Did Raymond Limited (NSE:RAYMOND) Use Debt To Deliver Its ROE Of 7.9%?

One of the best investments we can make is in our own knowledge and skill set. With that in mind, this article will work through how we can use Return On Equity (ROE) to better understand a business. We'll use ROE to examine Raymond Limited (NSE:RAYMOND), by way of a worked example.

Over the last twelve months Raymond has recorded a ROE of 7.9%. One way to conceptualize this, is that for each ₹1 of shareholders' equity it has, the company made ₹0.079 in profit.

Check out our latest analysis for Raymond

How Do I Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit ÷ Shareholders' Equity

Or for Raymond:

7.9% = ₹1.5b ÷ ₹20b (Based on the trailing twelve months to June 2019.)

Most know that net profit is the total earnings after all expenses, but the concept of shareholders' equity is a little more complicated. It is the capital paid in by shareholders, plus any retained earnings. The easiest way to calculate shareholders' equity is to subtract the company's total liabilities from the total assets.

What Does ROE Signify?

ROE looks at the amount a company earns relative to the money it has kept within the business. The 'return' is the amount earned after tax over the last twelve months. That means that the higher the ROE, the more profitable the company is. So, as a general rule, a high ROE is a good thing. Clearly, then, one can use ROE to compare different companies.

Does Raymond Have A Good Return On Equity?

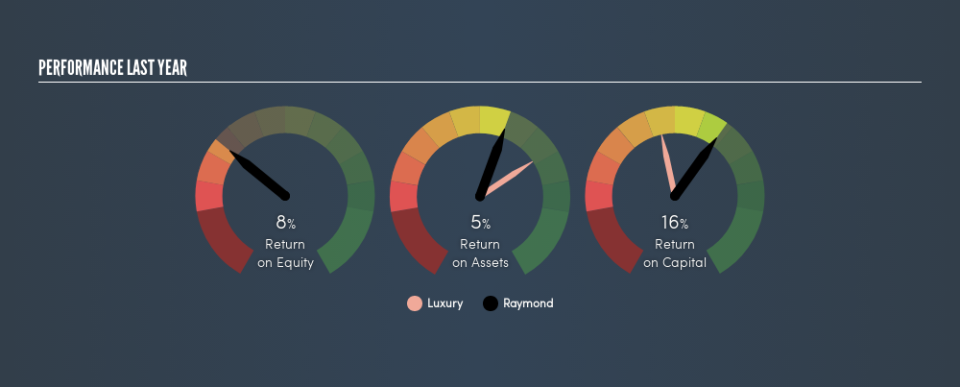

One simple way to determine if a company has a good return on equity is to compare it to the average for its industry. However, this method is only useful as a rough check, because companies do differ quite a bit within the same industry classification. You can see in the graphic below that Raymond has an ROE that is fairly close to the average for the Luxury industry (7.9%).

That isn't amazing, but it is respectable. ROE tells us about the quality of the business, but it does not give us much of an idea if the share price is cheap. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Why You Should Consider Debt When Looking At ROE

Virtually all companies need money to invest in the business, to grow profits. The cash for investment can come from prior year profits (retained earnings), issuing new shares, or borrowing. In the case of the first and second options, the ROE will reflect this use of cash, for growth. In the latter case, the debt required for growth will boost returns, but will not impact the shareholders' equity. Thus the use of debt can improve ROE, albeit along with extra risk in the case of stormy weather, metaphorically speaking.

Combining Raymond's Debt And Its 7.9% Return On Equity

Raymond clearly uses a significant amount of debt to boost returns, as it has a debt to equity ratio of 1.21. With a fairly low ROE, and significant use of debt, it's hard to get excited about this business at the moment. Debt does bring extra risk, so it's only really worthwhile when a company generates some decent returns from it.

The Bottom Line On ROE

Return on equity is useful for comparing the quality of different businesses. Companies that can achieve high returns on equity without too much debt are generally of good quality. If two companies have the same ROE, then I would generally prefer the one with less debt.

But when a business is high quality, the market often bids it up to a price that reflects this. Profit growth rates, versus the expectations reflected in the price of the stock, are a particularly important to consider. So you might want to take a peek at this data-rich interactive graph of forecasts for the company.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.