Crane (CR) to Report Q4 Earnings: What's in the Offing?

Crane Co. CR is scheduled to release fourth-quarter 2021 results on Jan 24, after market close.

The company delivered better-than-expected results in three of the last four quarters, while lagging estimates once. The average earnings surprise is 22.02%. In the last reported quarter, the company’s earnings of $1.89 surpassed the Zacks Consensus Estimate of $1.37 by 37.96%.

In the past three months, shares of Crane have gained 8.3% against the industry’s decline of 4.2%.

Image Source: Zacks Investment Research

Let us delve deeper.

Key Factors & Estimates for Q4

For the fourth quarter, Crane anticipates the Aerospace & Electronics segment’s sales to be similar to the third-quarter reported figure. Improved demand in the commercial aerospace end markets is likely to have favored the aftermarket and OEM businesses in the quarter. However, revenue mix and the timing of projects are predicted to have adversely impacted margins. Considering the full year, the segment’s sales are predicted to decline slightly on a year-over-year basis.

The Zacks Consensus Estimate for Aerospace & Electronics’ revenues is expected to be $162 million, suggesting a 13.3% increase from the year-ago reported figure and a fall of 4.1% from the previous quarter’s number.

The company expects revenue mix and seasonality to affect the quarterly results of Process Flow Technologies. Sequentially, both revenues and margins are predicted to decline. Strength across the general industrial and chemical markets is likely to have benefited. Sales growth in the low-double-digit range is expected for 2021.The consensus estimate for Process Flow Technologies’ revenues is pegged at $273 million, suggesting a 5.8% increase from the year-ago quarter’s reported figure and a decline of 8.7% from the previous quarter’s number.

Payment & Merchandising Technologies’ sales are predicted to decline sequentially in the fourth quarter. Margins are also expected to moderate to the high-teens range. On a year-over-year basis, the quarter’s sales are predicted to improve. The consensus estimate for the segment’s revenues is pegged at $302 million, implying a 6.7% increase from the figure reported a year ago and a 17.5% decrease sequentially.

Then again, Crane’s solid product offerings, strengthening end markets and synergistic gains from buyouts are anticipated to have benefited the fourth-quarter performance. Its healthy liquidity position and shareholder-friendly policies as well as lower taxes are expected to have been other tailwinds. High corporate expenses and supply-chain restrictions are likely to have ailed.

The Zacks Consensus Estimate for fourth-quarter revenues of $744 million suggests a 2.5% increase from the year-ago reported figure and a 10.8% decrease from the previous quarter’s number. Earnings estimates are pegged at $1.12 per share, suggesting growth of 12% from the year-ago quarter and a 40.7% fall from the previous quarter.

Earnings Whispers

Our proven model does not conclusively suggest an earnings beat for Crane this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of beating estimates. That is not the case with Crane as shown below. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Earnings ESP: Crane has an Earnings ESP of 0.00% as both the Most Accurate Estimate and the Zacks Consensus Estimate are pegged at $1.12.

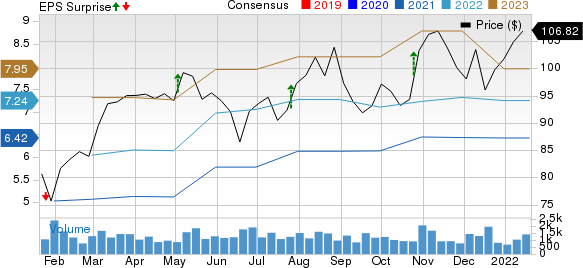

Crane Co. Price, Consensus and EPS Surprise

Crane Co. price-consensus-eps-surprise-chart | Crane Co. Quote

Zacks Rank: Crane currently carries a Zacks Rank #4 (Sell).

Stocks to Consider

Here are some companies that you may want to consider as, according to our model, these have the right combination of elements to beat on earnings this reporting cycle.

UFP Technologies, Inc. UFPT currently has an Earnings ESP of +8.77% and is a Zacks #1 Ranked player. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for UFP Technologies’ earnings is pegged at 57 cents per share for the fourth quarter of 2021. The company delivered better-than-expected results in three of the last four quarters, while lagging estimates once. The average earnings surprise for UFPT is 22.90%.

AGCO Corporation AGCO presently has an Earnings ESP of +25.00% and a Zacks Rank of 2.

For the fourth quarter of 2021, the Zacks Consensus Estimate for AGCO’s earnings is pegged at $1.72 per share. The company delivered better-than-expected results for the fourth quarter of 2021, with an average earnings surprise of 47.53%.

3M Company MMM currently has an Earnings ESP of +0.21% and a Zacks Rank #3.

The Zacks Consensus Estimate for 3M’s earnings is pegged at $2.03 per share for the fourth quarter of 2021. In the last four quarters, the company’s results were better than expected, with an average earnings surprise of 14.82%.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

3M Company (MMM) : Free Stock Analysis Report

AGCO Corporation (AGCO) : Free Stock Analysis Report

UFP Technologies, Inc. (UFPT) : Free Stock Analysis Report

Crane Co. (CR) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research