An ETF Trade for the Summertime Blues

May is here and with that has come the arrival of the worst six-month period for stocks. Perhaps it is too early to say that “sell in May and go away” is on in full force, but the S&P 500 is off 0.28% since the start of the month.

Momentum offerings have fared worse. For example, the iShares Russell 2000 ETF (IWM) is down 1.7% since May 1 while the Nasdaq Composite is lower by almost 1.4%. That is not the start to the fifth month of the anti-sell in May crowd was hoping for, but there are trades investors can put on to help ameliorate the summertime doldrums.

Take the example of a trade involving the Powershares DWA Momentum Portfolio (PDP) and the Powershares S&P 500 Low Volatility (SPLV) with SPLV being an ideal play for an environment that favors low volatility and value. [Getting Defensive With Low Vol ETFs]

The two-minute overview of the PDP/SPLV switching strategy as presented by Dorsey Wright & Associates is that SPLV is the avenue of choice during the worst six-month period for stocks, the period the market is currently in, while PDP is the way to go in the November through April time frame.

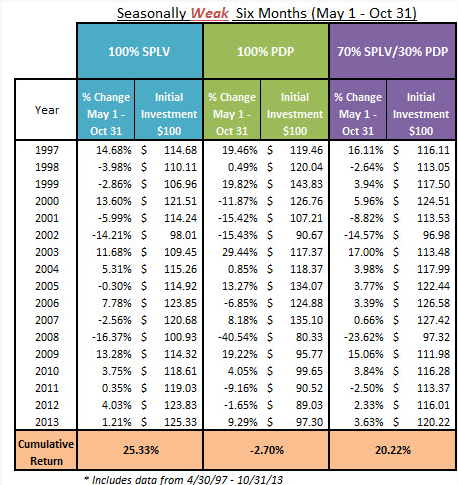

“The backdrop for our strategy all lies in the historical bias that having exposure to the market during the seasonally strong six months is a good thing, and having exposure to the market during the seasonally weak period has caused more headache than actual return,” notes Dorsey Wright.

Dorsey Wright’s PDP/SPLV switching strategy goes like this: An investor is 70% invested in PDP and 30% in SPLV from November through April. When May rolls around, the trade switches to 70% SPLV and 30% PDP. [Monthly Dividend ETFs]

“The SPLV has generally provided greater returns during the seasonally weak six months (cumulative of 25.33% since 4/30/1997) than the PDP (-2.70%). However, the SPLV has notably lagged the return of the PDP during the seasonally strong six months, up 127.08% compared to 597.42%, respectively. Therefore, a 30% PDP/70% SPLV split during the seasonally weak six months has seen a cumulative return of 20.22%, while a 70% PDP/30% SPLV split during the seasonally strong six months has seen a return of 435.8%, according to Dorsey Wright.

A 10-year backtest running through April 17, 2014 shows the PDP/SPLV switching strategy generated averaged annualized returns of almost 7.1%, nearly 200 basis points better than the S&P 500 over the same time. The three-year standard deviation on the PDP/SPLV strategy was just under 10% compared to almost 12.4% for the S&P 500, according to Dorsey Wright data. [An ETF Strategy for the Best Six Months]

The strategy is not a holy grail. For example, U.S. stocks were strong during the seasonally weak period last year, leading to 3.63% return for 70% SPLV/30% PDP portfolio when being 100% in PDP offered better than double that upside. However, the long-term track record is stout and the PDP/SPLV switch is a way for investors to stay involved in stocks during the weakest six months.

Table Courtesy: Dorsey Wright & Associates

Tom Lydon’s clients own shares of IWM.