Estimating The Intrinsic Value Of WH Smith PLC (LON:SMWH)

I am going to run you through how I calculated the intrinsic value of WH Smith PLC (LSE:SMWH) using the discounted cash flow (DCF) method. If you want to learn more about this method, the basis for my calculations can be found in detail in the Simply Wall St analysis model. If you are reading this after April 2018 then I highly recommend you check out the latest calculation for WH Smith here.

What’s the value?

I’ve used the 2-stage growth model, which takes into account the initial higher growth stage of a company’s life cycle and the steadier growth phase over the long run. To begin, I took the analyst consensus estimates of SMWH’s levered free cash flow (FCF) over the next five years and discounted these values at the rate of 8.3%. When estimates weren’t available, I’ve extrapolated the average annual growth rate over the previous five years, capped at a reasonable level. This resulted in a present value of 5-year cash flow of UK£498.76M. Want to understand how I arrived at this number? Check out our detailed analysis here.

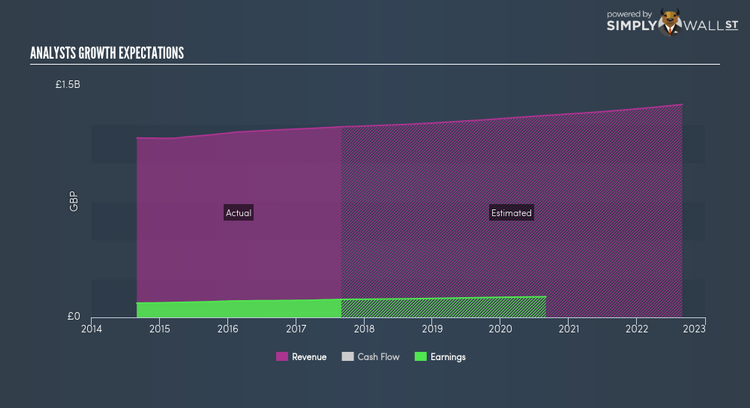

Above is a visual representation of how SMWH’s top and bottom lines are expected to move going forward, which should give you some color on SMWH’s outlook. Now we need to determine the terminal value, which is the business’s cash flow after the first stage. I’ve decided to use the 10-year government bond rate of 2.8% as the stable growth rate, which is rightly below GDP growth, but more towards the conservative side. Discounting the terminal value back five years gives us a present value of UK£1.33B.

The total value, or equity value, is then the sum of the present value of the cash flows, which in this case is UK£1.83B. The last step is to then divide the equity value by the number of shares outstanding. This results in an intrinsic value of £16.68, which, compared to the current share price of £19.79, we find that WH Smith is fair value, maybe slightly overvalued and not available at a discount at this time.

Next Steps:

Although the valuation of a company is important, it shouldn’t be the only metric you look at when researching a company.

For SMWH, there are three important aspects you should further examine:

Financial Health: Does SMWH have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

Future Earnings: How does SMWH’s growth rate compare to its peers and the wider market? Dig deeper into the analyst consensus number for the upcoming years by interacting with our free analyst growth expectation chart.

Other High Quality Alternatives: Are there other high quality stocks you could be holding instead of SMWH? Explore our interactive list of high quality stocks to get an idea of what else is out there you may be missing!

PS. The Simply Wall St app conducts a discounted cash flow for every stock on the LSE every 6 hours. If you want to find the calculation for other stocks just search here.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.