The Consensus EPS Estimates For Select Energy Services, Inc. (NYSE:WTTR) Just Fell Dramatically

Today is shaping up negative for Select Energy Services, Inc. (NYSE:WTTR) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon. Investors however, have been notably more optimistic about Select Energy Services recently, with the stock price up a remarkable 23% to US$5.26 in the past week. It will be interesting to see if the downgrade has an impact on buying demand for the company's shares.

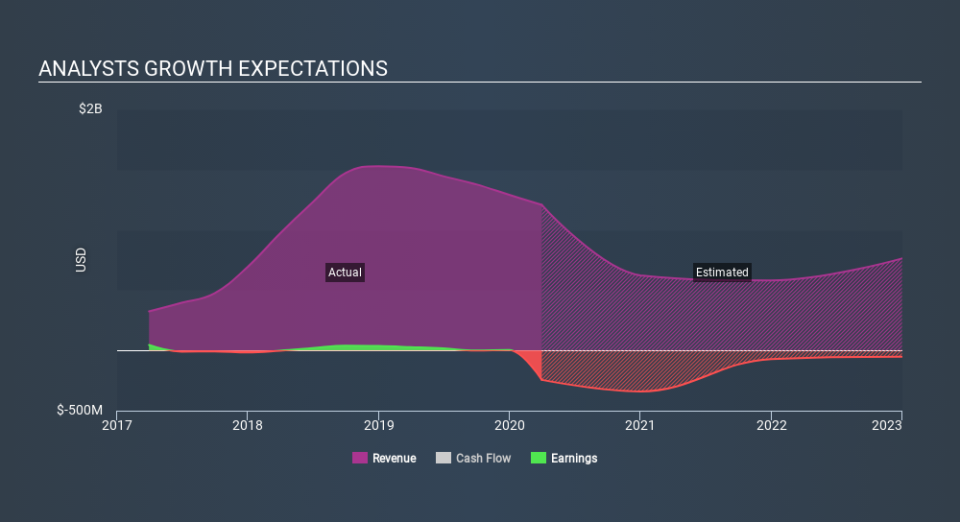

After the downgrade, the consensus from Select Energy Services' six analysts is for revenues of US$623m in 2020, which would reflect a stressful 48% decline in sales compared to the last year of performance. Per-share losses are expected to explode, reaching US$3.62 per share. However, before this estimates update, the consensus had been expecting revenues of US$712m and US$0.76 per share in losses. Ergo, there's been a clear change in sentiment, with the analysts administering a notable cut to this year's revenue estimates, while at the same time increasing their loss per share forecasts.

Check out our latest analysis for Select Energy Services

The consensus price target lifted 13% to US$4.84, clearly signalling that the weaker revenue and EPS outlook are not expected to weigh on the stock over the longer term. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on Select Energy Services, with the most bullish analyst valuing it at US$6.65 and the most bearish at US$3.00 per share. This is a fairly broad spread of estimates, suggesting that the analysts are forecasting a wide range of possible outcomes for the business.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. These estimates imply that sales are expected to slow, with a forecast revenue decline of 48%, a significant reduction from annual growth of 35% over the last three years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 0.05% next year. It's pretty clear that Select Energy Services' revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that analysts increased their loss per share estimates for this year. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. The rising price target is a puzzle, but still - with a serious cut to this year's outlook, we wouldn't be surprised if investors were a bit wary of Select Energy Services.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Select Energy Services analysts - going out to 2022, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.