Factors Likely to Decide Dillard's (DDS) Fate in Q4 Earnings

Dillard’s, Inc. DDS is expected to register year-over-year top and bottom-line declines when it reports fourth-quarter fiscal 2022 numbers.

The Zacks Consensus Estimate for fiscal fourth-quarter revenues of $2.11 billion indicates a 0.1% decline from the year-ago reported figure. The Zacks Consensus Estimate for fiscal fourth-quarter earnings is pegged at $8.85 per share, indicating a 43.6% decrease from the year-ago quarter’s reported figure. The consensus estimate has moved down 0.2% in the past 60 days.

We expect the company’s fiscal fourth-quarter total revenues to decline 2.4% year over year to $2.1 billion and the bottom line to plunge 44.7% to $8.85 per share.

For fiscal 2022, the Zacks Consensus Estimate is pegged at $6.89 billion, suggesting 6% growth from the prior-year quarter’s reported figure. The Zacks Consensus Estimate for fiscal 2022 earnings indicates a 4.5% year-over-year increase to $41.85. We expect the company’s fiscal 2022 total revenues to advance 4.7% year over year to $6.9 billion and the bottom line to increase 2.2% to $42.8 per share.

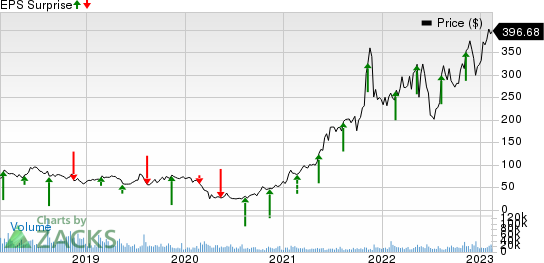

In the last reported quarter, the company reported an earnings surprise of 125.1%. We note that in the trailing four quarters, the company’s bottom line beat the Zacks Consensus Estimate by 144.2%, on average.

Dillard's, Inc. Price and EPS Surprise

Dillard's, Inc. price-eps-surprise | Dillard's, Inc. Quote

Key Factors to Note

Dillard’s has been benefiting from continued momentum in consumer demand and inventory-management initiatives. The company’s strategy to offer fashion-forward and trendy products in order to attract customers has been a key driver.

The company is likely to have retained its sales momentum on robust sales across product categories and regions. It has been witnessing robust demand for cosmetics, men’s apparel and accessories, home and furniture, and shoes.

However, stiff competition and inflation are likely to have been concerning. The company has been witnessing elevated SG&A expenses for the past few quarters, which have been denting the bottom line to some extent. Also, increased payroll and payroll-related expenses are likely to have acted as headwinds. Such downsides are anticipated to have affected the company’s profitability in the to-be-reported quarter.

What the Zacks Model Suggests

Our proven model does not conclusively predict an earnings beat for Dillard’s this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Dillard’s currently has a Zacks Rank #4 (Sell) and an Earnings ESP of 0.00%.

Stocks With Favorable Combination

Here are three companies worth considering, as our model shows that these have the right combination of elements to beat on earnings this time around.

American Eagle Outfitters AEO has an Earnings ESP of +1.96% and currently flaunts a Zacks Rank #1. The Zacks Consensus Estimate for AEO’s fourth-quarter fiscal 2023 earnings stands at 30 cents per share, implying a year-over-year decline of 14.3%. You can see the complete list of today’s Zacks #1 Rank stocks here.

American Eagle is estimated to report revenues of $1.47 billion, which suggests a fall of 2.5% from the year-ago quarter. AEO has a trailing four-quarter negative earnings surprise of 5%, on average.

Casey's General Stores CASY currently has an Earnings ESP of +14.04% and a Zacks Rank #3. The company is expected to register a bottom-line decline when it reports third-quarter fiscal 2023 results. The Zacks Consensus Estimate for quarterly earnings per share of $1.66 suggests a decrease of 2.9% from the year-ago quarter.

Casey's top line is anticipated to rise year over year. The consensus mark for revenues is pegged at $3.57 billion, indicating an increase of 17.2% from the figure reported in the year-ago quarter. CASY has a trailing four-quarter earnings surprise of 7.2%, on average.

Dollar General DG currently has an Earnings ESP of +0.93% and a Zacks Rank #3. DG is likely to register year-over-year top-line growth in its fourth-quarter fiscal 2022 results. The Zacks Consensus Estimate for quarterly revenues is pegged at $9.43 billion, suggesting 10.7% growth from the figure reported in the prior-year quarter.

The Zacks Consensus Estimate for Dollar General’s earnings for the fiscal fourth quarter is pegged at $2.54 per share, suggesting 22.1% growth from the year-ago quarter’s actual. The consensus mark has been unchanged in the past 30 days. DG delivered an earnings beat of 2.2%, on average, in the trailing four quarters.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dillard's, Inc. (DDS) : Free Stock Analysis Report

Dollar General Corporation (DG) : Free Stock Analysis Report

American Eagle Outfitters, Inc. (AEO) : Free Stock Analysis Report

Casey's General Stores, Inc. (CASY) : Free Stock Analysis Report