Declining Stock and Solid Fundamentals: Is The Market Wrong About Gateley (Holdings) Plc (LON:GTLY)?

Gateley (Holdings) (LON:GTLY) has had a rough three months with its share price down 17%. However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. In this article, we decided to focus on Gateley (Holdings)'s ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

See our latest analysis for Gateley (Holdings)

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Gateley (Holdings) is:

25% = UK£14m ÷ UK£58m (Based on the trailing twelve months to October 2021).

The 'return' refers to a company's earnings over the last year. So, this means that for every £1 of its shareholder's investments, the company generates a profit of £0.25.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Gateley (Holdings)'s Earnings Growth And 25% ROE

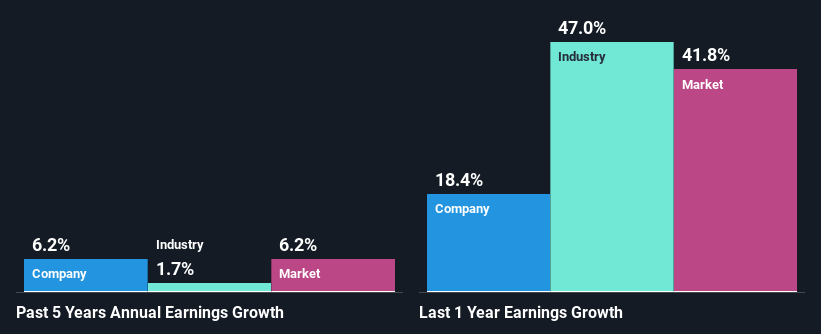

Firstly, we acknowledge that Gateley (Holdings) has a significantly high ROE. Second, a comparison with the average ROE reported by the industry of 11% also doesn't go unnoticed by us. This probably laid the groundwork for Gateley (Holdings)'s moderate 6.2% net income growth seen over the past five years.

Next, on comparing with the industry net income growth, we found that Gateley (Holdings)'s growth is quite high when compared to the industry average growth of 1.7% in the same period, which is great to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Has the market priced in the future outlook for GTLY? You can find out in our latest intrinsic value infographic research report.

Is Gateley (Holdings) Using Its Retained Earnings Effectively?

The high three-year median payout ratio of 60% (or a retention ratio of 40%) for Gateley (Holdings) suggests that the company's growth wasn't really hampered despite it returning most of its income to its shareholders.

Additionally, Gateley (Holdings) has paid dividends over a period of six years which means that the company is pretty serious about sharing its profits with shareholders. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 61%.

Conclusion

Overall, we are quite pleased with Gateley (Holdings)'s performance. In particular, its high ROE is quite noteworthy and also the probable explanation behind its considerable earnings growth. Yet, the company is retaining a small portion of its profits. Which means that the company has been able to grow its earnings in spite of it, so that's not too bad. So far, we've only made a quick discussion around the company's earnings growth. You can do your own research on Gateley (Holdings) and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.