Is CPI Computer Peripherals International (ATH:CPI) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, CPI Computer Peripherals International (ATH:CPI) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for CPI Computer Peripherals International

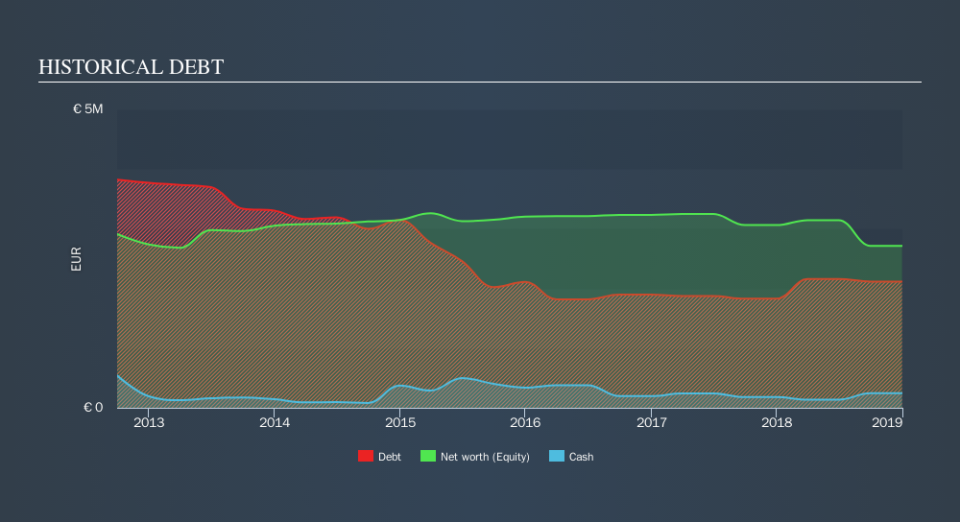

What Is CPI Computer Peripherals International's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2018 CPI Computer Peripherals International had €2.12m of debt, an increase on €1.83m, over one year. However, it also had €245.2k in cash, and so its net debt is €1.87m.

A Look At CPI Computer Peripherals International's Liabilities

According to the last reported balance sheet, CPI Computer Peripherals International had liabilities of €6.25m due within 12 months, and liabilities of €100.7k due beyond 12 months. Offsetting these obligations, it had cash of €245.2k as well as receivables valued at €3.52m due within 12 months. So it has liabilities totalling €2.58m more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of €2.77m. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

CPI Computer Peripherals International shareholders face the double whammy of a high net debt to EBITDA ratio (6.4), and fairly weak interest coverage, since EBIT is just 1.1 times the interest expense. This means we'd consider it to have a heavy debt load. The good news is that CPI Computer Peripherals International grew its EBIT a smooth 79% over the last twelve months. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since CPI Computer Peripherals International will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, CPI Computer Peripherals International saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both CPI Computer Peripherals International's interest cover and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Looking at the bigger picture, it seems clear to us that CPI Computer Peripherals International's use of debt is creating risks for the company. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. Even though CPI Computer Peripherals International lost money on the bottom line, its positive EBIT suggests the business itself has potential. So you might want to check outhow earnings have been trending over the last few years.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.