You Definitely Should Buy Celgene Corporation Stock After Earnings Beat

On Thursday before the open, Celgene Corporation (NASDAQ:CELG) reported its fourth-quarter earnings results. The company beat on earnings per share and revenue expectations. It also provided good, but not great guidance (more on that in a minute). CELG stock is up moderately in Thursday’s trading session as a result.

Is this investors’ last chance to buy the biotech giant?

First, let’s digest some of this new information. Earnings per share of $2 came in 3 cents ahead of expectations. Revenue results were ahead of forecasts too, growing almost 17% year-over-year. 2018 guidance is the big focus point though.

InvestorPlace - Stock Market News, Stock Advice & Trading Tips

Management is guiding for sales of $14.4 billion to $14.8 billion. This is short of analysts’ forecasts calling for $14.82 billion. However, management’s call for non-GAAP earnings per share of $8.70 to $8.90 is ahead of consensus expectations calling for $8.64 per share.

Although revenue is still forecast to climb about 12.5% year-over-year, this is disappointing to some as it’s below consensus expectations. Is management being conservative? We can only hope, but we are not certain.

On the flip side, earnings came in strong. Because of the mix between exceeding earnings guidance and disappointing sales guidance, shares aren’t moving a whole lot.

Breaking Down CELG Stock

While the market seems mixed on Celgene’s earnings results, I for one am relieved. CELG stock fell from $148 to less than $100 inside of a four-week stretch in October. That’s terrible!

Given that fall, shares now trade with a paltry valuation. While CELG stock trades with a price-to-earnings (P/E) ratio of 24, it trades at just 11.7 times 2018 estimates. If all goes to plan this year, earnings will grow a hair under 19%, going along with double-digit sales growth. That’s dirt cheap if you ask me.

Investors are willing to discount CELG stock to such extremes on fear that its pipeline is drying up. I don’t think that’s the case, as Celgene has become a stalwart in the biotech sector. Further, its M&A strategy is built around keeping its pipeline robust. While at times there are setbacks, CELG overall has an excellent business that’s being undervalued by the market.

The company disappointed investors in October, there’s no doubt it. But this quarter should be met with relief, as the situation isn’t getting worse; they didn’t disappoint and actually gave a solid outlook. Investors will hopefully realize this sooner rather than later and buy in at today’s low valuation.

Unlike some of its peers, such as Eli Lilly and Co (NYSE:LLY), Pfizer Inc. (NYSE:PFE) or Merck & Co., Inc. (NYSE:MRK), Celgene doesn’t pay a dividend. For some, that’s a game-changer, as they need some form of income.

For me, I’m okay with Celgene’s capital strategy. While Celgene’s deal for Juno Therapeutics Inc (NASDAQ:JUNO) was pricey, it could pay off in the future.

Trading CELG

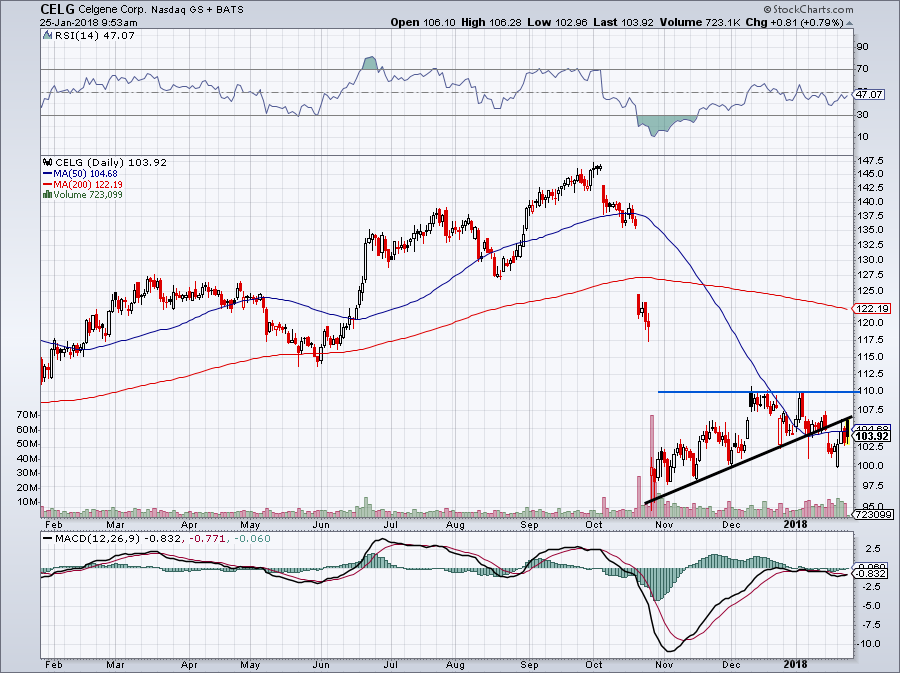

CELG stock does not have a very bullish chart. Back in October, we pointed out that long-term support sat right at $95. Ultimately, we went long CELG near $100. Although the technicals aren’t pretty, the fundamentals are too strong to ignore.

You’ll see what I mean on the chart. From its lows in October, Celgene stock was making an orderly move higher. It even got back above its 50-day moving average. However, 2018 has been tough on CELG. It fell below the 50-day and is still below trend-line support.

What now? Celgene stock needs to take some baby steps. The first positive move would be a close above the 50-day, then back above trend-line support. That would require a move north of $107.50.

I don’t want to get ahead of my skis here, but over trend-line support and $110 becomes the new target. If Celgene can get above that level of resistance, $120 is a conservative target.

Conversely, a breakdown and close below $95 makes me bearish CELG stock and likely forces a stop-out. As it stands though, this is a very cheap, very good company with an excellent risk-reward. Even a move back to “just” $120 is a return of nearly 20% from these levels.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell had a position in CELG.

More from InvestorPlace

The post You Definitely Should Buy Celgene Corporation Stock After Earnings Beat appeared first on InvestorPlace.