How Consolidated Edison, Inc. Has Managed to Raise Its Dividend for 44 Years

At first blush, there's nothing all that exciting about Consolidated Edison, Inc.'s (NYSE: ED) business -- until you look at the utility's incredible dividend history. To put it mildly, 44 years worth of annual dividend increases isn't something that happens by accident. If you're a dividend investor looking for a reliable income stock, Con Ed is likely to show up in your stock screens. Here's a quick look at what the company does that supports such an incredible dividend streak.

A solid "core"

Consolidated Edison is a holding company that operates in and around New York City. The Big Apple is a vibrant market, with notable scale in finance and, increasingly, technology. It is also a huge tourist destination. For a utility, operating in a region with population growth is a key benefit because it means an increasing customer base. The population of New York City totals around 8.6 million (up 5.5% since 2010), with projections calling for it to continue expanding through 2040, when the population is expected to reach roughly 9 million people.

Image source: Getty Images.

Put another way, the region in which Con Ed operates is a good one. However, the utility isn't focused just on New York City. It also operates in local suburbs in the counties of Westchester and Rockland, and in parts of New Jersey. All of these regions benefit from the allure of New York City's job market, entertainment options, and overall lifestyle. While southern markets are drawing an increasing number of residents, New York is a unique northeastern market that has been able to hold its own, and Con Ed has a key monopoly in serving the region's power needs.

What's key to Con Ed's dividend history is that the draw of New York City isn't new, even though it has ebbed and flowed over time. The expanding city has been the foundation on which Con Ed has been able to build its impressive dividend track record. That's the demand side, of course. What you also need to add is a conservative culture that has allowed Con Ed to avoid making the types of mistakes that cause dividend cuts, like taking on too much leverage or paying too much out in the form of dividends.

Con Ed's payout ratio has hovered between 60% and 70% for nine of the last 10 years, a reasonable level for a regulated utility. And it's debt to equity ratio has been below one for most of the last 20 years, another reasonable number. Combine a good market with a corporate culture that avoids undue risks and you start to see how Con Ed built such a great dividend track record.

A trio of assets

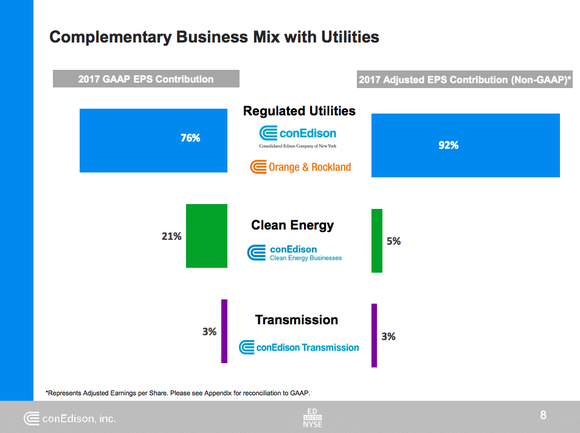

Electric and gas. Con Ed's largest business is delivering electricity and natural gas to customers. It serves roughly 3.6 million electric customers and 1.2 million gas customers. The key word here, though, is delivering. Con Ed basically passes the cost of electricity and natural gas on to customers, it owns only a small number of power plants. The power plants it owns, meanwhile, are largely associated with a small steam delivery service located in New York City (steam is used for heating, among other things). It gets paid for maintaining the power lines and natural gas pipes that allow it to deliver these key power sources to customers.

Delivering electricity and gas makes up around 90% of the utility's adjusted earnings. And it tends to be fairly stable since the fees don't change much over time. And, in fact, tend to move higher as the rates Con Ed charges go up. As a regulated utility, however, Con Ed has to get rates approved by the government (the trade-off for having a monopoly). The only way for Con Ed to get higher rates approved is for it to spend money on improving its assets.

Consolidated Edison Dividend Overview | |

|---|---|

Current yield | 3.6% |

Most recent increase | 3% |

Payout ratio in 2017 | 69% |

Which is why capital spending is such an important metric for investors to monitor. Currently, Con Ed plans to spend $9.5 billion on its regulated assets between 2018 and 2020. That spending will go toward things like storm hardening power lines, installing smart meters, and upgrading natural gas pipes. Regulators tend to view such moves positively. Con Ed expects this spending to support rate base growth of roughly 6% a year through 2020.

Renewable power. Although a much smaller piece of the pie at 5% of adjusted earnings, the company's Clean Energy division is an important asset. This business owns renewable power assets like solar (around 80% of its clean power portfolio) and wind farms and sells the power they generate to other companies under long-term contracts. Although the core of Con Ed is its New York focused electric and gas delivery business, the Clean Energy group allows it to take advantage of the shifting trends within the power sector.

Unlike the regulated business, however, Clean Energy grows by increasing its scale with new assets. Put simply, the more power it generates the more power it can sell. Con Ed plans to spend $1.2 billion on this business between 2018 and 2020. Although Clean Energy will always be a relatively small operation, it's worth watching the progress on Con Ed's spending here.

Con Ed's main businesses, with regulated utilities leading the way. Image source: Consolidated Edison, Inc.

Moving power around. The last business, at a slim 3% of adjusted earnings, is Con Ed's Transmission division. This business owns assets that move electricity and natural gas in large quantities over long distances. Think high voltage power lines and natural gas pipelines. This business is slated to spend just $400 million between 2018 and 2020.

Although a small division, don't underestimate the value Con Ed provides here. Electricity is increasingly produced great distances away from where it is used because of the shift toward cleaner power sources. And natural gas has to travel from where it is drilled to the markets where it gets used to generate electricity and heat. While this probably isn't a huge growth engine at Con Ed, it should be a reliable business for years to come.

The sum of the parts

When you add it all up, the key features to note at Con Ed are its strong and growing customer base in and around New York City and its plans for upgrading its wires and pipes. That's what has supported the utilities ability to pay a growing dividend in recent years and what will continue to support dividend growth over time. In the shadows, however, are Con Ed's Clean Energy and Transmission businesses, both of which allow it to take advantage of the utility industry's shifting trends. That, in turn, should offset the risk that efficiency efforts and increased residential solar put a crimp in demand from Con Ed's vibrant New York marketplace.

All in, look for Con Ed to leverage this collection of assets to keep the dividend growing at around the historical rate of inflation growth as it adds to its incredible record of annual dividend increases.

More From The Motley Fool

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.