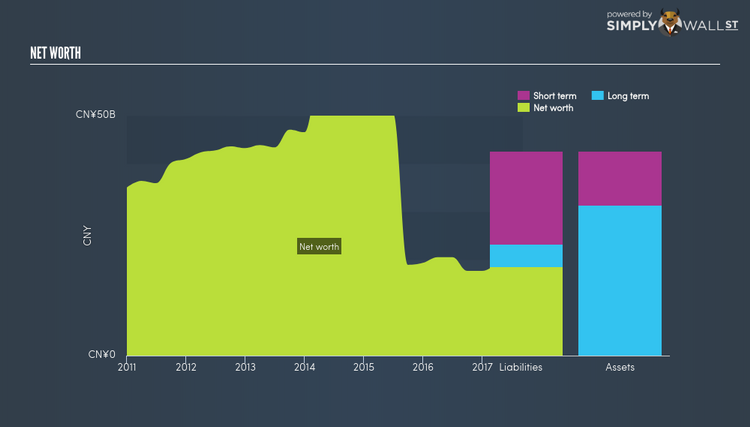

Does 291 face the risk of succumbing to its debt-load?

While ideally the debt-to equity ratio of a financially healthy company should be less than 40%, several factors such as industry life-cycle and economic conditions can result in a company raising a significant amount of debt. In the case of 291, the debt-to-equity ratio is 19.04%, which means its debt level does not pose a threat to its operations right now. We can test if 291’s debt levels are sustainable by measuring interest payments against earnings of a company. Ideally, earnings (EBIT) should cover interest by at least three times, therefore reducing concerns when profit is highly volatile. 291’s interest on debt is sufficiently covered by earnings as it sits at around 35.95x. Debtors may be willing to loan the company more money, giving 291 ample headroom to grow its debt facilities.

Can 291 meet its short-term obligations with the cash in hand?

Debt to equity ratio is an important aspect of financial strength. But if the company has a substantial amount of cash on its balance sheet, that should allay some fear of a debt overhang and increase the chance of meeting upcoming liabilities. We need to assess 291’s cash and other liquid assets against its upcoming expenses. Our analysis shows that 291 is unable to meet all of its upcoming commitments with its cash and other short-term assets. While this is not abnormal for companies, as their cash is better invested in the business or returned to investors than lying around, it does bring about some concerns should any unfavourable circumstances arise.

Next Steps:

Are you a shareholder? 291’s high cash coverage and low levels of debt indicate its ability to use its borrowings efficiently in order to produce a healthy cash flow. Since 291’s capital structure could change, You should continue examining market expectations for 291’s future growth on our free analysis platform.

Are you a potential investor? While investors should analyse the serviceability of debt, it shouldn’t be viewed in isolation of other factors. Ultimately, debt financing is an important source of funding for companies seeking to grow through new projects and investments. 291’s Return on Capital Employed (ROCE) in order to see management’s track record at deploying funds in high-returning projects.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.