With EPS Growth And More, Exchange Income (TSE:EIF) Makes An Interesting Case

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Exchange Income (TSE:EIF). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

View our latest analysis for Exchange Income

Exchange Income's Earnings Per Share Are Growing

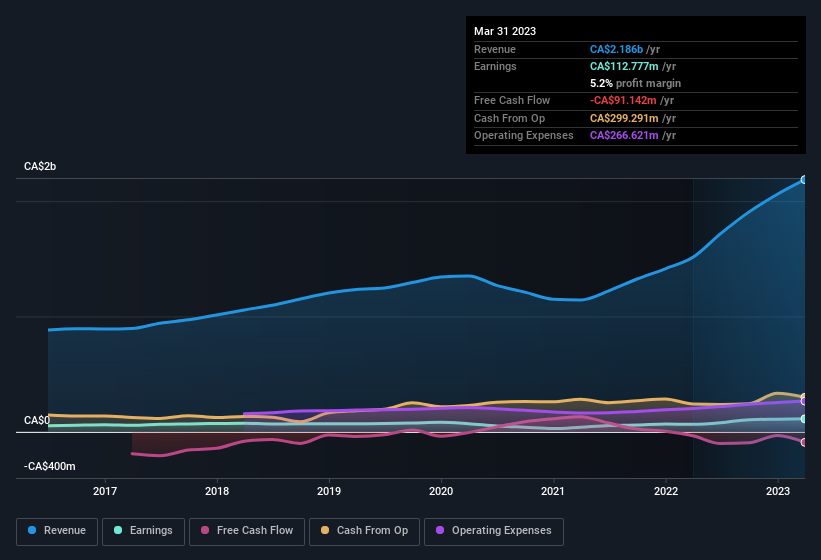

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. Exchange Income managed to grow EPS by 7.2% per year, over three years. This may not be setting the world alight, but it does show that EPS is on the upwards trend.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. The music to the ears of Exchange Income shareholders is that EBIT margins have grown from 9.3% to 12% in the last 12 months and revenues are on an upwards trend as well. Both of which are great metrics to check off for potential growth.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Exchange Income's forecast profits?

Are Exchange Income Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Despite CA$285k worth of sales, Exchange Income insiders have overwhelmingly been buying the stock, spending CA$907k on purchases in the last twelve months. This overall confidence in the company at current the valuation signals their optimism. It is also worth noting that it was Chief Corporate Development Officer Adam Terwin who made the biggest single purchase, worth CA$419k, paying CA$41.85 per share.

Along with the insider buying, another encouraging sign for Exchange Income is that insiders, as a group, have a considerable shareholding. Indeed, they hold CA$50m worth of its stock. This considerable investment should help drive long-term value in the business. While their ownership only accounts for 2.2%, this is still a considerable amount at stake to encourage the business to maintain a strategy that will deliver value to shareholders.

Is Exchange Income Worth Keeping An Eye On?

One important encouraging feature of Exchange Income is that it is growing profits. On top of that, we've seen insiders buying shares even though they already own plenty. That should do plenty in prompting budding investors to undertake a bit more research - or even adding the company to their watchlists. It is worth noting though that we have found 3 warning signs for Exchange Income (1 is potentially serious!) that you need to take into consideration.

Keen growth investors love to see insider buying. Thankfully, Exchange Income isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here