Does Medical Facilities (TSE:DR) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Medical Facilities Corporation (TSE:DR) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Medical Facilities

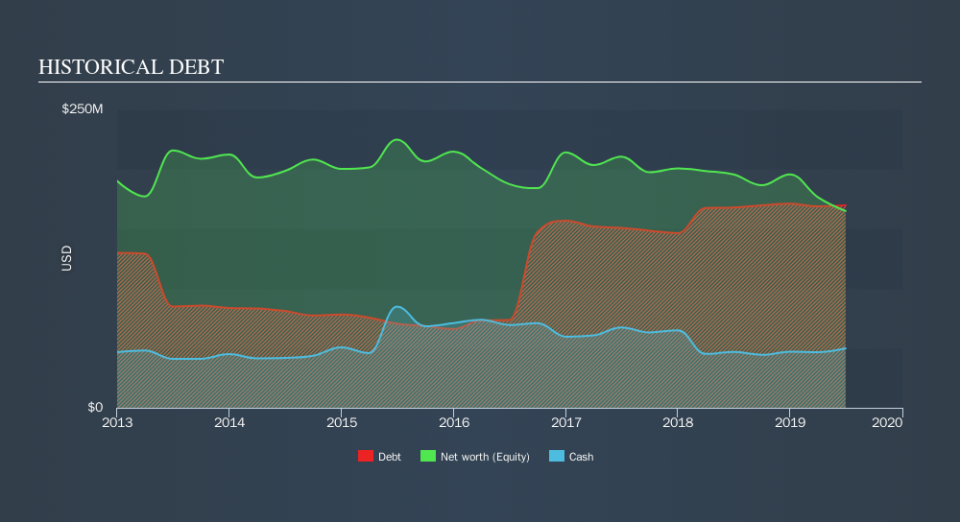

What Is Medical Facilities's Debt?

The chart below, which you can click on for greater detail, shows that Medical Facilities had US$169.7m in debt in June 2019; about the same as the year before. On the flip side, it has US$49.8m in cash leading to net debt of about US$119.9m.

How Healthy Is Medical Facilities's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Medical Facilities had liabilities of US$108.9m due within 12 months and liabilities of US$223.4m due beyond that. Offsetting these obligations, it had cash of US$49.8m as well as receivables valued at US$57.7m due within 12 months. So its liabilities total US$224.8m more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's market capitalization of US$185.4m, we think shareholders really should watch Medical Facilities's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Looking at its net debt to EBITDA of 1.4 and interest cover of 3.7 times, it seems to us that Medical Facilities is probably using debt in a pretty reasonable way. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Unfortunately, Medical Facilities's EBIT flopped 11% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Medical Facilities can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Medical Facilities generated free cash flow amounting to a very robust 85% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Our View

Medical Facilities's level of total liabilities and EBIT growth rate definitely weigh on it, in our esteem. But the good news is it seems to be able to convert EBIT to free cash flow with ease. We should also note that Healthcare industry companies like Medical Facilities commonly do use debt without problems. Taking the abovementioned factors together we do think Medical Facilities's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. While Medical Facilities didn't make a statutory profit in the last year, its positive EBIT suggests that profitability might not be far away.Click here to see if its earnings are heading in the right direction, over the medium term.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.