Are Davide Campari-Milano S.p.A.’s (BIT:CPR) Interest Costs Too High?

The size of Davide Campari-Milano S.p.A. (BIT:CPR), a €9.0b large-cap, often attracts investors seeking a reliable investment in the stock market. Big corporations are much sought after by risk-averse investors who find diversified revenue streams and strong capital returns attractive. However, the health of the financials determines whether the company continues to succeed. Today we will look at Davide Campari-Milano’s financial liquidity and debt levels, which are strong indicators for whether the company can weather economic downturns or fund strategic acquisitions for future growth. Note that this information is centred entirely on financial health and is a high-level overview, so I encourage you to look further into CPR here.

See our latest analysis for Davide Campari-Milano

Want to help shape the future of investing tools and platforms? Take the survey and be part of one of the most advanced studies of stock market investors to date.

How does CPR’s operating cash flow stack up against its debt?

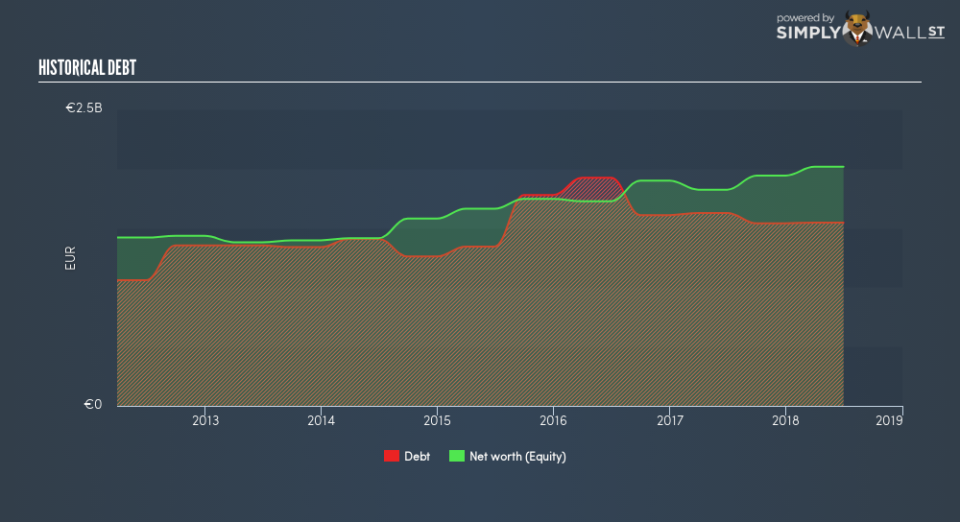

CPR has shrunken its total debt levels in the last twelve months, from €1.6b to €1.5b , which includes long-term debt. With this reduction in debt, CPR currently has €588m remaining in cash and short-term investments , ready to deploy into the business. On top of this, CPR has produced €319m in operating cash flow over the same time period, resulting in an operating cash to total debt ratio of 21%, signalling that CPR’s operating cash is sufficient to cover its debt. This ratio can also be a sign of operational efficiency as an alternative to return on assets. In CPR’s case, it is able to generate 0.21x cash from its debt capital.

Does CPR’s liquid assets cover its short-term commitments?

At the current liabilities level of €434m, the company has been able to meet these obligations given the level of current assets of €1.5b, with a current ratio of 3.42x. However, many consider a ratio above 3x to be high, although this is not necessarily a bad thing.

Is CPR’s debt level acceptable?

With debt reaching 77% of equity, CPR may be thought of as relatively highly levered. This is common amongst large-cap companies because debt can often be a less expensive alternative to equity due to tax deductibility of interest payments. Accordingly, large companies often have an advantage over small-caps through lower cost of capital due to cheaper financing. The sustainability of CPR’s debt levels can be assessed by comparing the company’s interest payments to earnings. As a rule of thumb, a company should have earnings before interest and tax (EBIT) of at least three times the size of net interest. In CPR’s case, the ratio of 15.96x suggests that interest is comfortably covered. It is considered a responsible and reassuring practice to maintain high interest coverage, which makes CPR and other large-cap investments thought to be safe.

Next Steps:

At its current level of cash flow coverage, CPR has room for improvement to better cushion for events which may require debt repayment. However, the company exhibits an ability to meet its near-term obligations, which isn’t a big surprise for a large-cap. Keep in mind I haven’t considered other factors such as how CPR has been performing in the past. You should continue to research Davide Campari-Milano to get a more holistic view of the stock by looking at:

Future Outlook: What are well-informed industry analysts predicting for CPR’s future growth? Take a look at our free research report of analyst consensus for CPR’s outlook.

Valuation: What is CPR worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether CPR is currently mispriced by the market.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.