How Financially Strong Is Shineco Inc (NASDAQ:TYHT)?

While small-cap stocks, such as Shineco Inc (NASDAQ:TYHT) with its market cap of $48.38M, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Assessing first and foremost the financial health is essential, since poor capital management may bring about bankruptcies, which occur at a higher rate for small-caps. Here are few basic financial health checks you should consider before taking the plunge. Though, since I only look at basic financial figures, I recommend you dig deeper yourself into TYHT here.

Does TYHT generate enough cash through operations?

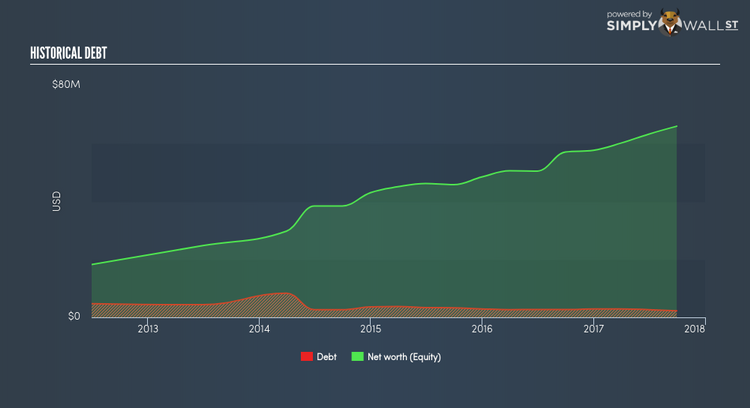

TYHT’s debt level has been constant at around $2.7M over the previous year . At this stable level of debt, TYHT currently has $23.3M remaining in cash and short-term investments , ready to deploy into the business. Though its operating cash flow is not yet significant enough to calculate a meaningful cash-to-debt ratio, indicating that operational efficiency is something we’d need to take a look at. As the purpose of this article is a high-level overview, I won’t be looking at this today, but you can take a look at some of TYHT’s operating efficiency ratios such as ROA here.

Does TYHT’s liquid assets cover its short-term commitments?

At the current liabilities level of $5.0M liabilities, it seems that the business has maintained a safe level of current assets to meet its obligations, with the current ratio last standing at 8.89x. Though, a ratio greater than 3x may be considered as too high, as TYHT could be holding too much capital in a low-return investment environment.

Does TYHT face the risk of succumbing to its debt-load?

With debt at 3.42% of equity, TYHT may be thought of as having low leverage. This range is considered safe as TYHT is not taking on too much debt obligation, which may be constraining for future growth. We can check to see whether TYHT is able to meet its debt obligations by looking at the net interest coverage ratio. A company generating earnings before interets and tax (EBIT) at least three times its net interest payments is considered financially sound. In TYHT’s, case, the ratio of 194.43x suggests that interest is excessively covered, which means that debtors may be willing to loan the company more money, giving TYHT ample headroom to grow its debt facilities.

Next Steps:

Are you a shareholder? Although TYHT’s debt level is relatively low, its cash flow levels still could not copiously cover its borrowings. This may indicate room for improvement in terms of its operating efficiency. However, the company exhibits an ability to meet its near term obligations should an adverse event occur. Given that its financial position may be different. I suggest researching market expectations for TYHT’s future growth on our free analysis platform.

Are you a potential investor? TYHT’s low-debt position gives it headroom for future growth funding in the future. In addition, its high liquidity means the company should continue to operate smoothly in the case of adverse events. In order to build your confidence in the stock, you need to further analyse TYHT’s track record. I encourage you to continue your research by taking a look at TYHT’s past performance analysis on our free platform to conclude on TYHT’s financial health.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.