Does Coca-Cola Amatil Limited’s (ASX:CCL) Debt Level Pose A Serious Problem?

Mid-caps stocks, like Coca-Cola Amatil Limited (ASX:CCL) with a market capitalization of AUD A$5.92B, aren’t the focus of most investors who prefer to direct their investments towards either large-cap or small-cap stocks. However, generally ignored mid-caps have historically delivered better risk adjusted returns than both of those groups, primarily due to seasoned executives running a lean corporate structure. I’ve put together a small checklist, which I believe provides a ballpark estimate of their financial health status. View our latest analysis for Coca-Cola Amatil

Can CCL service its debt comfortably?

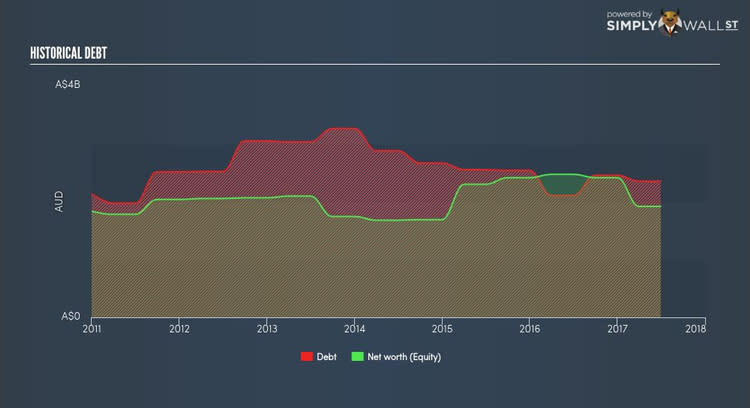

Debt-to-equity ratio tells us how much of the asset debtors could claim if the company went out of business. In the case of CCL, the debt-to-equity ratio is over 100%, which indicates that the company is holding a high level of debt relative to its net worth. In the event of financial turmoil, the company may experience difficulty meeting interest and other debt obligations. We can test if CCL’s debt levels are sustainable by measuring interest payments against earnings of a company. Ideally, earnings should cover interest by at least three times, therefore reducing concerns when profit is highly volatile. CCL’s profits amply covers interest at 10.09 times, which is seen as relatively safe. Debtors may be willing to loan the company more money, giving CCL ample headroom to grow its debt facilities.

Can CCL meet its short-term obligations with the cash in hand?

Another important aspect of financial health is liquidity: the company’s ability to meet short-term obligations, including payments to suppliers and employees. If an adverse event occurs, the company may be forced to pay these immediate expenses with its liquid assets. We need to assess CCL’s cash and other liquid assets against its upcoming expenses. Our analysis shows that CCL is able to meet its upcoming commitments with its cash and other short-term assets, which lessens our concerns for the company’s business operations should any unfavourable circumstances arise.

Next Steps:

Are you a shareholder? CCL’s high cash coverage means that, although its debt levels are high, investors shouldn’t panic since the company is able to utilise its borrowings efficiently in order to generate cash flow. Since CCL’s capital structure may change over time, I encourage examining market expectations for CCL’s future growth on our free analysis platform.

Are you a potential investor? Although understanding the serviceability of debt is important when evaluating which companies are viable investments, it shouldn’t be the deciding factor. After all, debt is often used to fund or accelerate new projects that are expected to improve a company’s growth trajectory in the longer term. CCL’s Return on Capital Employed (ROCE) in order to see management’s track record at deploying funds in high-returning projects.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.