Did Albany International Corp (NYSE:AIN) Use Debt To Deliver Its ROE Of 12%?

Many investors are still learning about the various metrics that can be useful when analysing a stock. This article is for those who would like to learn about Return On Equity (ROE). To keep the lesson grounded in practicality, we’ll use ROE to better understand Albany International Corp (NYSE:AIN).

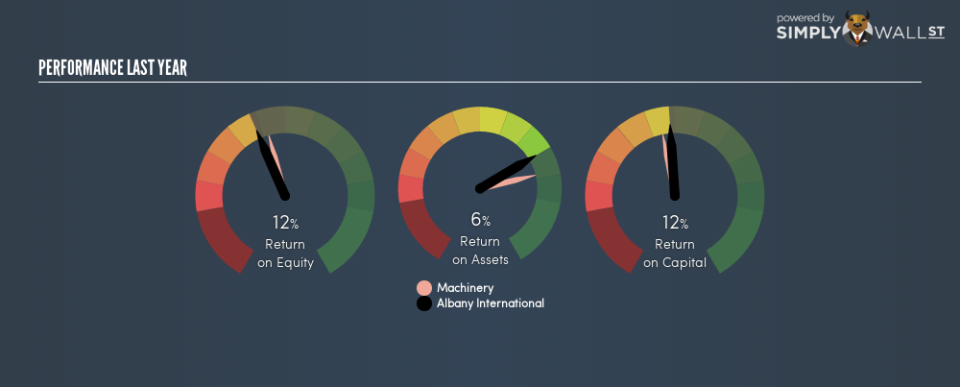

Our data shows Albany International has a return on equity of 12% for the last year. One way to conceptualize this, is that for each $1 of shareholders’ equity it has, the company made $0.12 in profit.

View our latest analysis for Albany International

How Do I Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit ÷ Shareholders’ Equity

Or for Albany International:

12% = US$75m ÷ US$609m (Based on the trailing twelve months to September 2018.)

Most know that net profit is the total earnings after all expenses, but the concept of shareholders’ equity is a little more complicated. It is all the money paid into the company from shareholders, plus any earnings retained. The easiest way to calculate shareholders’ equity is to subtract the company’s total liabilities from the total assets.

What Does Return On Equity Signify?

Return on Equity measures a company’s profitability against the profit it has kept for the business (plus any capital injections). The ‘return’ is the yearly profit. The higher the ROE, the more profit the company is making. So, as a general rule, a high ROE is a good thing. Clearly, then, one can use ROE to compare different companies.

Does Albany International Have A Good Return On Equity?

One simple way to determine if a company has a good return on equity is to compare it to the average for its industry. Importantly, this is far from a perfect measure, because companies differ significantly within the same industry classification. If you look at the image below, you can see Albany International has a similar ROE to the average in the machinery industry classification (14%).

That’s neither particularly good, nor bad. Generally it will take a while for decisions made by leadership to impact the ROE. So I like to check the tenure of the board and CEO, before reaching any conclusions.

How Does Debt Impact Return On Equity?

Most companies need money — from somewhere — to grow their profits. That cash can come from issuing shares, retained earnings, or debt. In the first two cases, the ROE will capture this use of capital to grow. In the latter case, the debt used for growth will improve returns, but won’t affect the total equity. Thus the use of debt can improve ROE, albeit along with extra risk in the case of stormy weather, metaphorically speaking.

Albany International’s Debt And Its 12% ROE

While Albany International does have some debt, with debt to equity of just 0.87, we wouldn’t say debt is excessive. The combination of modest debt and a very respectable ROE suggests this is a business worth watching. Judicious use of debt to improve returns can certainly be a good thing, although it does elevate risk slightly and reduce future optionality.

The Key Takeaway

Return on equity is useful for comparing the quality of different businesses. In my book the highest quality companies have high return on equity, despite low debt. If two companies have the same ROE, then I would generally prefer the one with less debt.

But when a business is high quality, the market often bids it up to a price that reflects this. Profit growth rates, versus the expectations reflected in the price of the stock, are a particularly important to consider. So you might want to check this FREE visualization of analyst forecasts for the company.

Of course Albany International may not be the best stock to buy. So you may wish to see this free collection of other companies that have high ROE and low debt.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.