Does Fire & Flower Holdings (TSE:FAF) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Fire & Flower Holdings Corp. (TSE:FAF) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Fire & Flower Holdings

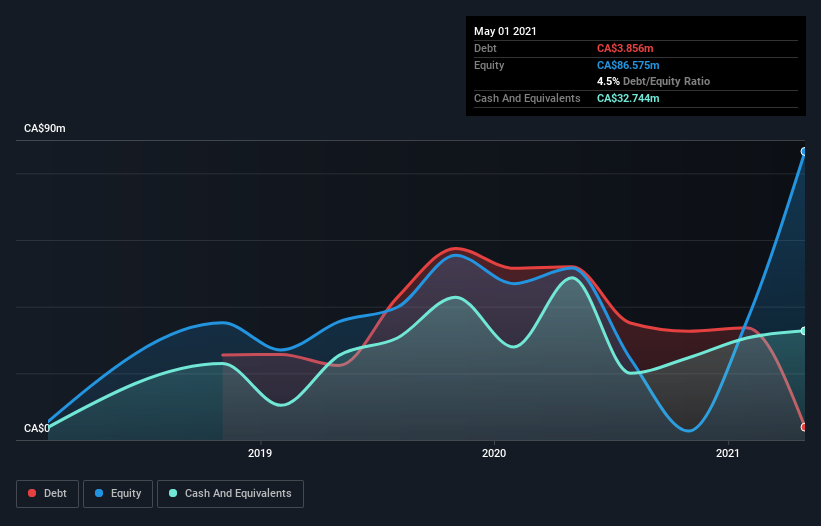

How Much Debt Does Fire & Flower Holdings Carry?

As you can see below, Fire & Flower Holdings had CA$3.86m of debt at May 2021, down from CA$52.0m a year prior. But it also has CA$32.7m in cash to offset that, meaning it has CA$28.9m net cash.

How Strong Is Fire & Flower Holdings' Balance Sheet?

According to the last reported balance sheet, Fire & Flower Holdings had liabilities of CA$34.9m due within 12 months, and liabilities of CA$100.1m due beyond 12 months. Offsetting these obligations, it had cash of CA$32.7m as well as receivables valued at CA$8.98m due within 12 months. So it has liabilities totalling CA$93.2m more than its cash and near-term receivables, combined.

Fire & Flower Holdings has a market capitalization of CA$366.6m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. Despite its noteworthy liabilities, Fire & Flower Holdings boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Fire & Flower Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Fire & Flower Holdings reported revenue of CA$149m, which is a gain of 131%, although it did not report any earnings before interest and tax. So its pretty obvious shareholders are hoping for more growth!

So How Risky Is Fire & Flower Holdings?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Fire & Flower Holdings had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through CA$16m of cash and made a loss of CA$128m. Given it only has net cash of CA$28.9m, the company may need to raise more capital if it doesn't reach break-even soon. Importantly, Fire & Flower Holdings's revenue growth is hot to trot. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Fire & Flower Holdings is showing 2 warning signs in our investment analysis , you should know about...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.