Can Demographic Tailwinds Drive HCP's Earnings This Season?

HCP Inc. HCP is slated to report third-quarter 2018 results on Oct 31, before the opening bell. Though the company’s performance will likely reflect a year-over-year decline in funds from operations (FFO), its top-line results are anticipated to display growth.

In the last reported quarter, this Irvine, CA-based healthcare REIT delivered a positive surprise of 2.17%, in terms of adjusted FFO per share. Results reflected better-than-expected revenue numbers for the Apr-Jun quarter.

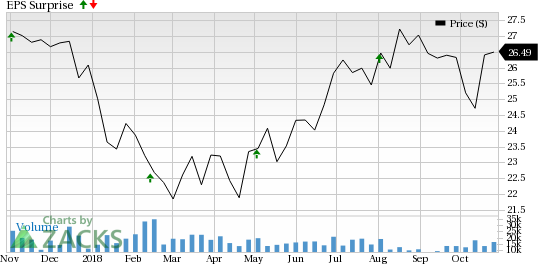

The company has an impressive surprise history. In fact, over the trailing four quarters, this REIT exceeded estimates in each occasion, coming up with an average positive beat of 3.25%. This is depicted in the graph below.

HCP, Inc. Price and EPS Surprise

HCP, Inc. Price and EPS Surprise | HCP, Inc. Quote

Let’s see how things are shaping up, prior to this announcement.

Factors to Consider

Per an article by National Investment Center for Seniors Housing & Care (NIC), fundamentals of the senior housing real estate assets remained soft in the third quarter. In fact, occupancy rate for seniors housing (including properties still in lease up) shrunk 80 basis points (bps) year over year to 87.9%, marking the lowest dip since second-quarter 2011. Nonetheless, same-store asking rent for seniors housing was up 2.7% sequentially.

Understandably, the company is expected to have witnessed a decline in its senior housing portfolio occupancy. Nonetheless, net operating income for this segment is expected to be up moderately 2.3% as compared to the prior quarter to $37.44 million, while revenues might have remained flat at $138 million.

In the quarter under review, the company is likely to have gained from rising healthcare spending and growing aging population. In fact, the Zacks Consensus Estimate for rental and related revenues of $280 million indicates a year-over-year increase of 5.3%. Also, total revenues for the Sep-end quarter are projected at nearly $457.45 million — reflecting a year-over year increase of 0.76%.

In its life-science segment, we estimate occupancy and revenues to have remained sequentially flat at 96% and $78 million, respectively.

Further, rising interest rates is another unfavorable development for the company. Since healthcare REITs have substantial exposure to long-term leased assets that are subject to annual escalations, this REIT sector is the most sensitive to interest rate hikes. Therefore, a higher interest rate is likely to have raised the cost of debt, which, in turn, is likely to have affected the company’s profitability in the Jul-Sep quarter.

In fact, HCP’s activities during the quarter were inadequate to gain analyst confidence. Consequently, the Zacks Consensus Estimate for Q3 FFO remained unchanged at 43 cents in a month’s time. Furthermore, it indicates a 10.42% year-over-year decline.

Earnings Whispers

Our proven model does not show that HCP has the right combination of the two key ingredients — positive Earnings ESP and a Zacks Rank #3 (Hold) or better — to increase the odds of an earnings beat in the third quarter.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Earnings ESP: The Earnings ESP for HCP is 0.00%.

Zacks Rank: HCP carries a Zacks Rank of 3, at present.

Stocks That Warrant a Look

Here are a few stocks in the REIT sector that you may want to consider, as our model shows that these have the right combination of elements to report a positive surprise this quarter:

Ashford Hospitality Trust AHT, scheduled to release earnings on Nov 1, has an Earnings ESP of +7.14% and a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Douglas Emmett, Inc. DEI, slated to report Sep-end quarter results on Nov 1, has an Earnings ESP of +0.44% and a Zacks Rank of 3.

SBA Communications Corporation SBAC, set to release quarterly figures on Nov 5, has an Earnings ESP of +1.29% and a Zacks Rank of 3.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2020.

Click here for the 6 trades >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

SBA Communications Corporation (SBAC) : Free Stock Analysis Report

Douglas Emmett, Inc. (DEI) : Free Stock Analysis Report

HCP, Inc. (HCP) : Free Stock Analysis Report

Ashford Hospitality Trust Inc (AHT) : Free Stock Analysis Report

To read this article on Zacks.com click here.