How Financially Strong Is Marston’s PLC (LON:MARS)?

Marston’s PLC (LON:MARS) is a small-cap stock with a market capitalization of UK£639.33m. While investors primarily focus on the growth potential and competitive landscape of the small-cap companies, they end up ignoring a key aspect, which could be the biggest threat to its existence: its financial health. Why is it important? Assessing first and foremost the financial health is crucial, as mismanagement of capital can lead to bankruptcies, which occur at a higher rate for small-caps. Here are a few basic checks that are good enough to have a broad overview of the company’s financial strength. However, since I only look at basic financial figures, I suggest you dig deeper yourself into MARS here.

How much cash does MARS generate through its operations?

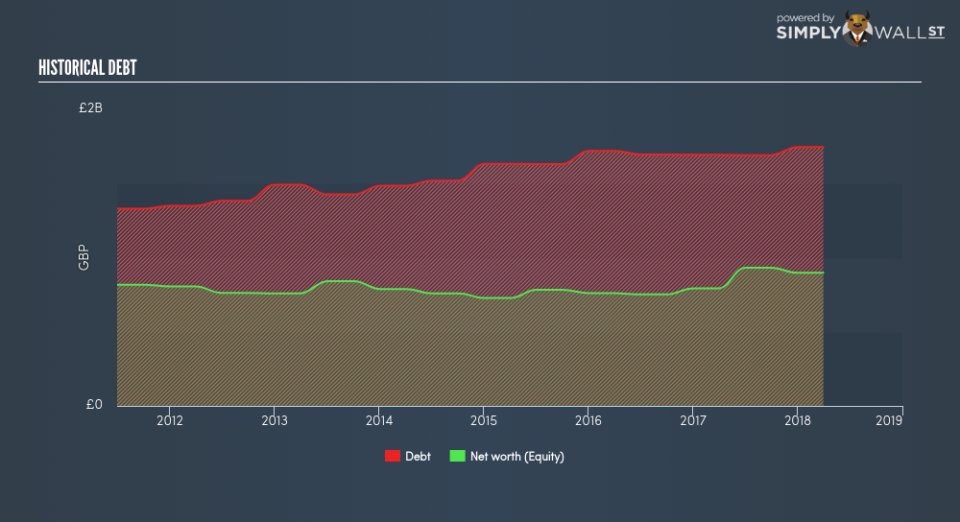

MARS has sustained its debt level by about UK£1.69b over the last 12 months – this includes both the current and long-term debt. At this current level of debt, MARS currently has UK£54.60m remaining in cash and short-term investments for investing into the business. Additionally, MARS has generated UK£213.60m in operating cash flow over the same time period, leading to an operating cash to total debt ratio of 12.63%, meaning that MARS’s current level of operating cash is not high enough to cover debt. This ratio can also be a sign of operational efficiency as an alternative to return on assets. In MARS’s case, it is able to generate 0.13x cash from its debt capital.

Can MARS meet its short-term obligations with the cash in hand?

At the current liabilities level of UK£440.40m liabilities, the company has not maintained a sufficient level of current assets to meet its obligations, with the current ratio last standing at 0.74x, which is below the prudent industry ratio of 3x.

Does MARS face the risk of succumbing to its debt-load?

MARS is a highly-leveraged company with debt exceeding equity by over 100%. This is not unusual for small-caps as debt tends to be a cheaper and faster source of funding for some businesses. We can test if MARS’s debt levels are sustainable by measuring interest payments against earnings of a company. Ideally, earnings before interest and tax (EBIT) should cover net interest by at least three times. For MARS, the ratio of 2.26x suggests that interest is not strongly covered, which means that lenders may be more reluctant to lend out more funding as MARS’s low interest coverage already puts the company at higher risk of default.

Next Steps:

MARS’s high debt levels is not met with high cash flow coverage. This leaves room for improvement in terms of debt management and operational efficiency. In addition to this, its lack of liquidity raises questions over current asset management practices for the small-cap. This is only a rough assessment of financial health, and I’m sure MARS has company-specific issues impacting its capital structure decisions. You should continue to research Marston’s to get a more holistic view of the stock by looking at:

Future Outlook: What are well-informed industry analysts predicting for MARS’s future growth? Take a look at our free research report of analyst consensus for MARS’s outlook.

Valuation: What is MARS worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether MARS is currently mispriced by the market.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.