These Factors Make Johnson Electric Holdings Limited (HKG:179) An Interesting Investment

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Building up an investment case requires looking at a stock holistically. Today I’ve chosen to put the spotlight on Johnson Electric Holdings Limited (HKG:179) due to its excellent fundamentals in more than one area. 179 is a financially-healthy company with a a strong track record of performance, trading at a great value. Below is a brief commentary on these key aspects. For those interested in digger a bit deeper into my commentary, take a look at the report on Johnson Electric Holdings here.

Excellent balance sheet, good value and pays a dividend

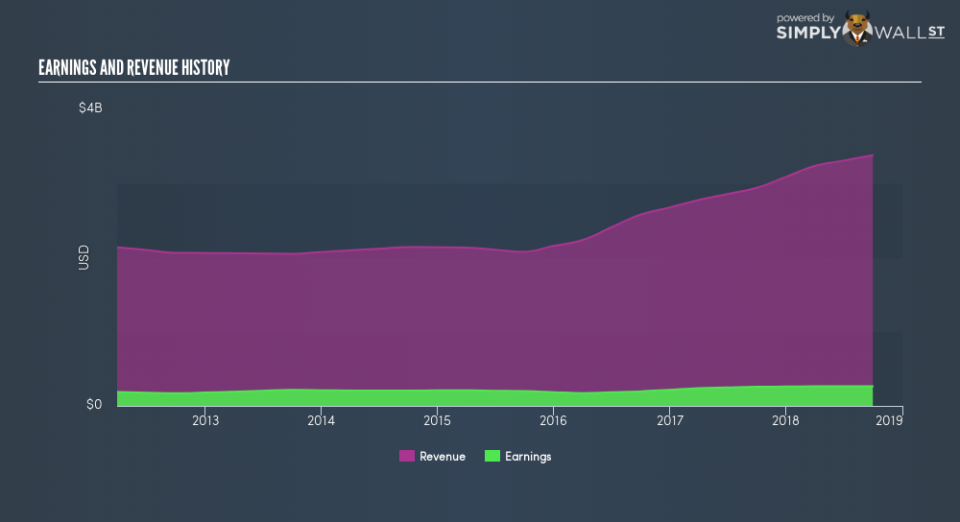

179 has a strong track record of performance. In the previous year, 179 delivered an impressive double-digit return of 6.9% Not surprisingly, 179 outperformed its industry which returned 4.6%, giving us more conviction of the company’s capacity to drive bottom-line growth going forward. 179’s strong financial health means that all of its upcoming liability payments are able to be met by its current cash and short-term investment holdings. This indicates that 179 has sufficient cash flows and proper cash management in place, which is a crucial insight into the health of the company. 179 appears to have made good use of debt, producing operating cash levels of 0.71x total debt in the prior year. This is a strong indication that debt is reasonably met with cash generated.

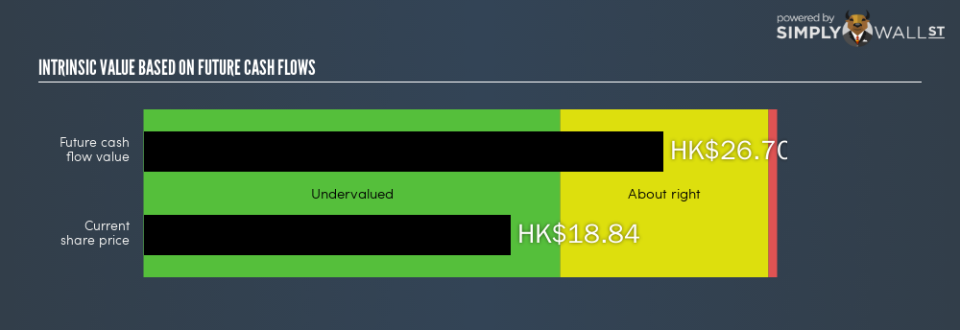

179 is currently trading below its true value, which means the market is undervaluing the company’s expected cash flow going forward. This mispricing gives investors the opportunity to buy into the stock at a cheap price compared to the value they will be receiving, should analysts’ consensus forecast growth be correct. Compared to the rest of the electrical industry, 179 is also trading below its peers, relative to earnings generated. This supports the theory that 179 is potentially underpriced.

Next Steps:

For Johnson Electric Holdings, I’ve put together three essential aspects you should further examine:

Future Outlook: What are well-informed industry analysts predicting for 179’s future growth? Take a look at our free research report of analyst consensus for 179’s outlook.

Dividend Income vs Capital Gains: Does 179 return gains to shareholders through reinvesting in itself and growing earnings, or redistribute a decent portion of earnings as dividends? Our historical dividend yield visualization quickly tells you what your can expect from 179 as an investment.

Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of 179? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.