Factor Seasonality: Analyzing a Variety of Investing Behaviors

Note: This article appears on the ETFtrends.com Strategist Channel

By Grant Engelbart, CFA

Factors have become widely-agreed-upon drivers of risk and return, backed by academia and practitioners alike. Explanations for outperformance have been cataloged from both a fundamental and behavioral perspective. Factors have transitioned from anomalies to truths in many circles. One market anomaly recognized for decades (perhaps longer) has been the idea of seasonality in the stock market. The “Santa Claus Rally,” “January Effect,” and “Summer Swoon,” have all been recognized patterns of persistence. Seasonality, however, has not taken on the same academic truth as factors; nonetheless, it’s possible they can coexist.

Seasonality can prompt a variety of behaviors, whether avoiding Mondays or capitalizing on turn-of-the-month effects. But, perhaps the most visible imprint of seasonality on the markets is the relative slowdown of the summer months. Whether measured since the turn of the century, post-World War II, or Volcker era, the S&P 500 and global stock market (measured by MSCI ACWI) have outperformed during the November to April period.

Related: No, This is Not an Ugly Chart on Factor Investing

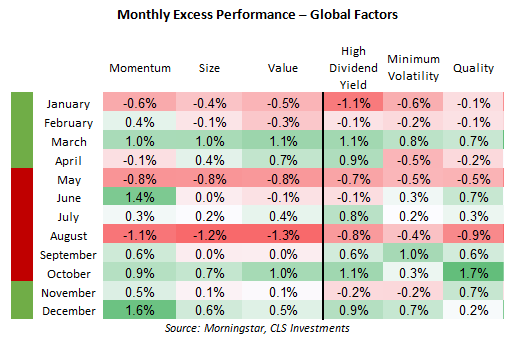

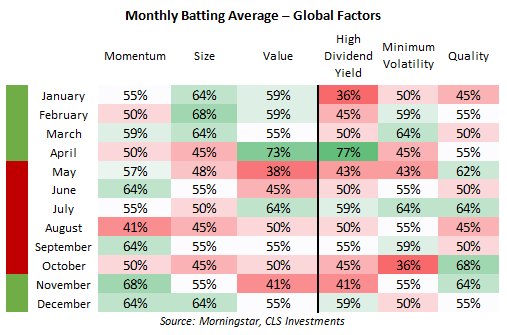

Turning to Factors, March, October, and December have been the best months for global factors to outperform the broader ACWI Index, while January, May, and August have been the worst. This is true for both excess performance and batting average, or the percentage of time the factor outperforms the parent index. Cyclical factors (left side on the chart below) tend to do somewhat better during the stronger seasonal period of November to April, while defensive factors (right side) tend to hold up better in the lackadaisical summer months. (Note: it is questionable whether high dividend yield is cyclical or defensive, as the factor splits its time below or above the risk of the broad market historically).

Looking at individual factors, there are a few interesting tidbits. On average, size underperforms in January, contrary to conventional thought, albeit at a low percentage. Quality does best in January. Window dressing in December would potentially lead to the opposite effect, as quality stocks would be sold in January and smaller cap stocks purchased.

Interestingly, April has a strong tendency for outperformance by value-oriented factors (value and high dividend yield), both outperforming more than 70% of the time. Perhaps investors get excited about Berkshire Hathaway’s annual meeting in late April/early May and pile into value stocks? Obviously not; a more likely explanation could be the strong seasonality of crude oil during April relating to refinery maintenance, summer driving demand, and the switchover to summer-blend fuels – all of which have historically helped propel energy stocks (classic value names) higher.

Related: An Equation to Identify the Next Market Bubble?

One final observation here – these indices are rebalanced at the end of May and November. There doesn’t seem to be a meaningful performance or batting average result the month following rebalance for all factors, but it could potentially be argued that momentum sees some impact from fresh index holdings in June and December.

While this may seem like voodoo to some, it is possible to conceptualize several strategies, with a little engineering, from the historical seasonality of various factors. A simple way to take advantage of different market environments would be to favor cyclical factors during strong months (November-April), and defensive factors during weaker months (May-October).

Related: The Bayesian View to Multi-Factor ETF Investing

Simple enough, right? This would keep investors broadly diversified and invested, while altering their risk profiles slightly during weaker periods of time. Many practitioners have followed a similar strategy with different tools.

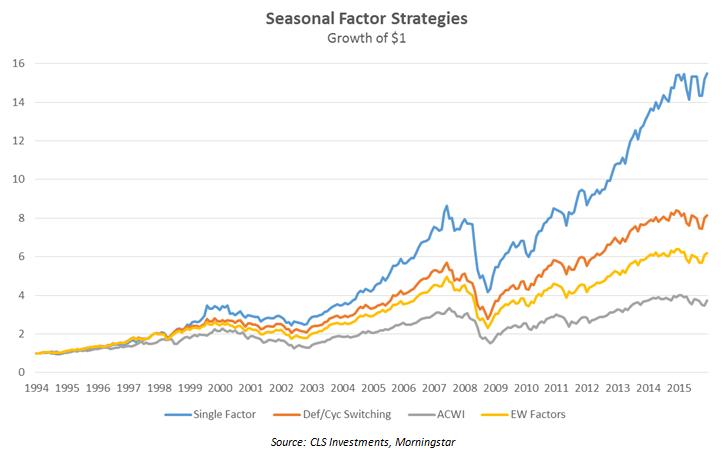

In the chart below, the orange line demonstrates the performance of this strategy over time, generating significant alpha above the ACWI and above an equally-weighted mix of all six factors we covered here. Of course, this is excluding transaction costs and ignoring the fact that there aren’t currently ETFs covering all of these ACWI factors.

If one were to simply invest each month in the factor that has historically had the highest batting average (percent chance to outperform), the results are quite impressive, as indicated by the blue line. This is similar to that of the defensive and cyclical-switching strategy, but utilizes only a single factor. During the months of January and February size is favored; minimum volatility is utilized in the summer; and momentum in the later months of the year. Very simple, yet very impressive results. However, we are faced with the possibility that past results won’t correlate with the future and the potential for incurring sizeable transaction costs associated with making those monthly trades.

While seasonality is thought by many to be consequential, there are still important and relevant considerations for the active manager when allocating throughout the year. Utilizing factors in strategies like these greatly increases diversification and can also reduce the chances of being wrong, particularly versus a sector-timing strategy. Factor investing is becoming a more important part of the investing landscape, particularly as high fees and active management come under pressure. Being able to utilize factors to an investor’s advantage is crucial. Now we just need the ETFs to do it!

Related: Are Factor ETFs the Key to Unlocking Your Portfolio’s Risk DNA?

This information is prepared for general information only. Information contained herein is derived from sources we believe to be reliable, however, we do not represent that this information is complete or accurate and it should not be relied upon as such. All opinions expressed herein are subject to change without notice. The graphs and charts contained in this work are for informational purposes only. No graph or chart should be regarded as a guide to investing.

Grant Engelbart is a Portfolio Manager at CLS Investments , a participant in the ETF Strategist Channel .