Is Corteva (NYSE:CTVA) Using Too Much Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Corteva, Inc. (NYSE:CTVA) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Corteva

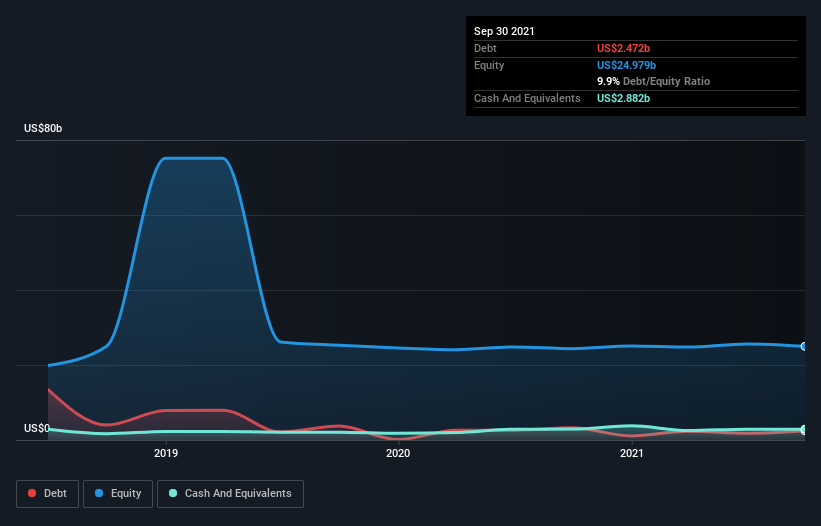

What Is Corteva's Net Debt?

The image below, which you can click on for greater detail, shows that Corteva had debt of US$2.47b at the end of September 2021, a reduction from US$3.24b over a year. But it also has US$2.88b in cash to offset that, meaning it has US$410.0m net cash.

How Strong Is Corteva's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Corteva had liabilities of US$7.81b due within 12 months and liabilities of US$8.34b due beyond that. Offsetting these obligations, it had cash of US$2.88b as well as receivables valued at US$5.84b due within 12 months. So it has liabilities totalling US$7.42b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Corteva is worth a massive US$35.0b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. While it does have liabilities worth noting, Corteva also has more cash than debt, so we're pretty confident it can manage its debt safely.

In addition to that, we're happy to report that Corteva has boosted its EBIT by 68%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Corteva's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Corteva has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Corteva actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing up

Although Corteva's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$410.0m. The cherry on top was that in converted 126% of that EBIT to free cash flow, bringing in US$1.9b. So is Corteva's debt a risk? It doesn't seem so to us. We'd be very excited to see if Corteva insiders have been snapping up shares. If you are too, then click on this link right now to take a (free) peek at our list of reported insider transactions.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.