If You Like EPS Growth Then Check Out Bank of Montreal (TSE:BMO) Before It's Too Late

Some have more dollars than sense, they say, so even companies that have no revenue, no profit, and a record of falling short, can easily find investors. Unfortunately, high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson.

In contrast to all that, I prefer to spend time on companies like Bank of Montreal (TSE:BMO), which has not only revenues, but also profits. While profit is not necessarily a social good, it's easy to admire a business that can consistently produce it. Loss-making companies are always racing against time to reach financial sustainability, but time is often a friend of the profitable company, especially if it is growing.

View our latest analysis for Bank of Montreal

Bank of Montreal's Earnings Per Share Are Growing.

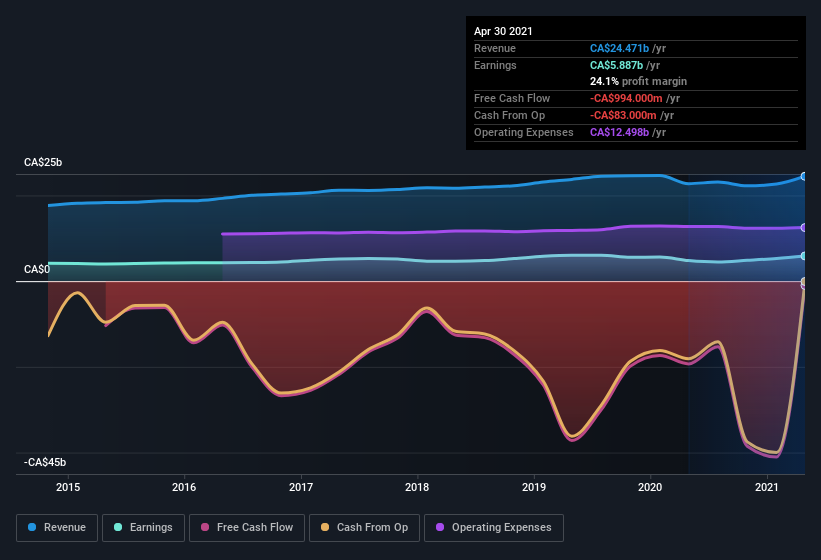

If a company can keep growing earnings per share (EPS) long enough, its share price will eventually follow. That makes EPS growth an attractive quality for any company. Over the last three years, Bank of Montreal has grown EPS by 8.4% per year. That growth rate is fairly good, assuming the company can keep it up.

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. I note that Bank of Montreal's revenue from operations was lower than its revenue in the last twelve months, so that could distort my analysis of its margins. While we note Bank of Montreal's EBIT margins were flat over the last year, revenue grew by a solid 7.6% to CA$24b. That's progress.

In the chart below, you can see how the company has grown earnings, and revenue, over time. To see the actual numbers, click on the chart.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Bank of Montreal's forecast profits?

Are Bank of Montreal Insiders Aligned With All Shareholders?

We would not expect to see insiders owning a large percentage of a CA$80b company like Bank of Montreal. But we do take comfort from the fact that they are investors in the company. To be specific, they have CA$24m worth of shares. That shows significant buy-in, and may indicate conviction in the business strategy. Despite being just 0.03% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

Does Bank of Montreal Deserve A Spot On Your Watchlist?

One positive for Bank of Montreal is that it is growing EPS. That's nice to see. If that's not enough on its own, there is also the rather notable levels of insider ownership. That combination appeals to me, for one. So yes, I do think the stock is worth keeping an eye on. We don't want to rain on the parade too much, but we did also find 1 warning sign for Bank of Montreal that you need to be mindful of.

Of course, you can do well (sometimes) buying stocks that are not growing earnings and do not have insiders buying shares. But as a growth investor I always like to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.