Third-quarter earnings season is just about over, and corporate results haven’t been this strong in eight years.

With 97% of the S&P 500 having reported results through the end of last week, the blended earnings growth rate for the S&P 500 is 25.9%, according to data from FactSet.

If this growth rate holds after 100% of reports are in, the third quarter of 2018 will mark the best earnings growth rate for a single quarter since the third quarter of 2010, a period when results were snapping back from the post-crisis collapse in profits.

To say earnings have been anything other than stellar of late is to misrepresent what is happening in corporate America. The stock market, on the other hand, has clearly been expressing concerns about a downturn in the economy. In the last six trading sessions, however, the S&P 500 has been up nearly 5% amid an abrupt shift in sentiment.

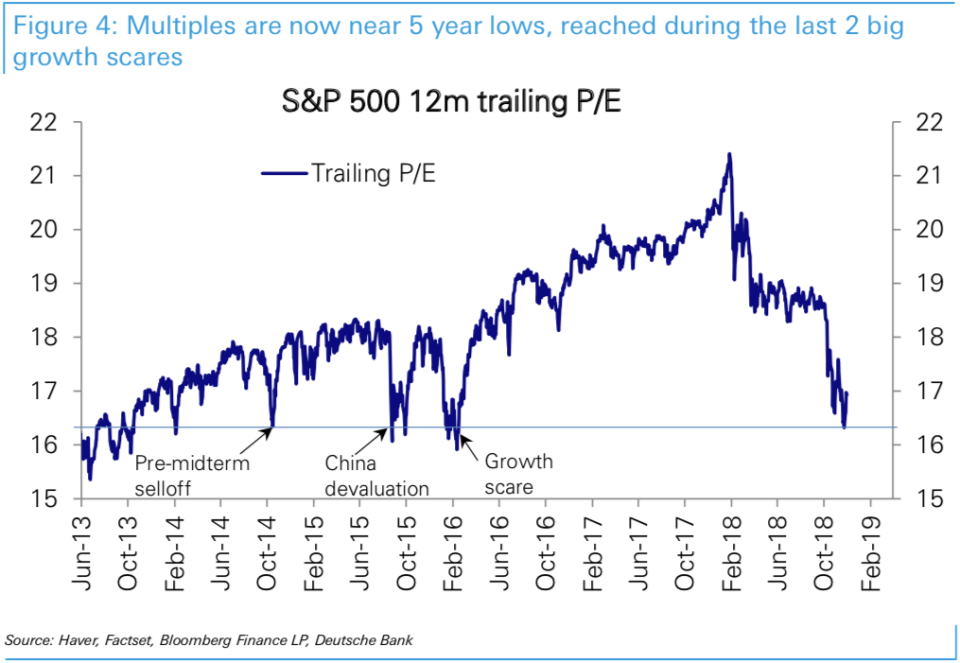

The earnings multiple on the S&P 500 this year — which most simply stated measures the amount investors will pay for $1 of corporate earnings — declined to a roughly five-year low as the price of the index advanced just 4%, according to data from Deutsche Bank. In a note to clients published last Friday, Deutsche Bank chief strategist Binky Chadha said that 2018 will mark the “year of the great de-rating.”

“2018 will mark the year of strongest earnings growth in this cycle, excluding the early years off of a low base,” Chadha writes. “S&P 500 EPS are on track to rise by 25%, boosted by the cut in the corporate tax rate (+10pp), but even adjusted for it, growth (15%) would have been the best of this cycle. Yet, with the S&P 500 up only modestly year to date, equity multiples de-rated severely.”

The last time the market’s trailing 12-month P/E ratio stood at current levels (around 16.5x the last 12 months of earnings), markets were bracing for midterm elections in 2014, grappling with a major currency adjustment from the world’s second-largest economy in 2015, and concerned about the global economy tipping into recession in early 2016.

Recent trading action, however, suggests that the sharp fall in multiples on various fears over higher rates and a slowing global economy may have been enough to snap at least some investors out of their sour moods.

As Chadha notes, during the average recession since World War II, the S&P 500 has seen a median decline of 21%. The 10% drop in stocks seen from early October through late November got investors about halfway to a market fully reacting to a recession.

“The extent of the multiple de-rating suggests a high (68%) probability of recession priced in,” Chadha writes. “The decline in equities has occurred in the context of strong growth in earnings, with the year to date decline (17%) in the multiple compared to a median decline around recessions (25%), suggesting a high probability of recession priced in.”

And with investors currently enjoying a U.S. economy adding more than 200,000 jobs per month, manufacturing data that continues to point to a solidly expanding U.S. economy, and an apparent de-escalation in trade tensions — which leaves out a Federal Reserve that last week showed signs of softening its stance on the pace of interest rate increases — it seems a 68% chance of recession was judged too high for many investors.

So while the recent trading action has been to a large extent attributed to the headline factors of a new outlook on trade and a more dovish Fed, it seems that investors had simply priced in more bad news than was available to harvest from either economic or corporate data.

And though markets are always trying to place a discounted value on future growth, the best corporate performance of the post-crisis economic cycle, at that price, simply became too much to ignore.

—

Myles Udland is a writer at Yahoo Finance. Follow him on Twitter @MylesUdland